")

")

")

")

Overview

As a dividend focused investor, it can be difficult to find a source of high yielding income from the tech sector. Tech companies are generally known to reinvest their earnings back into their business rather than distribute it to shareholders. This can expand earnings growth at a faster rate and this is why the large majority of tech companies do not pay any dividends. However, BlackRock Science and Technology Trust (NYSE:BST) solves this issue by providing a diverse exposure of holdings that are primarily rooted to the tech sector. The share price has fallen a bit over the last month and I believe this presents an attractive opportunity for both existing shareholders and potential new investors.

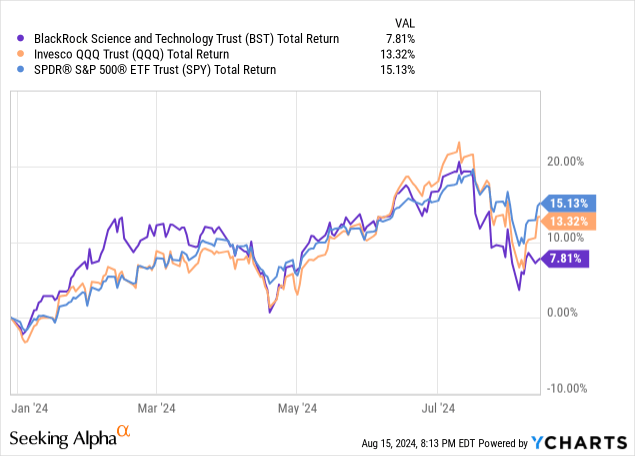

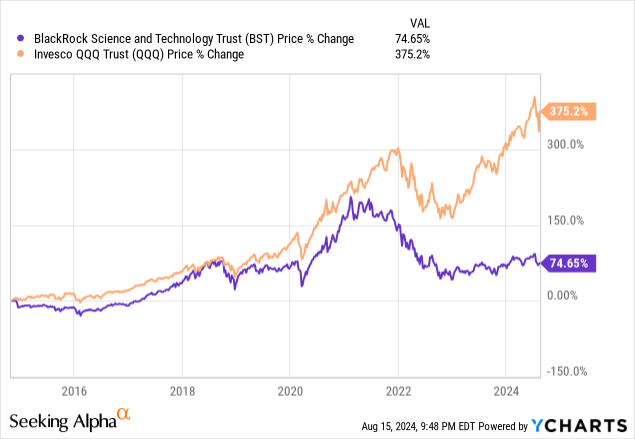

As we can see, BST has underperformed both the Invesco QQQ Trust (QQQ) and the S&P 500 (SPY) in total return on a year to date basis. I also observe that BST is currently trading at an attractive discount to net asset value. I previously covered BST back in early May and issued a buy rating do to its consistent performance and attractive income potential. BST has a sizeable dividend yield of 8.7% that is well-supported through its portfolio strategy of holdings. A bonus is that the distributions are paid out to shareholders on a monthly basis and this makes BST an attractive fund for investors that like to prioritize income generation in their portfolio.

Just to provide some brief context, BST operates as a closed end fund with a public inception dating back to 2014. Therefore, we have a decade of prior performance to use as a reference point. The fund has a primary objective of providing a total return comprised of current income and long term capital appreciation. The emphasis here is on income and as such, the fund implements a covered call option strategy to help generate additional income against the underlying assets as a way to fund the distribution. The fund holds the majority of its exposure to US-based companies, but there are some slight exposures to international markets such as the Netherlands, The United Kingdom, or Taiwan. The fund is managed by BlackRock and sports a total management fee of only 1%.

Attractive Valuation

What prompted me to revisit BST the most is the fact that the price currently trades at a relatively large discount to NAV (net asset value). Since BST operates as a closed end fund, the price can vary from the actual underlying value of its net assets. The price of BST currently trades at a discount to its NAV of 6.7%. For reference, the fund has only traded at an average discount to NAV of 1.35% over the last three-year period. Therefore, this could be a great time to scoop up shares.

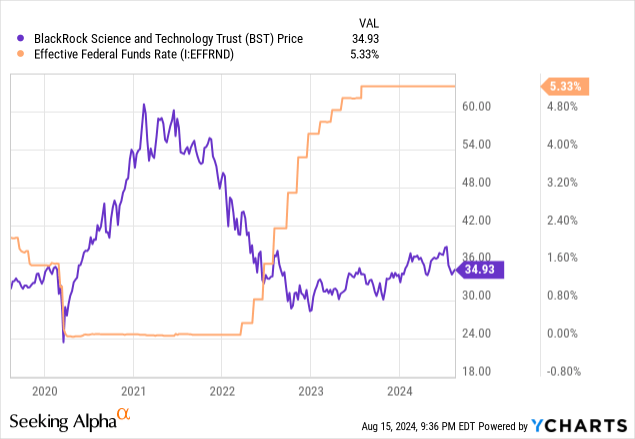

Looking at the chart below, we can see the ten-year history of its price in relation to the NAV. The price has only traded at this level of a discount a few times in its recent history. The last time BST regularly traded at a large discount to NAV on a regular basis was back in 2018. After this point, we can see that the price traded in the premium territory for most of 2019 through 2021. However, I believe that the conditions around interest rates have a lot to do with the price action of BST.

