")

")

")

Introduction

The ‘Undercovered’ Dozen series highlights undercovered stocks on our platform for you to have another source for idea generation.

Today we’re looking at ideas published between August 9th – 15th.

Take a look at what these less-covered stocks might hold for you. And please join the conversation below to share what you think: are any of these worth following up on?

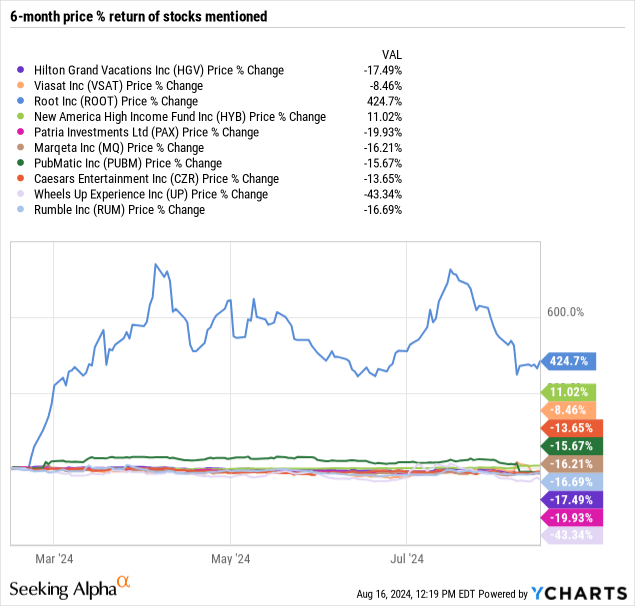

| Ticker | Rating | Analyst |

| HGV | Strong Buy |

PropNotes |

When it comes to investment opportunities, timeshares don’t exactly have the best reputation. Strict visitation schedules, high fees, and sketchy developers have given the industry a bad name – and for good reason. From a buyer perspective, timeshare contracts are notoriously hard to break, and selling a timeshare will often only net you pennies on the proverbial dollar.

However, in recent years, the industry has transitioned towards a points-based model, where an upfront buy-in gives a buyer an annually allotted number of points that they can use to book stays within a global network of resorts. The variable timeshares are still typically legal property (‘deeded’), but from a user perspective, the model operates more closely to a travel annuity – a lump sum paid up front, and ongoing value with minor fees attached as the product gets delivered year after year.

Today, we’ll take a closer look at one of the largest players in the space, Hilton Grand Vacations (HGV), and explain why we’re so bullish on this oft-overlooked area of the travel industry.

After Viasat, Inc. (VSAT) posted first-quarter results, the stock closed up by 37.82% on the day. I last covered this as a stock to buy but to wait for a pullback nearly a decade ago, will history repeat itself?

In Q1, Viasat reported a net loss of $33 million, down from $77 million in losses the year before. It attributed the improved operating performance to the smaller loss, offset by higher interest expenses and a lower tax benefit. Revenue grew by 6% Y/Y, thanks to the Defense and Advanced Technologies segment. Viasat’s aviation and government sitcom service revenues led to a growth in revenue in Q1.

Viasat’s potential prospects are vastly different than AST SpaceMobile (ASTS). They are comparable only in the stock price surging so quickly. The former is established in the high-speed satellite broadband service sector.

Root, Inc. (ROOT) is a property-casualty auto-insurer whose shares have seen impressive growth over the past year. Dealing in property-casualty for personal auto-lines, Root doesn’t exactly have a new insurance product to sell. Where they claim to have an advantage is in their data-driven approach that allows for more precise pricing. They claim to use a more unique risk model that prices based on causal factors (as opposed to correlation), one that rewards customers for good driving, while completely refusing to underwrite the riskiest drivers.

Since going public, they have been growing their business aggressively, suggesting there is some hope for them to become a contender in the auto-insurance. With Q2 results, we see that they have yet to report positive net income, but a turning point appears near. Similarly, they have finally reported an operating profit. These are good signs.

| HYB | Hold |

Binary Tree Analytics |

This article discusses the recent events surrounding the New America High Income Fund (HYB), a closed-end fund that historically traded at a discount to its net asset value. Activist hedge fund Saba Capital identified HYB’s discount as an arbitrage opportunity and took a position in the fund. Saba successfully pushed for a reorganization where HYB will potentially merge into the T. Rowe Price High Yield Fund (PRHYX), an open-ended mutual fund.

