")

")

")

Synopsis

Howmet (NYSE:HWM) specialises in supplying advanced engineered solutions for the aerospace and transportation industries. For 2Q24, HWM delivered strong earnings results. Its revenue grew 14% year-over-year, driven mainly by the commercial aerospace market. For context, commercial aerospace accounts for approximately 52% of HWM’s total revenue. Additionally, HWM’s 2Q24 adjusted margins also expanded year-over-year. According to data published by the International Civil Aviation Organisation, air travel demand is still strong. This is expected to bolster HWM’s outlook given the weight of the commercial aerospace market in HWM’s total revenue. Although Boeing is still facing challenges, HWM still has some optimism in them, thus increasing its expectations on Boeing’s expected build rate for Boeing’s 737 aircraft. Given HWM’s strong performance and favourable outlook, I am reiterating my buy rating.

Recap of Previous Coverage

In my previous coverage, I recommended a buy rating for HWM when it was trading at $80.21. The current share price has since increased to $93.88. This buy recommendation was based on several key factors. HWM’s historical financial results have demonstrated consistent top-line growth while maintaining robust profitability margins. In 1Q24, HWM reported strong results, with revenue growing 14% year-over-year, driven by significant growth in the commercial aerospace market.

Furthermore, data from the International Civil Aviation Organisation indicated strong passenger air traffic demand, with levels already exceeding pre-COVID figures. Aircraft deliveries were expected to increase in 2024 and continue growing into 2025. Airbus forecasted that total demand for new aircraft would reach approximately 40,850 by 2042.

HWM Business Overview

Investor Relations

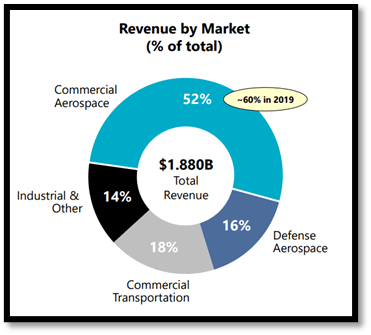

HWM’s end markets are segmented into key four areas. It comprises commercial aerospace, commercial transportation, defense aerospace, and industrial & other. Looking at the revenue by market chart above, its commercial aerospace end market forms the largest share of HWM’s total 2Q24 sales, accounting for 52%. The remaining three end markets in total account for less than half. Commercial transportation accounts for 18%, defense aerospace accounts for 16%, and industrial & others accounts for 14%.

Author’s Chart

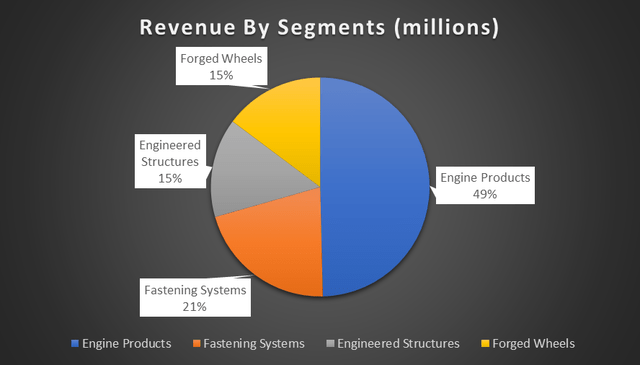

HWM’s has four reportable segments. These segments are engine products, fastening systems, engineered structures, and forged wheels. Looking at the above revenue by segment chart, engine products form the largest share of HWM’s 2Q24 total revenue, accounting for 49%. Given the scale of its engine products segment, it is crucial to analyse the performance of this segment.

Strong Air Travel Demand Fuels Positive Outlook

Given that the commercial aerospace market accounts for more than half of HWM’s revenue, it is an important market for the company. When analysing its most recent 2Q24 earnings results, HWM did discuss the strength and outlook of the commercial aerospace market. The strong air travel demand seen in the previous quarter continues and flows into the current quarter.

In particular, the growth of air traffic for international travel has strengthened in the Asia-Pacific region. For context, international travel has been growing by about 20%. On the freight side, demand and volume were robust as well. Apart from strong international travel demand, domestic travel demand has been growing as well.

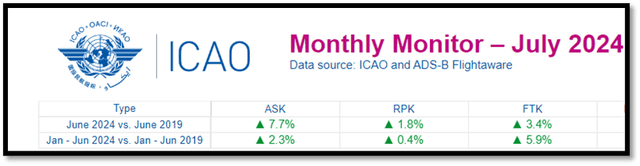

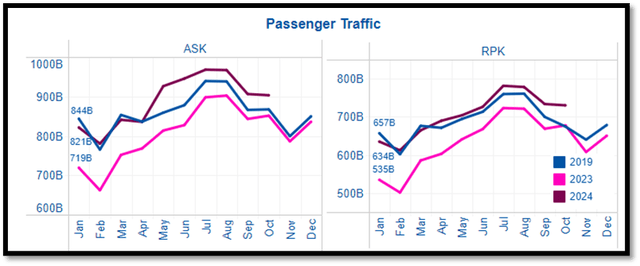

According to the data provided by the International Civil Aviation Organisation [ICAO], both revenue passenger kilometres [RPK] and available seat kilometres [ASK] increased when compared to June 2019 figures. For context, RPK is used to measure total demand, while ASK measures total capacity. For June 2024, ASK increased 7.7% when compared to June 2019, while RPK increased 1.8%. Looking at the passenger traffic chart, both 2024’s ASK and RPK, which are highlighted in brown, are above both 2023’s and 2019’s levels, or pre-COVID levels.