CEF Data

This can be reinforced that even the price movement has shared an inverse relationship to the federal funds rate. We can see that when interest rates were cut to near zero levels in response to the pandemic, the price of BST rapidly moved upward as this environment encouraged the use of debt to fund operational growth and expansion efforts of businesses. For example, in a low rate environment, tech companies were able to gain access to debt that could be used to fund the research and development of new products and innovations to fuel higher revenue levels.

Conversely, we can see that the price quickly retracted to the downside once the Fed begin aggressively raising interest rates throughout 2022 and 2023. As interest rates were hiked to their decade high, growth and valuations across sectors dropped. Higher interest rates can directly translate to lower operating and profit margins, and it now become more expensive to hold debt on the balance sheet. As a result, this caused companies to shift their focus to more of a defensive outlook by focusing on capital efficiency and cost-cutting measures rather than growth.

I mention interest rates because I feel that recent economic data may indicate a change coming. I believe that interest rates will begin to get cut soon and this may serve as a positive price catalyst for BST. For instance, the unemployment rate has steadily increased over the last twelve month period and now sits at the 4.3% level. As more households cut back their spending, the Fed may need a way to stimulate the economy. Additionally, the inflation rate has consistently trended downward for four consecutive months and now sits at 2.9%. This is getting much closer to the Fed’s 2% inflation target.

Not to mention, we also have the US Presidential elections upcoming to close off 2024. As the world awaits the outcome of elections, I anticipate the markets to see higher levels of volatility and uncertainty. The combination of these factors may be enough of an incentive for the Fed to begin cutting interest rates. This would be a positive catalyst for the market and I think there is a strong likelihood that the underlying assets in BST will appreciate in value in response. Therefore, I have continued to accumulate additional shares and fully reinvest all distributions to build my position before rate cuts take place.

Portfolio Strategy

It should be understood that BST is primarily a technology focused fund. You instantly gain exposure to some of the best large cap companies in the world with an investment in BST and as a result, this can increase the likelihood of experiencing a bit of capital appreciation. We can see that over 81% of the fund is comprised of this tech exposure. More specifically, this exposure can be broken down into varying weights spread across the semiconductor, software services, and tech hardware sub sectors according to the most recently posted fact sheet. The largest tech related exposure is broken down as follows:

- Semiconductor & Semiconductor Equipment: 37.2%

- Software & Services: 32.3%

- Tech Hardware & Equipment: 10.3%

Seeking Alpha

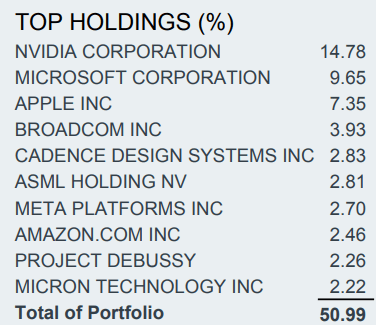

We can see that BST also maintains some exposure to communication companies, accounting for 7.38%. This is followed by varying weights in Consumer cyclicals, Financials, and Industrials. The fund is made up of 96 different holdings and has total assets amounting $1.35B. Taking a look at the top holdings, Nvidia (NVDA) currently makes up the largest individual position at 14.78%. This is closely followed by positions in Microsoft and Apple, accounting for 9.65% and 7.35% of the fund respectively. The top ten holdings make up approximately 51% of the total assets within. The fund seems to favor large cap holdings valued greater than $10B.

BST Fact Sheet

Despite all of the exposure to tech, you have likely noticed that BST’s price movement has been lacking compared to something like Invesco’s QQQ Trust (QQQ). This is can attributed to the fact that BST implements a covered call option writing strategy to help generate higher levels of income. BST does implement a single stock option writing strategy however, with the ability to sell covered call options on individual stocks within its portfolio. While the higher levels of income are great, it comes with a trade off of lower capital appreciation. While I searched throughout all of Blackrock’s listed documentation for BST, I could not locate whether the fund uses an at-the-money or out-of-the-money option strategy.

My personal preference here would be that BST implement an OTM option strategy because this would allow for a greater amount of capital appreciation to be experienced in comparison to an ATM approach. Regardless though, the inclusion of an option strategy does cap the possible upside that can be experienced. OTM option strategies means that the strike price is set a bit further away from the underlying asset’s current price.

As an example, let’s imagine that BST writes an option with a strike price at $110 per share for an underlying equity currently priced at $100 per share. If the underlying equity rises to $115 per share, the option will be executed at the strike price of $110 for BST and that extra $5 difference in gains would be missed. I hope this helps illustrate how the upside price movement can be capped. A negative side of this option strategy is that you would be getting limited upside potential but still experiencing the effects of a price retraction downward.

Distribution Insights

Something that I like about BST is the fact that the distributions are issued on a monthly basis. This can be beneficial for investors that may depend on the income generated from their portfolio, such as retired investors. This adds a bit of flexibility and can make it psychologically easier to remain invested during market downturns. As of the most recently declared monthly dividend of $0.25 per share, the current dividend yield sits at 8.7%.

