")

")

")

")

Gladstone Commercial Corporation (NASDAQ:GOOD) is a well-managed commercial real estate trust with considerable investments in office and industrial properties.

Gladstone Commercial solidly covered its dividend with funds from operations and collected 100% of its cash rent in the second quarter. In my view, it is particularly the industrial angle that makes Gladstone Commercial promising as a real estate investment for passive income investors.

Taking into account Gladstone Commercial’s 83% dividend pay-out ratio in the second quarter, I don’t see any elevated risks for the real estate investment trust’s 8% dividend yield.

The stock is also selling at a compelling FFO multiple, and Gladstone Commercial’s higher dependence on industrial properties could be a catalyst for FFO growth as well as a higher margin of safety moving forward.

My Rating History

My last stock classification for Gladstone Commercial was Buy. The trust has solid dividend pay-out metrics and performs rather well in terms of rent collection.

The focus on industrial properties also helps skew the risk/reward relationship in favor of the trust, in my view, and I think that the industrial segment profits from favorable tailwinds in the industry. The 8% dividend yield also appears to be sustainable for the remainder of 2024.

Portfolio And Rent Collection

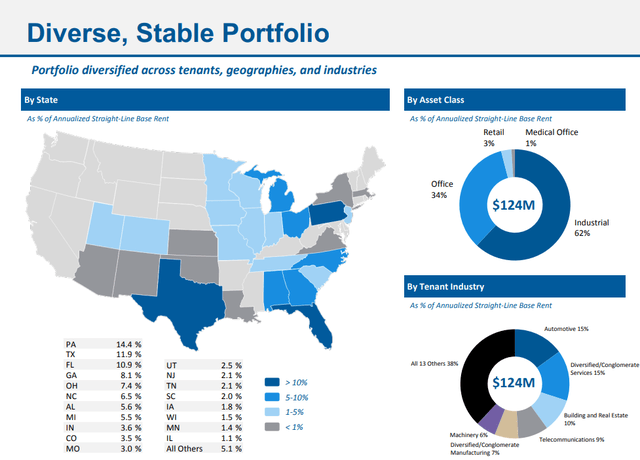

Gladstone Commercial’s real estate portfolio consists predominantly of office and industrial properties, which the company leases to corporations in 27 states (it owned a small number of properties in the retail and medical office markets as well).

The real estate investment trust owned 136 properties as of June 30, 2024, reflecting 16.8 million square feet, which were leased primarily to tenants in the Automotive, Diversified Services, Real Estate and Telecommunications industries.

Portfolio Overview (Gladstone Commercial Corporation)

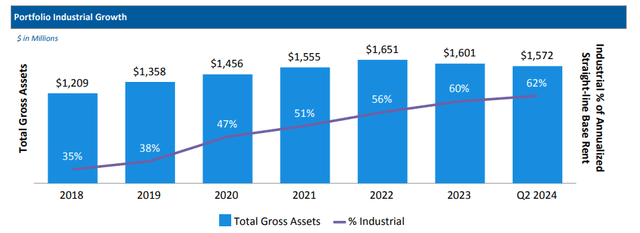

Gladstone Commercial has implemented a strategic policy of growing its industrial real estate footprint (at the expense of offices) amid more positive supply and demand dynamics in the industrial market.

The office real estate market is under considerable pressure, with the ability of people to work from home affecting office building occupancy negatively.

Industrial properties, on the other hand, profit from restoring initiatives as well as strong growth driven by the eCommerce industry.

As of June 30, 2024, Gladstone Commercial produced 62% of its annualized rent from its industrial real estate portfolio, which is up 15 percentage points since 2020 when the pandemic hit. The real estate investment trust has laid out a target to grow this percentage to 70% in the next 18 months.

Since industrial properties are in high demand, Gladstone Commercial potentially could see an acceleration of its FFO growth in the coming quarters, which might also improve the trust’s margin of dividend safety.

