")

Investment thesis

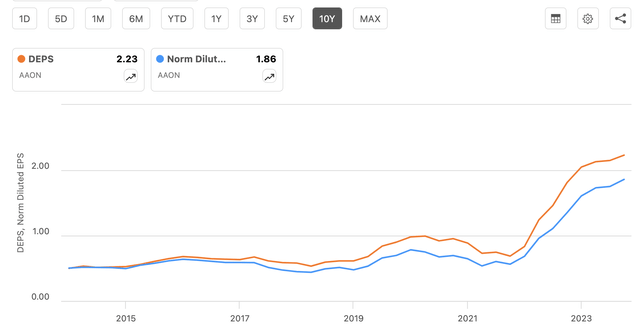

The earnings of HVAC company AAON, Inc. (NASDAQ:AAON) took off in the third quarter of 2022 and are expected to climb even more in 2025 and 2026. This 10-year chart shows its diluted and normalized EPS history through June 2024:

AAON earnings history chart (Seeking Alpha)

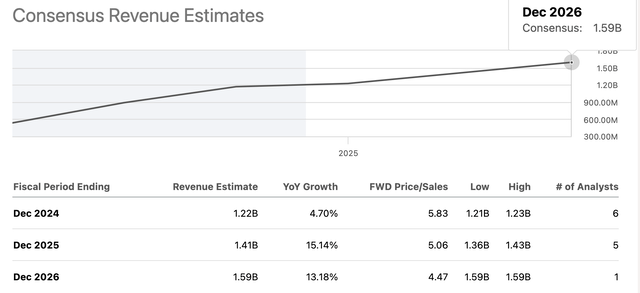

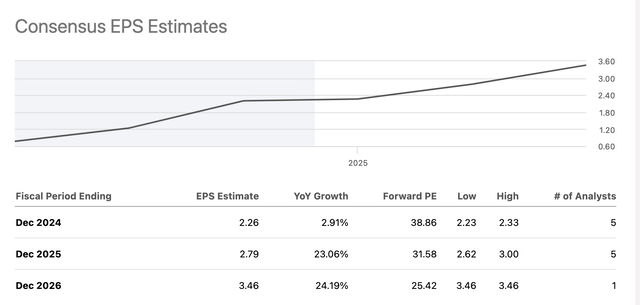

After a relatively flat 2024, earnings are expected to rise 23.06% in 2025 and 24.19% in 2026. In common with Wall Street analysts, I have a $99.00 one-year price target and have rated AAON a Buy.

About AAON

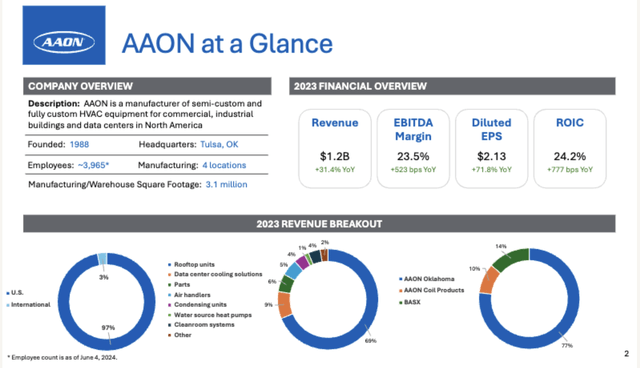

Founded in 1987, AAON builds heating, ventilation, and air conditioning [HVAC] systems for the commercial and industrial indoor markets. This slide, from its Q2-2024 earnings presentation, provides an overview of the company and where it gets its revenue:

AAON at a glance (Q2 earnings presentation)

As the slide shows, it gets 69% of that revenue from rooftop units, and 97% of its revenue is generated domestically.

The firm operates through three business segments:

- AAON Oklahoma: engineers, manufactures, and sells custom and semi-custom HVAC systems, as well as controls solutions and retail parts.

- AAON Coil Products: engineers and manufactures custom and semi-custom HVAC systems, as well as heating and cooling coils for HVAC systems.

- BASX: engineers, manufactures, and sells custom, high-performance cooling solutions for the data center market, ventilation solutions for cleanrooms, and highly custom air handlers and modular solutions.

One customer, Texas AirSystems accounted for 13.8%, 12.4%, and 11.7% of sales in 2023, 2022, and 2021, respectively.

