")

")

")

Annexon, Inc. (NASDAQ:ANNX) is a clinical-stage biopharmaceutical developing innovative therapies targeting the classical complement pathway, particularly the C1q protein. When this pathway is overactivated, it can lead to an inflammation cascade that produces tissue damage. ANNX’s pipeline spans three areas: autoimmune diseases, neurodegenerative conditions, and ophthalmology. ANNX’s strategy aims to benefit a diverse range of complement-mediated illnesses. Recently, its announcement of promising Phase 3 results of ANX005 for treating Guillain-Barré syndrome [GBS] sets the stage for a potential FDA submission. ANX005 showed it expedited recovery with durable benefits and overall disability reduction with a favorable safety profile. Ultimately, I rate ANNX a speculative “buy” due to its potential in GBS, which is still contingent on the upcoming comparability study data by yearend.

GBS Focus: Business Overview

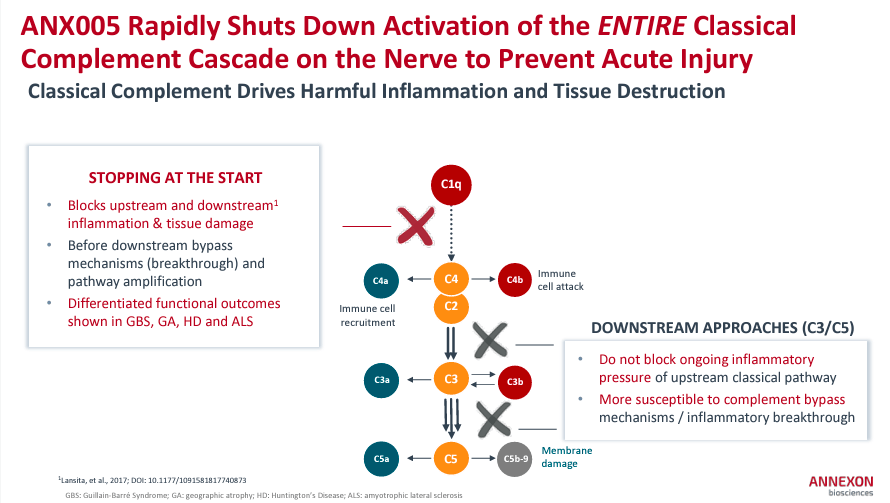

Annexon is a clinical-stage biopharmaceutical company founded in 2011 and based in Brisbane, California. The company’s therapies for inflammatory-related conditions target the classical complement pathway, specifically the C1q protein. Interestingly, the classical complement pathway is a part of the immune system that can produce excessive inflammation if overactivated. Activated C1q triggers a cascade of immune reactions that provoke inflammation. Therefore, inhibiting abnormal activation of this protein can potentially stop the classical complement pathway inflammatory elements, halting them before they hurt patients.

Source: Corporate Presentation. August 2024.