Portfolio Industrial Growth (Gladstone Commercial Corporation)

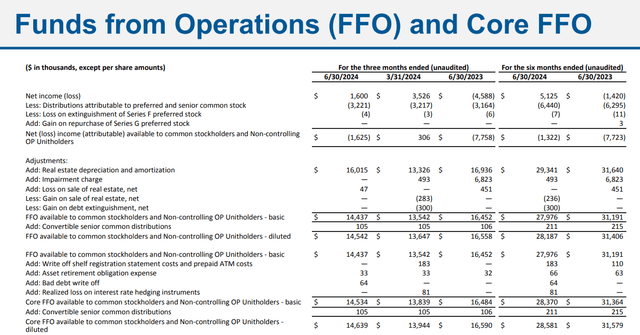

Gladstone Commercial’s second quarter showed a decline in funds from operations on a YoY basis, which was due to the real estate investment trust selling non-core real estate in an attempt to remove office risks out of its portfolio. In 2Q24, Gladstone Commercial’s core funds from operations decreased 12% YoY to $14.6 million.

In the short term, the real estate investment might continue to sell off office properties and invest proceeds in industrial properties, and thus passive income investors must anticipate a decline in the trust’s FFO basis.

In the long term, however, I think this strategy makes sense for Gladstone Commercial as the office market continues to struggle and the industrial market seeing growing demand for properties.

Funds From Operations (Gladstone Commercial Corporation)

Dividend Coverage

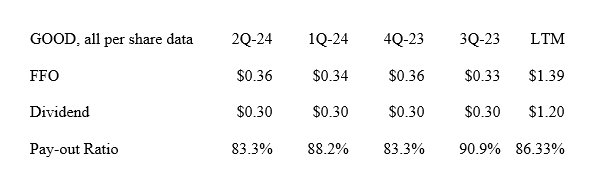

Gladstone Commercial earned $0.36 per share in core funds from operations in the second quarter, down 12% YoY, primarily due to the divestment of non-core office buildings. The business development company paid out a stable $0.30 per share in 2Q24 (the dividend is paid monthly), however, which equates to a dividend pay-out ratio of 83.3%. The dividend, based on current run-rate funds operations, is well-covered by FFO.

Though I don’t see the dividend at risk of getting chopped based on the present dividend pay-out metrics, a further shift towards industrial properties, could increase the margin of safety for the trust moving forward. Industrial real estate is in high demand, particularly from the eCommerce industry, which points to strong asset utilization and positive FFO growth.

Dividend (Author Created Table Using Company Supplements)

Cheap FFO Multiple

The commercial real estate investment trust has annualized core FFO potential of $1.39 per share, based on LTM funds from operations, and $1.44 per share based on 2Q24 run-rate funds from operations.

With the stock presently selling for $14.67, the valuation implies a 10.3x core FFO multiple. STAG Industrial Inc. (STAG), which is a pure-play industrial REIT, is selling for 16.2x 2Q24 run-rate core funds from operations. STAG also profits from growing real estate investments into warehouses and distribution centers due to the overall growth of the eCommerce industry.

From a valuation angle, I prefer Gladstone Commercial. However, if higher industrial property exposure is critical to you, STAG Industrial might be the better choice for you.

Why The Investment Thesis Might Not Pan Out

Gladstone Commercial still has exposure to offices and there is a risk, as I suggested, that the trust’s funds from operations might continue to slide due to non-core asset sales in the short term.

With that being said, though, I don’t think passive income investors have to lose sleep here over the dividend, which is well-covered by FFO and has been so consistently in the last four quarters.

My Conclusion

Gladstone Commercial collected 100% of its cash rent in the second quarter (as well as in July) and had no trouble whatsoever to cover its $0.30 per share dividend with funds from operations. Even with a 12% YoY drop in core funds from operations, the dividend was well-covered.

The trust also laid out its goal of growing its industrial properties at the expense of its office properties, which means Gladstone Commercial is more than likely to sell more real estate moving forward, which, in the short-term, may trigger a further dip in core funds from operations.

In the long term, however, this strategy should pay off as industrial real estate assets are in higher demand and have stronger income potential. Buy.

Read the full article here

")

")

")

")