The firm had a record backlog at the end of the second quarter. According to the Q2-2024 earnings release, it amounted to $650 million versus $526 million in the same quarter last year. The company reported in its 10-K for 2023 that the size of the backlog in recent years has mostly eliminated what had been moderate seasonality.

Research and development have become essentials, as engineering for performance, flexibility, and serviceability have become critical factors in the industry. In 2023, it spent about $43.7 million on R&D. It further noted that it does not consider any of its patents, etc. to be material to its business operations, although it does hold several patents related to the design and use of its products.

At the close on August 16, AAON traded at $88.69, and it had a market cap of $7.24 billion.

Competition and competitive advantages

There are many competitors in the industry, and competition is intense. It reported in the 10-K that its AAON Oklahoma and AAON Coil Products segments compete mainly with Lennox International Inc. (LII), Trane Technologies plc (TT), York International (Johnson Controls International plc (JCI)), Carrier Global Corporation (CARR), and Daikin Industries (OTCPK:DKILF).

The BASX segment competes with Vertiv Holdings Co. (VRT), STULZ Air Technology Systems, Inc., Munters Group AB (OTCPK:MMNNF), Silent Aire (Johnson Controls International PLC), Nortek Inc. (NTK), and Engineered Air.

AAON noted that all of its publicly traded competitors are larger and have greater resources. While these competitors may be able to offer lower prices, the company said it has been successful in recent years by competing on total value rather than price. That has made it more competitive in both the construction and replacement markets.

This strategy appears to have been successful, with margins greater than the Industrials sector medians:

- Gross margin: 36.27% versus 31.33%.

- EBITDA margin: 25.53% versus 13.79%.

- Net margin: 15.61% versus 6.19%.

- Return on common equity: 26.61% versus 12.84%.

The company argues it has a competitive advantage because of regulatory changes imposed by the Department of Energy on May 1. It explained the edge this way in the 10-K, “AAON perceives this as an advantage because our equipment is designed for higher energy efficiency and superior part load and dehumidification performance than competitors who focus on the initial sale price of their equipment or do not participate in the certification programs offered by AHRI.”

AAON may be a small player in the HVAC industry, but it appears to have good pricing power. With that in mind, I believe it has a medium-width moat.

Second-quarter financial results

Issued on August 1, AAON’s top and bottom-line results exceeded estimates:

- Net sales increased 10.4% to a record $313.6 million, compared to $284 million in the same period last year.

- Gross margin increased to 36.1%, from 33.1%.

- Earnings per diluted share jumped 12.7%, to $0.62.

- Cash, cash equivalents, and restricted cash of $12.1 million and a credit balance of $85.9 million.

- Repurchased $100 million in shares.

The sales increase was led by BASX, which increased its sales 58.3%, mainly through sales of data center equipment.

Management attributed improvement in the gross margin mainly to greater operational efficiencies at AAON Oklahoma and AAON Coil Products. The primary source of the backlog increase was also due to the data center market.

CEO Gary Fields noted in the Q2 earnings release, “Beyond the bookings that made up the backlog at quarter-end, there remains a large pipeline of data center projects for both airside and liquid cooling products that the Company is pursuing.”

On the balance sheet, the firm had total liabilities of $270.2 million, including $85.9 million in long-term debt. On the other side of the ledger, it had total assets of $1.011 billion, which included $12.1 million in cash.

At the end of Q2-2024, there were 81.0 million shares outstanding, down from 81.6 million at the end of June 2023.

Growth prospects

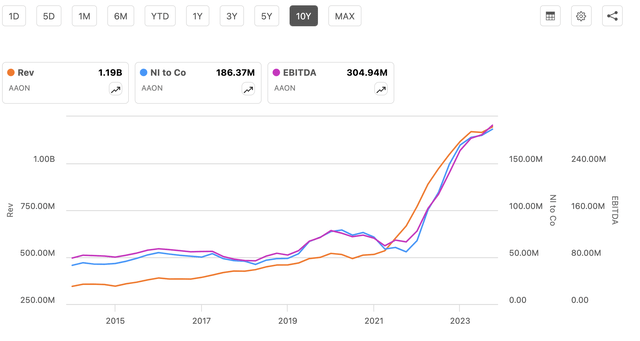

Until the third quarter of 2022, AAON has been a humdrum stock, with little growth:

AAON revenue, EBITDA, net income chart (Seeking Alpha)

Here’s how the company explained the turnaround in its annual report for 2022:

“At AAON, 2022 started off slow but finished with a bang. Hyperinflation and supply chain issues that weighed on our performance at the end of 2021 accelerated in the early months of 2022. In response, our team pivoted quickly and made necessary adjustments, resulting in profitability improving significantly throughout the year.