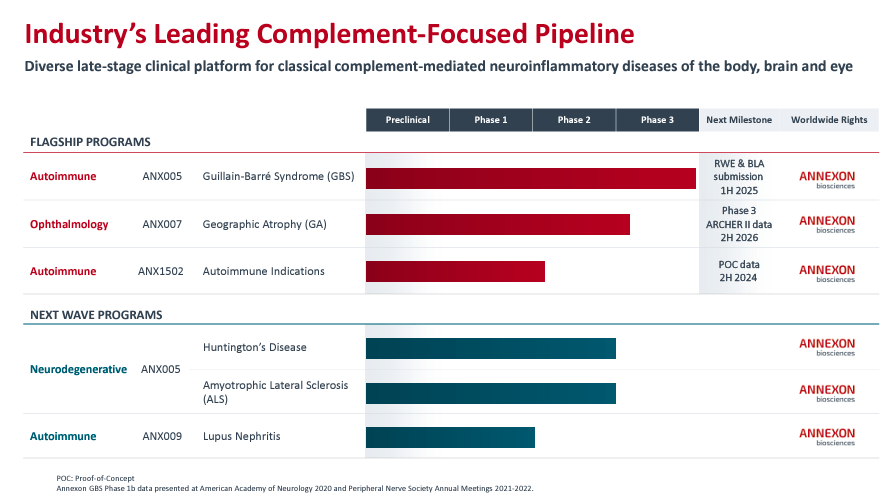

Currently, ANNX’s platform focuses on three distinct therapeutic areas. The first area is autoimmune diseases like Lupus Nephritis [LN]. The second area targets neurodegenerative conditions, including Huntington’s disease [HD] and Amyotrophic Lateral Sclerosis [ALS]. The third area is ophthalmology, addressing illnesses like geographic atrophy [GA], where C1q-driven inflammation leads to the deterioration of retinal cells.

Autoimmune Product Pipeline

Additionally, ANNX’s flagship drug candidates are ANX005, ANX007, and ANX1502. ANX005 is a Phase 3 intravenous monoclonal antibody [IV mAb] indicated for treating GBS. I believe this is ANNX’s main value driver, and a successful Phase 3 trial with a reasonable safety profile would be a Biologics License Application [BLA] submission by 1H2025.

Source: Corporate Presentation. August 2024.

The company’s second candidate, ANX007, is an intravitreal [IVT] fragment antigen-binding [Fab] for GA. This means ANX007 is an intravitreal injection in the back of the eye that binds the C1q protein to protect the retina’s photoreceptors. ANX007’s Phase 3 will start in 2H2024. Lastly, the company’s third leading drug candidate, ANX1502, is a Phase 1 oral low-molecular-weight organic compound. ANX1502 is indicated for autoimmune conditions and benefits from its relatively small molecule that facilitates its entry into cells. Its Proof of Concept [POC] data is expected by 2H2024.

Beyond the previously mentioned drug candidates, ANNX’s pipeline is also working on next-wave programs. In particular, the company is exploring expanding ANX005’s indications into HD and ALS. Essentially, ANX005 from the flagship program is being repurposed for different indications. ANX005 for HD and ALS is in Phase 2b/3 clinical trials and is relatively advanced. The other next-wave program is ANX009, a subcutaneous Fab for LN administered via injections for gradual absorption.