Looking ahead, ICAO forecasts that ASK and RPK for July to October 2024 will continue to exceed both 2023 and pre-pandemic levels. As a result, this positive outlook is expected to support HWM’s growth outlook.

International Civil Aviation Organisation International Civil Aviation Organisation

Boeing Situation Creating Slight Headwind

As discussed, the demand side is favourable for HWM, but it is currently limited by the supply side. HWM’s financial performance is limited by the ability of aircraft manufacturers, such as Boeing and Airbus, to build and deliver aircraft.

In relation to Boeing, HWM does have concerns with Boeing’s production rate, especially the production rate of Boeing’s 737 and 787. Although Boeing reduced its parts orders, they still exceed the actual production rates of the 737 and 787 aircraft. On the other hand, Boeing has significantly trimmed its engine orders. Due to the ongoing challenges plaguing Boeing, uncertainty remains within HWM regarding Boeing’s inventory positions and the potential liquidation of this inventory.

In order to better reflect the Boeing challenge, HWM adjusted their expectations on the expected build rate for Boeing’s 737 aircraft. For context, in the previous quarter, the expectations were 20 aircraft per month for 2024. For 2Q24, this expectation has been increased to 22. The increase in expectation reflects some optimism regarding Boeing’s ability to address these issues moving forward. Looking ahead, once Boeing is able to overcome the production challenge, it will benefit HWM positively.

HWM Delivers Strong Q2 2024 Earnings Growth

For 2Q24, HWM reported robust earnings results. Revenue increased 14% year-on-year, driven mainly by the commercial aerospace market, which increased 27% year-over-year or 5% sequentially, and the defense aerospace market, which increased 11% year-over-year or 4% sequentially.

By reportable segments, engine products increased 14%, fastening systems were up 20%, and engineered structures increased 38%. On the other hand, forged wheels fell 4%, caused by lower volume and aluminium price. As discussed, the forged wheels segment only accounts for 15% of total revenue, so the impact is not as significant.

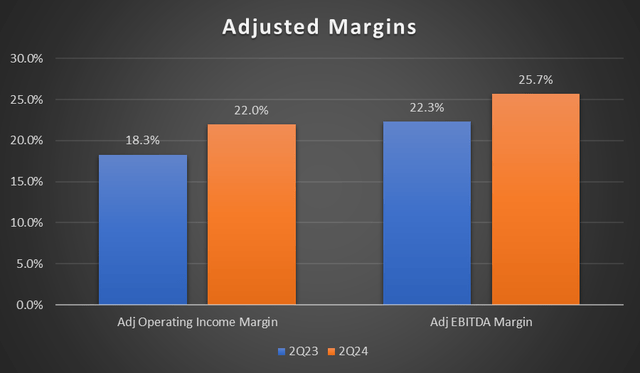

Moving on to margins, HWM reported robust figures. Starting with adjusted operating income margin, it expanded 3.7% from 18.3% to 22%. On to adjusted EBITDA, it increased 31% year-over-year to $483 million. This strong double-digit growth was attributed to strong growth in the commercial aerospace market. As a result, its adjusted EBITDA margin increased from 22.3% to 25.7%. Due to HWM’s strong top line growth and margin expansion, its adjusted EPS increased 52% year-over-year from $0.44 to $0.67.

Author’s Chart

Strong Engine Products Segment Performance

For 2Q24, HWM’s engine products segment reported strong results. For the quarter, revenue increased 14% year-over-year from $821 million to $933 million. This strong double-digit percentage growth was driven by growth in the commercial aerospace, defense aerospace, oil & gas, and industrial gas turbine markets. For context, commercial aerospace increased 18% while defense aerospace grew 10%, and both growth were driven by higher OE build rates and spares. On the other hand, the oil & gas market and industrial gas turbine markets grew 14% and 6%, respectively.

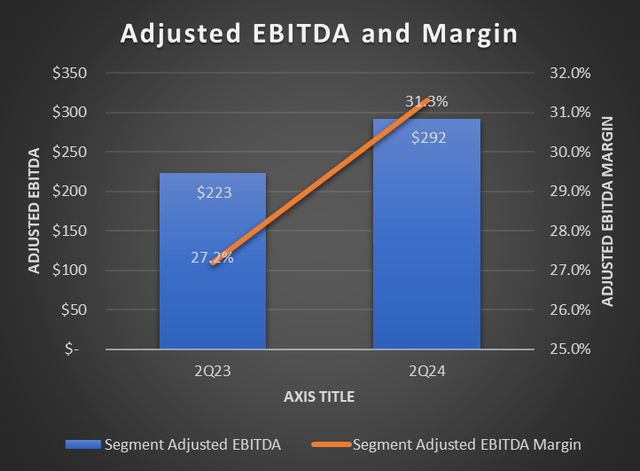

Moving on to engine products segment adjusted EBITDA and adjusted EBITDA margin, both metrics increased year-over-year. For the quarter, engine products segment adjusted EBITDA increased 31% from $223 million to $292 million. In terms of adjusted EBITDA margin, it expanded from 27.2% to 31.3%. The growth in both adjusted EBITDA and adjusted EBITDA margin were driven by growth in commercial aerospace, defense aerospace, oil & gas, and industrial gas turbine markets.