“By the third quarter, we achieved record sales and earnings, quickly followed with another record in the fourth quarter. We finished 2022 with record sales, earnings, and backlog. Our backlog finished up year-over-year 110% and increased sequentially every quarter even while we increased capacity and production rates.”

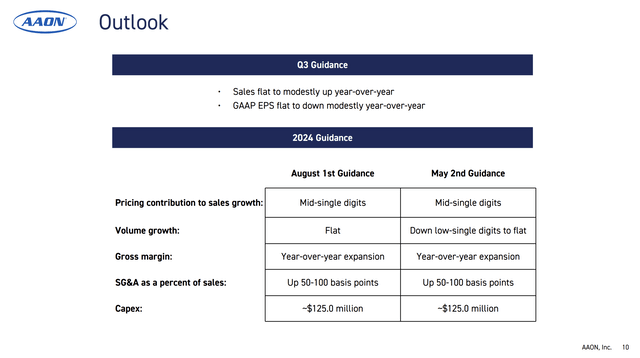

For the Q3 and the rest of this year, the company expects mostly flat results:

AAON outlook table (Q2 earnings presentation)

In the Q2 earnings call, CEO Fields pointed to softening macro conditions and disruptions caused by the refrigerant transition for its packaged rooftop business. The latter refers to implementation of the American Innovation and Manufacturing Act, which mandates that hydrofluorocarbons (major contributors to greenhouse warming) no longer be manufactured after December 31, 2024. They are being replaced by A2L refrigerants.

It’s true that BASX is doing well; however, it only made up 10.5% of net sales in the first half of 2024.

Fields sees a return to growth in 2025, after a flat 2024, as do the Wall Street analysts:

AAON revenue estimates table (Seeking Alpha)

They also see even bigger earnings pickups in the two years after 2024:

AAON EPS estimates table (Seeking Alpha)

AAON dividend

The dividend’s forward yield, with the share price at $88.69, is 0.36%. The annual payout is $0.32, and the payout ratio is 14.41%. In the first quarter of 2023 it began paying the dividend quarterly, rather than semi-annually.

It has paid a dividend for 16 consecutive years and currently has two consecutive years of growth.

Valuation

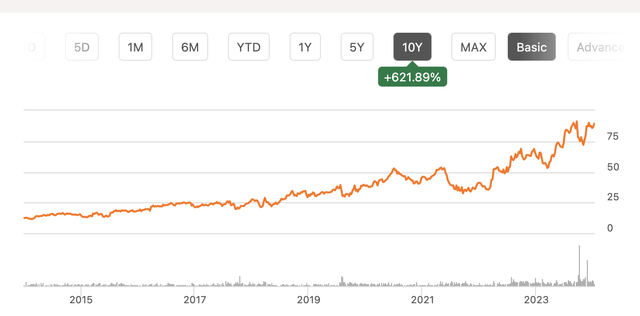

Generally, the AAON share price has made steady gains over the past decade, with a couple of exceptions:

AAON 10-year price chart (Seeking Alpha)

Supply chain woes and other challenges caused by pandemic-related issues caused one exception.

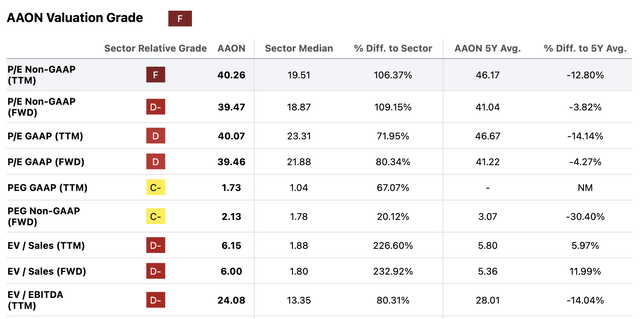

As this excerpt from the AAON valuation table at Seeking Alpha indicates, the stock appears to be overvalued. Even the PEG ratios are well above the fair value mark; there’s not enough growth to justify the high P/E ratios.