Despite the yield already being higher than average, the fund has experienced some dividend growth throughout its history. For instance, the monthly distribution rate before the pandemic in 2019 sat at a rate of $0.15 per share. This was increased several times over the course of the pandemic and serves as a testament to the fund’s performance. The dividend managed to ultimately increase at a CAGR (compound annual growth rate) of 9.79% over the last five year period.

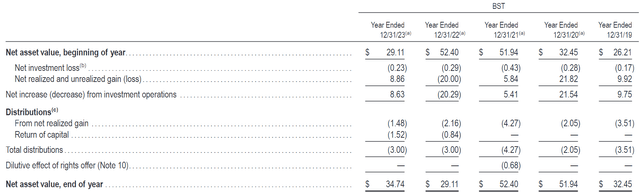

This rate of dividend growth prompted me to take a look at the most recent 2023 annual report for BST to see what the distribution is comprised of. We can see that it has been supported by mostly net realized gains from the underlying assets. Unfortunately, it seems like BST continues to rake in losses from net investments. In 2023 NII per share landed at -$0.23 and this has been a common theme over the last five years. Therefore, BST’s distribution growth is highly dependent on net realized gains from the underlying portfolio of holdings. The most recent annual distribution sat at $3 per share which means that the fund has to surpass this in earnings in order to effectively grow NAV.

BST 2023 Annual Report

We can see that realized gains totaled $8.86 per share for 2023. However, the prior year suffered losses of $20.00 per share but this comes as no surprise as the overall market experienced a correction throughout most of 2022. As a result, we can see that the fund’s NAV dropped by nearly 40% by the end of 2022. This makes BST highly vulnerable to general market performance and it doesn’t seem like the income generated from the option strategies has helped offset this weakness.

We can see that the fund has implemented the use of return of capital over the course of 2022 and 2023 to help fund the distribution. However, I am not too concerned with this since the fund still managed to out earn the distribution from net realized gains by itself. As long as the realized gains outweigh the distribution amount, BST should be able to retain enough earnings to help grow NAV over time.

Vulnerabilities

Despite the large tech exposure, it needs to be understood that BST is best utilized as an income investment. The inclusion of option strategies severely caps the upside price appreciation experienced here. We can see that BST significantly underperforms QQQ over a longer time frame. While the price growth of BST since its inception is still impressive for a closed end fund, QQQ returns a price growth greater than 5x of BST.

Not to mention, the option income generated from BST may also make the distributions received from BST a bit less tax efficient. Income generated from funds that include option strategies is generally classified as ordinary dividends. Ordinary dividends have less favorable tax consequences than the qualified dividends you would get from a more traditional dividend growth stock or ETF. Therefore, an investment in BST might be best utilized in a tax advantaged account based on your situation.

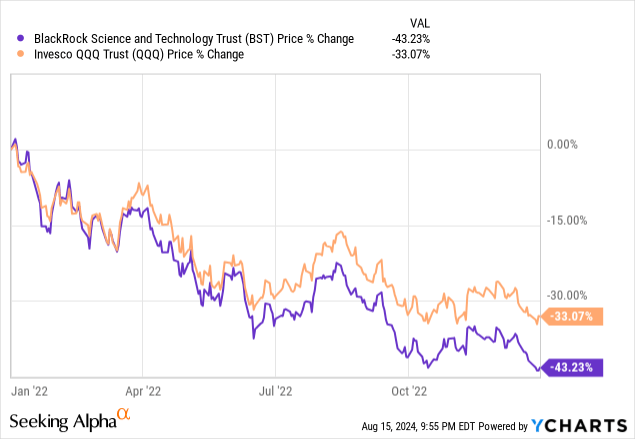

Lastly, BST remains sensitive to downward swings in the market, judging from the net realized losses captured in poorly performing years. As mentioned, realized losses in 2022 amounted to $20.00 per share. If we compare the price decrease between BST and QQQ for the full year of 2022, we can see that BST actually held up a bit worse than QQQ.

Since the fund didn’t generate enough earnings to support the distribution, it had to use return of capital, which was likely pulled directly from the NAV of the fund. Therefore, we should be aware that this exact scenario can play out again if tech goes through a bear market and falls. If the fund cannot generate enough earnings to support the distribution, the distribution can either be reduced or the fund’s NAV can take a large reduction through the continued use of return of capital.

Takeaway

As a result, I maintain my buy rating on BST because of its underlying exposure to the tech sector and the ability to provide a high distribution income. I believe that future interest rate cuts are on the horizon and will serve as a positive price catalyst going forward. BST’s price and the federal funds rate have shared a bit of an inverse relationship and lowering rates can help the underlying assets grow more rapidly. If the underlying assets within BST continue to grow, there is an increased likeliness that the NAV will also grow. The monthly distribution makes the fund highly appealing for investors that value income, but there are some vulnerabilities around the fund’s continued use of return of capital. Despite this potential risk, the fund trades at a favorable discount to NAV and presents an attractive opportunity to accumulate.

Read the full article here

")

")

")

")