ANX005 Analysis: Prospects and Limitations

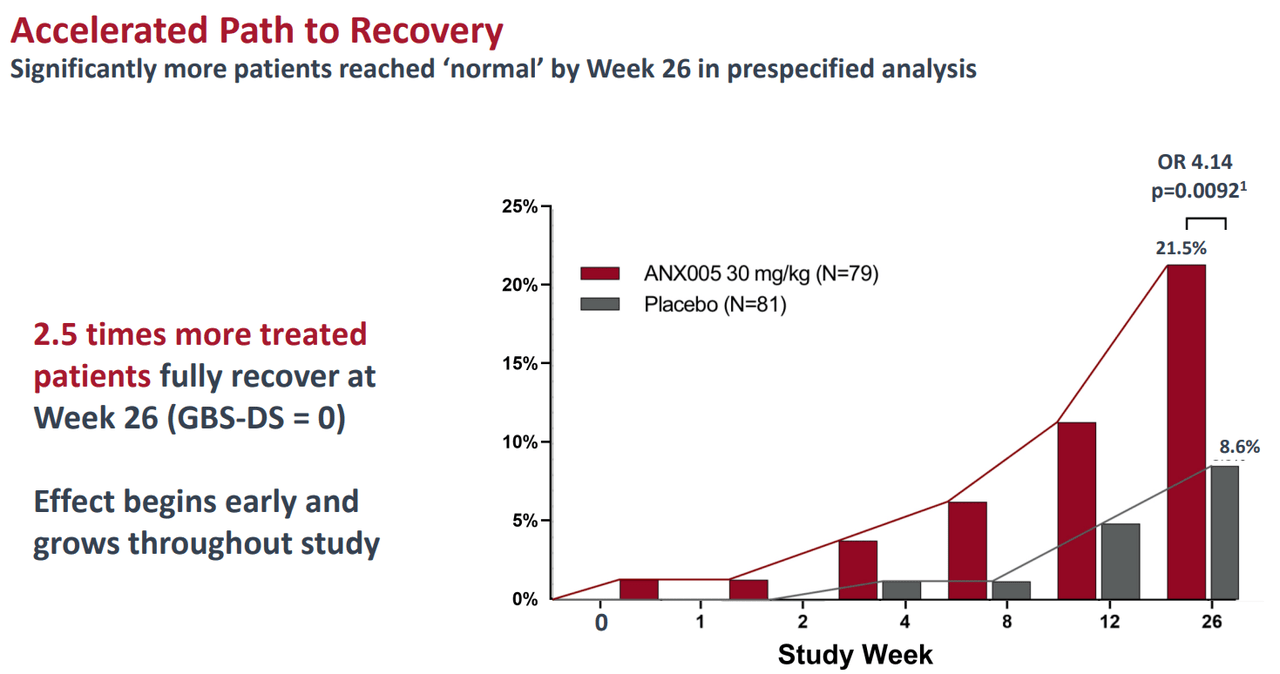

ANX005’s Phase 3 trial met its primary endpoints for GBS, achieving a statistically significant p-value of 0.0058. The data showed that patients treated with ANX005 were 2.4 times more likely to improve on the Guillain-Barré Syndrome Disability Scale [GBS-DS] at Week 8 compared to placebo.

Source: Corporate Presentation. August 2024.

It’s worth mentioning that GBS is considered a post-infectious autoimmune disease and generally develops after the body’s immune response mistakenly targets peripheral nerves. Thus, post-infection, GBS causes symptoms typically after 1-3 weeks. Nerve damage from GBS usually starts with weakness and tingling in the legs. However, if left untreated, GBS worsens as it spreads to the rest of the body. Eventually, GBS can cascade into varying degrees of paralysis. Unfortunately, some GBS patients even require mechanical ventilation due to respiratory muscle weakness. This is why ANNX’s Phase 3 results could represent a breakthrough for GBS treatment.

Patients using ANX005 experienced clinically significant benefits, such as walking and running earlier than those on placebo by Week 8. The trial showed that ANX005 reduced nerve damage, and patients requiring respiratory support spent less time on ventilation. Some patients also experienced a reduction in general disability symptoms. More importantly, ANX005 seems to have lasting benefits with a favorable safety profile compared to a placebo. This suggests ANX005 might also help prevent Chronic Inflammatory Demyelinating Polyneuropathy [CIDP] as a result of GBS relapses.

Source: Comparative Efficacy Presentation. June 2024.