AAON excerpt from Valuation table (Seeking Alpha)

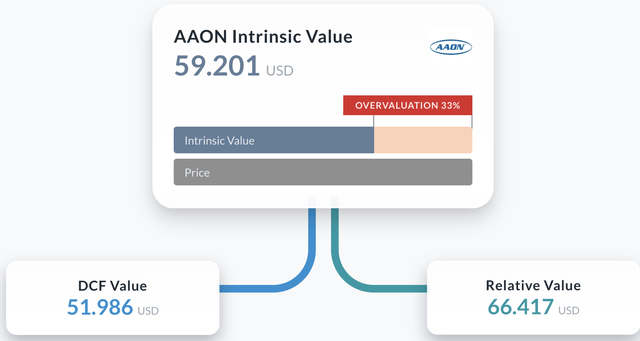

The value calculators at Alpha Spread come to the same conclusion:

AAON intrinsic value calculator (Alpha Spread)

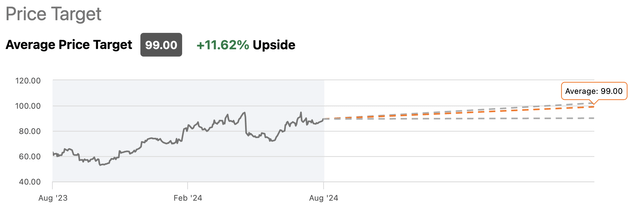

The Wall Street analysts have a one-year price target of $99.00, which, I think, is reasonable when considering the modest EPS growth through the rest of this year and then accelerated growth in 2025:

AAON price target chart (Seeking Alpha)

Note how close the price targets are among the six analysts providing targets. That suggests there is something close to a meeting of the minds on the price target.

My take on AAON’s situation is that the stock is overvalued if you are looking at a short-term investment. However, if you are considering an investment of three-years, five-years, or more, then the price is likely fair.

That’s backed up by the knowledge that the refrigerant transition will constrain earnings this year, but once past that, the company can count on both organic growth and the backlog to improve bottom-line results for the two years that follow.

As we saw above, the analysts expect modest year-over-year EPS growth in 2024, and then a 23.06% increase in 2025 and a 24.19% increase in 2026.

Based on AAON’s earnings prospects in the next two years and the $99 price target, I rate it’s a Buy. No other Seeking Alpha analysts have posted ratings in the past 90 days, while the company receives a Hold rating from the Quant system and a Buy from the Wall Street analysts (made up of three Strong Buys and three Holds).

Risk factors

The company leads off its list of risks with a possible recurrence of something like the COVID-19 pandemic. It noted that it experienced price increases in some of its components and raw materials because of COVID and subsequent inflation.

Demand for its products is linked to construction activity in the commercial and industrial markets. In turn, those markets are influenced by factors such as interest rates, consumer spending habits, and employment rates. To some extent, its large backlog mitigates this risk.

Most of its operations are in Tulsa, Oklahoma, an area where natural disasters, including tornados, occur frequently. And with the acquisition of BASX, it has operations in an area that has been affected by wildfires (Redmond, Oregon).

Low cash flow or other factors might affect its ability to fund research and development. AAON reported it operates in the highly competitive HVAC industry, which makes it essential that it develops new products and achieves technological advances.

Because it tries to minimize price fluctuations on the commodities it buys, it uses non-cancellable contracts with its major suppliers. These contracts typically last for six to 18 months, and if there is a downturn, then AAON would be committed to buying more materials than necessary for production, forcing it to carry excess inventory.

Conclusion

In the second half of 2022, AAON, Inc. took advantage of the normalization of supply chains, lower inflation, and its own internal improvements to become a growth stock. That growth will continue through at least 2026, as the company focuses on its total value solutions in the HVAC industry.

The bullish outlook has prompted investors to bid up the price of AAON stock, so it is somewhat overvalued, depending on which metric you use. However, it is still a good prospect for growth investors with medium to long-term outlooks.

I have a one-year price target of $99.00 and rated it as a Buy.

Read the full article here

")