")

Saia, Inc. (NASDAQ:SAIA), the LTL transportation holding company, reported relatively weak quarterly results on July 26, sending its stock price plummeting 19% in one day. Earnings per share were $3.83 instead of the expected $4.08, and revenue for 2Q2024, although it reached a record value of $823 million, was also below analysts’ forecasts of $843 million.

Today I want to look at how dramatically the business is doing following this market reaction to the report and find out through careful quantitative analysis of the financial data whether SAIA shares are viable investments today.

LTL Industry Overview

Saia provides less-than-truckload (LTL) services through a single integrated organization. The company also offers customers various value-added services across North America, including non-asset truckload, expedited, and logistics services. Less-than-truckload or less-than-load is a shipping service for relatively small loads or quantities of freight. LTL services have gained great importance in the modern economy with the rise of e-commerce, delivering products quickly to customers is a must for online businesses.

US LTL Market (Mordor Intelligence)

Despite this, the LTL segment is still significantly smaller than full truckload (FTL) with an approximate share of 11.3% of trucking. However, this is a fairly large market with a volume of approximately $109 billion and a growth rate of 3.24% CAGR (4.19% is expected for 2024-2023).

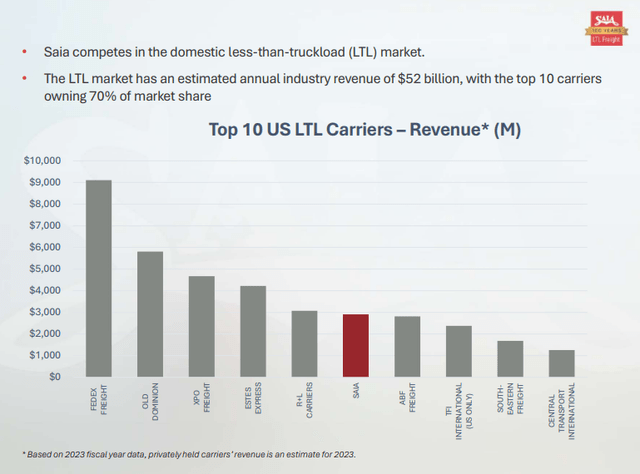

Saia is among the top 7 companies in the industry, with an annual revenue of $3.1%. What is extremely important is that it is developing much faster than the market, demonstrating a growth rate of 12.3% CAGR.

According to this indicator, the company is significantly ahead of market leaders FedEx (FDX) with 5.5% and Old Dominion Freight Line (ODFL) with 8.7% growth rates.

This dynamics allows me to believe that the company will be able to win the part of the market shortly and significantly increase its current share of 2.8% (based on 2023 results). True, the company operates with a market volume of $52 billion, considering only privately held carriers’ revenue.

Top 10 US LTL Companies (Saia Inc.)

Financial Performance

Saia doesn’t impress with its margins. Judging by the reporting for the second quarter, 45% of revenue is spent on paying staff, almost 20% – on fuel and materials, and 7% goes to cover the purchase of new vehicles. Add depreciation here and we get a net margin of 12%. Although the company does not disclose the cost of goods sold and gross margin in its reports, according to Seeking Alpha, gross margin is 27%.

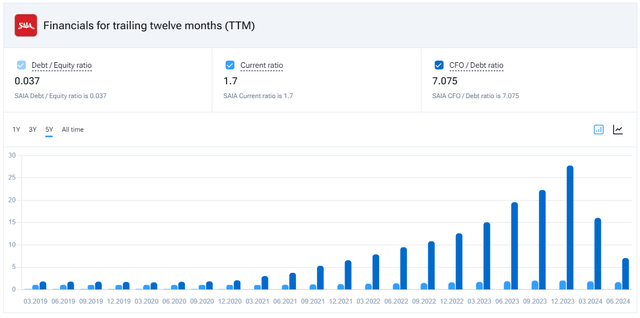

However, the quality of earnings of $354.8 million for 2023 and $102.5 million for Q2 2024 is very high. This is evidenced by the analysis of cash flow statements. Dividing net cash provided by operating activities cash flow by net profit for the last 12 months, I get a value of 1.38 or 138% – whichever is more convenient for you to analyze the numerical value. Saia can confirm the accrued profit in the financial statements with the actual funds received into the company’s account, and this is undoubtedly a positive point for me.

Zero-emission Nikola Heavy Truck (Nikola Motor)

Frankly, the analysis of profitability indicators that I do in search of some undoubted advantages of the company is not impressive. There are no significant flaws in the reports, nor are there any super-positive signals. Relatively low margins are an illustration of high competition in the industry; therefore, investors should not expect a quick and multiple increase in share price from Saia – there are simply no prerequisites for this.

Financial Position

Suddenly, in the second quarter, the company increased its long-term borrowings by 28 times: from $6 to $169 million! Saia is a party to an unsecured credit agreement with Revolving Credit Facility, which provides up to a $300 million revolving line of credit through February 2028, according to the Credit Arrangements notes (page 9) to Condensed Consolidated Financial Statements.

I will quote the words of Saia President and CEO, Fritz Holzgrefe, who commented on the quarter, stating in a press release on the company website:

During the quarter, we successfully opened six new terminals and relocated two others in new and established markets, while maintaining our high service standards. Successfully opening and relocating terminals required investments in employee hiring, training and other costs that come in advance of opening and revenue generation… We are excited about the opening of our new Stockton, California and Davenport, Iowa terminals earlier this week, and as we move through the rest of 2024, we plan to continue executing on our opening timeline, with the potential to open an additional 10 to 13 new terminals this year.”

Saia’s solvency metrics (eyestock.io)

According to the balance sheet as of June 30, 2024, cash and equivalents were only $11 million. It seems that all of the above figures and company statements are linked in one chain. To maintain the business growth that I spoke about at the very beginning, the company is making appropriate efforts, which is important, without severely compromising its solvency.