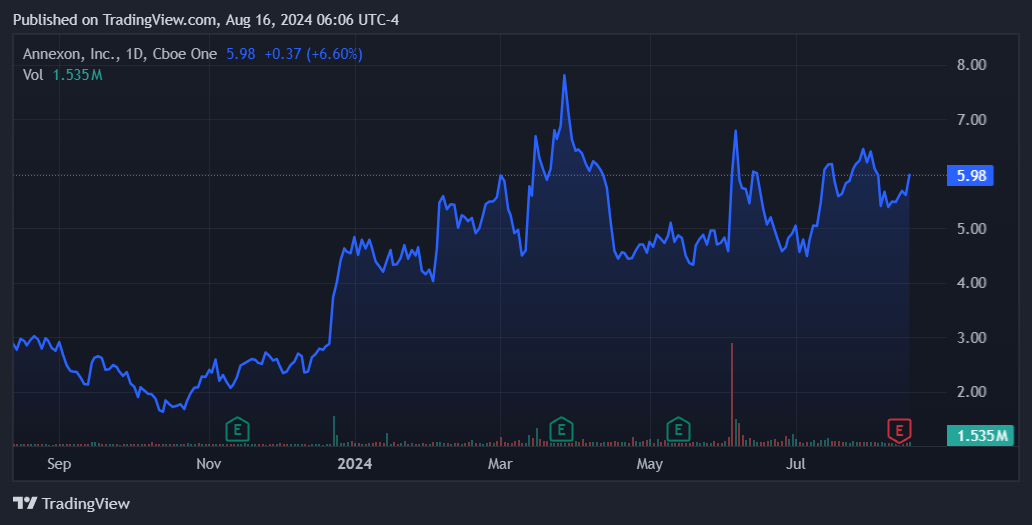

However, understanding the current standard of care is key because GBS already has a patient recovery rate of about 70%. The latest Phase 3 trial results suggest ANX005 could potentially produce a higher recovery rate, but it was only compared against a placebo, which could be a limitation. Since ANNX announced those results, its shares have traded higher, suggesting the market is also optimistic about its approval odds and potential market adoption. Nevertheless, the current standard of care for GBS focuses mostly on IVIg and plasmapheresis. ANX005’s effects likely overlap with IVIg’s, but IVIg offers a broader approach by modulating general immune response processes. Plasmapheresis focuses on filtering the patient’s blood to reduce harmful antibody concentrations. Thus, on paper, ANX005’s targeted C1q inhibition looks like a promising complement to IVIg and plasmapheresis.

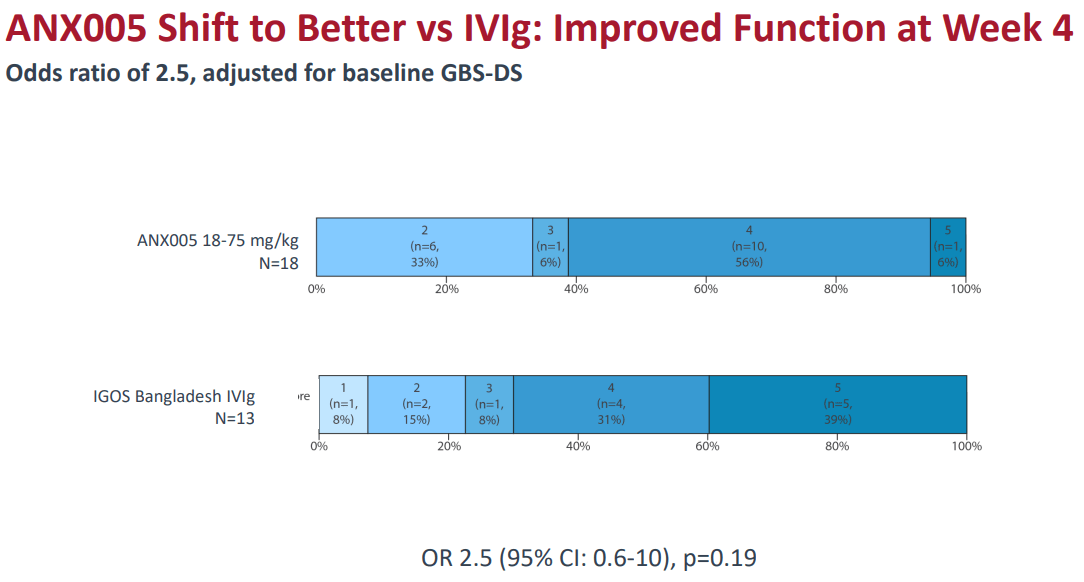

ANNX offered indirect comparative data between IVIg and ANX005 using data from Phase 1b and an unrelated IVIg study from Bangladesh. ANX005 demonstrated statistically significant muscle improvement at Week 1 compared to IVIg. However, by Week 4, the p-value was 0.19, indicating that the results were not statistically significant compared to IVIg. So, whether care providers add ANX005 to treatment regimens solely based on these limited comparisons remains to be seen. My impression is that ANX005 is likely highly effective at the early stages of GBS, as it prevents neuronal damage. Yet, GBS requires long-term care, and so far, I don’t think there’s as much evidence supporting ANX005’s superior effectiveness over that time frame.