Author’s Chart

Relative Valuation Model

Author’s Relative Valuation Model

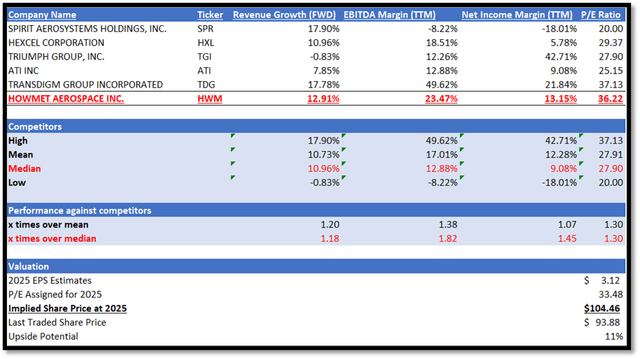

HMW operates in the aerospace and defence industries. In my relative valuation model, I will be comparing HWM against its peers in terms of growth outlook and profitability margin trailing twelve months [TTM]. For growth outlook, I will be comparing their forward revenue growth rate, which is a forward-looking metric. For profitability margins TTM, I will be comparing their EBITDA margin TTM and net income margin TTM.

Starting off with growth outlook, HWM outperformed its peers’ median. HWM reported forward revenue growth rate of 12.91%, which is 1.18x over the peers’ median of 10.96%. In terms of profitability margin TTM, HWM also outperformed peers’ median in both EBITDA margin TTM and net income margin TTM. HWM has an EBITDA margin TTM of 23.47%, higher than peers’ median of 12.88%. For net income margin TTM, HWM reported 13.15%, higher than peers’ median of 9.08%. HWM’s EBITDA margin TTM and net income margin TTM are 1.82x and 1.45x over peers’ median, respectively.

Currently, HWM has a forward non-GAAP P/E ratio of 36.22x, higher than peers’ median of 27.90x. Given HWM’s strong outperformance in both forward revenue growth rate and profitability margins TTM, I argue that it is fair for HWM to have a higher P/E ratio. However, in order to remain conservative, I will set my 2025 target P/E for HWM slightly below its current level.

For 2024, the market revenue estimate for HWM is approximately $7.46 billion, while EPS is $2.59. For 2025, the market revenue estimate is approximately $8.15 billion, while EPS is $3.12. When analysing its 2Q24 earnings result, HWM did provide guidance for FY2024. Starting with revenue, it is forecast to be in the range of $7.4 billion to $7.48 billion. Adjusted EBITDA is forecast to be in the range of $1.855 billion to $1.875 billion, which implies that adjusted EBITDA margin will be approximately 25.1%. Lastly, adjusted EPS is forecast to be between $2.53 and $2.57.

Taken together, HWM’s FY2024 guidance and my forward-looking analysis as discussed support the market’s estimates. Therefore, by applying my 2025 target P/E for HWM to its 2025 EPS estimate, my 2025 target share price is $104.46.

Risk and Conclusion

The risk associated with HWM stems from its reliance on a small group of suppliers for essential materials needed for its operations. Currently, HWM only purchases goods and services, including raw materials, from a small number of suppliers. For specialised metal alloys and raw materials like titanium sponge, HWM relies on a small pool of suppliers or one main source.

While most of its supply requirements are covered by annual or long-term contracts, the remaining requirements are contingent upon spot purchases. As in the case of most contracts, there is no guarantee of renewing them on favourable terms or at all. In addition, HWM may be compelled to acquire materials and supplies from alternative sources, which may not be available in sufficient quantities or at prices that are advantageous to them, if any of its suppliers are unable to deliver due to difficulties.

Additionally, according to Federal Aviation Administration [FAA] update on Boeing Oversight Actions, the latest updates stated that FAA is still actively monitoring Boeing’s progress. FAA did not provide a specific timeline for when the production cap on Boeing’s 737 MAX will be lifted. The cap will remain in force until Boeing demonstrates improvements in safety and quality.

HWM’s most recent 2Q24 results were strong as revenue increased mid-teens year-over-year, driven mainly by the strength of the commercial aerospace market. In addition, its 2Q24 adjusted margins also expanded year-over-year. As a result, its adjusted EPS increased 52% year-over-year from $0.44 to $0.67.

Looking ahead, HWM’s outlook remains favourable, as data published by ICAO indicates that air travel demand continues to be robust. Although Boeing is still grappling with production challenges, HWM remains cautiously optimistic and has increased its expectations for the build rate of Boeing’s 737 aircraft. Overall, HWM performed strongly for the quarter.

Read the full article here

")

")