Despite this fact of borrowings increasing, total debt remains very modest: approximately $180 million against a stockholders’ equity of over $2.1 billion. If you look at the Debt-to-equity ratio of 0.037, then everything is in order. Liquidity is also good, the current ratio is 1.7.

Management Efficiency and Growth Sustainability

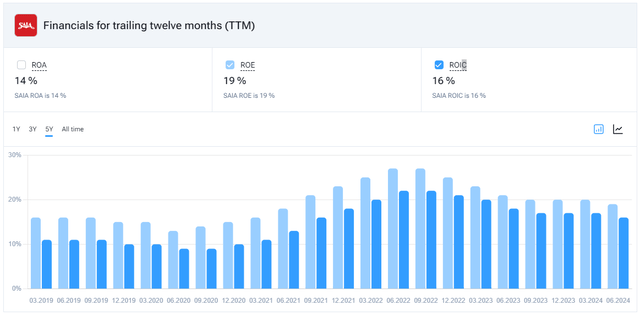

As with margins, the efficiency of management in the form of return on capital is sufficient for me, but not dizzying. Return on equity is 19% according to my calculation and ROIC, which I prefer a little more for evaluating efficiency – is 16%. What is important is that both indicators have a medium-term downward trend.

The 5-year dynamic of Saia’s ROE and ROIC (eyestock.io)

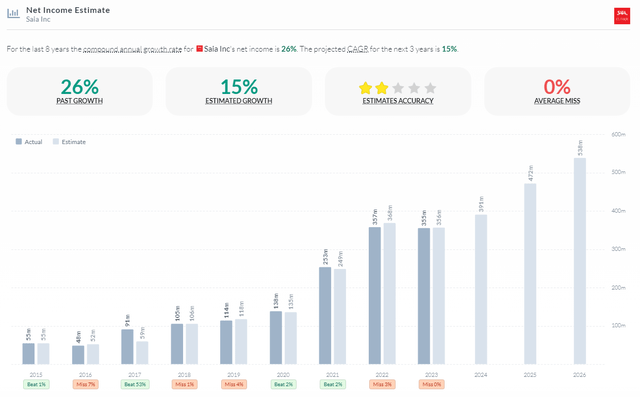

As well as the growth rate of net profit, if you look at quarterly dynamics. However, as I said, the company has historically grown at a faster rate than the market. For the last 8 years, the compound annual growth rate for Saia’s net income is 26%. The average growth rate of net profit over 5 years (42%) is significantly higher than the two years (14%) if we take the quarter-to-quarter ratio as a basis. This confirms that the company is in a correction phase. However, what I pay close attention to is the mathematical deviation of the growth rate. For 5 and 2-year periods, the deviation value is 45% and 11%, which practically corresponds to the average growth rate. Is this good? I believe that this is an acceptable indicator at this point, which suggests that future profits can be predicted based on this track with a high confidence interval.

Saia’s growth rate of net income (alphaspread.com)

After the analysis and the listed financial characteristics regarding the industry and the company itself, I had a clear idea that I was not dealing with a star, but with a very tough nut to crack that could become part of my investment portfolio. However, for such investments, it is doubly important to carefully select the entry point, since a mistake with it can ruin the whole idea.

Valuation and Future Prospects

I am not a strong forecaster. And it is not part of my decision-making system. Therefore, I will judge the value of Saia solely from the standpoint of numbers, comparing the current valuation with the historical one and with competitors. As of August 14, Saia’s price share is $375 and this means that the price-to-earnings ratio is about 26. This estimate is higher than the industry median and, in particular, the industry leader in market share, but not in terms of performance, FedEx (P/E TTM 16). For reasons that are clear to me: FedEx is performing much worse financially, and its profit growth rate is much weaker.

But this score is lower than ODFL (P/E TTM 33). And also for reasons that are clear to me. The second-largest market player has significantly better margins and returns on capital, and therefore has a premium in valuation. It looks like Saia is being priced fairly as of today.

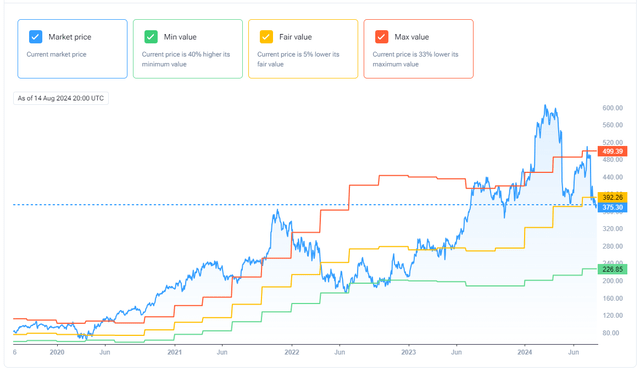

Saia’s quantitative valuation (eyestock.io)

Moreover, the historical median meaning of Saia’s P/E for the last 20 quarters is 27.6 which is so close to the current valuation. The current price is 5% below the median P/E multiplied by 12-month trailing earnings per share, which I use as a fair valuation. That is, the growth potential is quite limited.

Conclusion

With fairly solid financials on review and a strong industry presence, the company caught my eye and is a quality candidate for a moderate portfolio share given the recent share price decline. While not a star stock with prospects for multiple growth, Saia can become a good representative of the Industrial sector with a clear development track. However, when I deal with such stocks with limited prospects, I want to get a price discount, but there is none. The company is now fairly valued by all methods. I do not exclude that I will begin to collect a position at current prices soon, but, of course, I would like to see prices at $220-240 per share to receive a strong buy signal.

Read the full article here

")