Compelling Price: Valuation Analysis

From a valuation perspective, ANNX trades at a $592.7 million valuation, making it a relatively small biotech in its sector. Its balance sheet holds $157.3 million in cash and equivalents and $211.4 million in short-term investments. This amounts to $368.7 million in available short-term liquidity against $45.0 million in total liabilities. ANNX’s book value stands at $361.1 million, implying a P/B of 1.6. This looks cheap compared to its sector’s median P/B of 2.4.

Source: KBV Research.

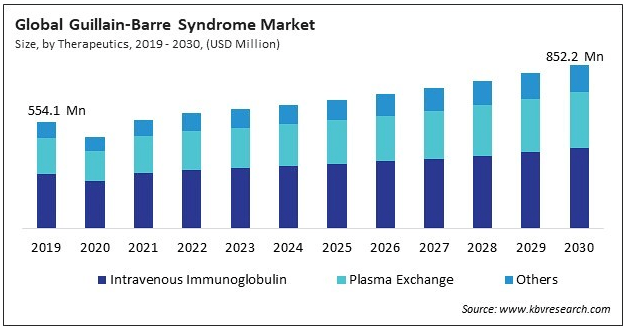

Moreover, I estimate the company’s latest quarterly cash burn was $21.7 million by adding its CFOs and Net CAPEX. This would suggest 4.2 years in cash runway, which I consider healthy for a company with a late-stage drug with a realistic chance of getting FDA approval. It’s also worth mentioning that the GBS market is forecasted to reach $852.2 million by 2030. So, even if ANX005 is mostly viable as a complementary treatment, it would likely still have a sizeable TAM. This, coupled with the stock’s relatively cheap valuation and promising research progress, nudges me towards a “buy” rating.

Investment Caveats: Risk Analysis

I think the company has enough resources to finance its research on ANX005 and potential FDA approval. Its clinical trial data indicates that it’s effective and relatively safe. However, the key variable now lies in how effective ANX005 is compared to the current standard of care, not just a placebo. ANNX expects to deliver initial topline data from a new comparability study with IGOS by late 2024. Ideally, this will support its BLA submission by 1H2025. However, I suspect the market’s reaction will hinge on how it compares to other treatment alternatives rather than its standalone effectiveness. So far, my impression is that ANNX’s communications focus on ANX005 as a potential standalone treatment. Still, the reality is that GBS already has a well-defined and reasonably effective treatment regimen.

Source: TradingView.

Moreover, ANNX recently filed an equity offering of 3 million shares, which could add some headwinds to the stock price. However, I believe the main variable will be how effective ANX005 is compared to treatment alternatives, as its potential inferiority could lead to significant shareholder losses. In fact, that could be a considerable setback to ANNX’s main value driver, and this risk cannot be entirely discounted based on the data available today. Nevertheless, I think ANX005 targets a large market, so it’s likely that even in the worst-case scenario, it will still be useful in some GBS cases. Its effectiveness seems impressive, especially in the early stages of GBS, and it has a unique mechanism of action. Thus, I believe a speculative ‘buy’ rating makes sense for ANNX at its current valuation.

Speculative Buy: Conclusion

Overall, ANNX is a promising biotech focused on inflammatory-related conditions. Its main value driver is ANX005, and its clinical trial data suggests it has favorable approval odds. However, I noticed that ANX005 has limited comparability data, which will likely be a key factor in determining its competitive profile if approved. Nevertheless, GBS is a huge market, and ANX005 has appeared relatively effective. Thus, I think there’s a viable investment case for ANX005, even as a complementary treatment in some GBS cases. The main risk is its upcoming comparability data by year-end 2024, as it’ll determine ANX005’s true potential. But overall, I think ANNX is a viable speculative ‘buy’ for investors who understand the clinical trial risk leading up to the announcement of the top-line data.

Read the full article here

")

")