This corporate action significantly reduced the discount to NAV, causing a 7% jump in HYB’s price on August 9, 2024. The merger is subject to shareholder approval, expected in November 2024. Approval is likely, as it eliminates the discount.

Large funds like Saba can leverage their expertise and lawyers to take a large position in a CEF and then try to implement corporate changes in order to force the management company to take actions favorable to the shareholders. Ultimately, they do what small investors cannot, and when they are successful, all shareholders benefit, just like in this case.

| AGNCP | Hold |

Colorado Wealth Management Fund |

It’s been so long since there was an article about AGNC’s 6.125% Series F Fixed-To-Floating Rate Cumulative Redeemable Preferred Stock (AGNCP) that Seeking Alpha asked me to write an update. Since you, my dear readers, deserve quality, I’m fulfilling that request.

AGNCP is one of 5 preferred shares from AGNC Investment (AGNC). AGNC is a mortgage REIT investing in agency MBS (mortgage-backed securities). The debt to equity may seem high, but this is perfectly normal for an agency mortgage REIT. The agency mortgages are quite safe, aside from interest rate risk. The company hedges much of the interest rate risk. Consequently, when there is a big move in rates, the damage is absorbed by the common shareholders.

There is one exception to that statement. Because four of the preferred shares, including AGNCP, either have a floating-rate dividend or will have a floating rate dividend by the middle of 2025, a reduction in short-term rates means a reduced dividend rate. That part kind of stinks, but it’s a necessary part of “floating rate.” Specifically, it’s the rate and it’s the part that floats. Basically, it’s the whole thing. That’s how these shares work.

| PAX | Strong Buy |

Jussi Askola, CFA |

Many of you here on Seeking Alpha know me as a REIT analyst. REITs (VNQ) are my specialty, and I invest heavily in them because they are today priced at historically low valuations and essentially allow you to buy high-quality, professionally managed real estate at a heavily discounted price.

But just because I’m bullish on REITs does not mean that I invest all of my capital into them. The only free lunch in the capital markets is diversification, and you never want to be fully exposed to a single sector as it could become the victim of a black swan.

For this reason, I invest about 50% of my portfolio outside of the REIT sector, and right now, my biggest non-REIT investment is an asset management company called Patria Investments Limited (PAX). I have accumulated a lot more of it lately, and it has become one of my largest holdings in my entire portfolio, even larger than some of my biggest REIT investments.

| MQ | Strong Buy |

Riyado Sofian |

Marqeta, Inc. (MQ) — the modern card issuing and payment processing platform — just reported Q2 earnings that beat both analyst Revenue and EPS estimates, sending shares 8% higher the following day. While the post-earnings rally was a confidence boost for shareholders, it is worth noting that Marqeta stock is still down 80%+ from its IPO price of $27 a share. Back then, the company was valued at a Market Cap of $15B — today, it is worth less than $3B.

We can blame astronomical valuations and interest rate hikes as the main contributors to Marqeta’s valuation reset. But ever since the company IPOed, Marqeta has done nothing but execute and build on its business, landing customer after customer and processing more volume than ever.

Perhaps, one of the main reasons for this underperformance was the Block (SQ) contract renewal that was announced in Q2 last year, which completely distorted Marqeta’s financials, making it difficult for analysts and investors alike to put a valuation on the company. However, now that the Block contract renewal has been fully lapped, investors have more clarity regarding the fundamentals of the business, which could finally turn the stock around to the upside.

The Other Five Fit For Mention

PubMatic: Revenue Miss Sends Stock South, It Could Present An Opportunity

PubMatic, Inc. (PUBM) stock is down significantly after a revenue miss and guide-down raised concerns about the company’s ability to compete and gain share. Despite challenges, PubMatic’s recent big client wins and success in SPO suggest that they can, in fact, gain share. If growth initiatives bear fruit in 2025 and beyond, buying at the current price will look like a good move.

Caesars: WSOP Sale & Las Vegas Momentum Enable Accelerated Debt Deleveraging

| CZR | Hold |

Caffital Research |

Caesars Entertainment, Inc. (CZR) debt remains high after the COVID earnings slump and the 2020 merger, but debt paydowns should accelerate through improved cash flows. The sale of the World Series Of Poker brand should also aid in paying down debt, while the transaction still lets the Company leverage licensed brand assets from WSOP, including tournament hosting. Caesars’ stock valuation seems balanced but extremely volatile due to its extremely high debt.

Wheels Up: High Risk, High Reward; Catalyst In Place For Rebound

Shares of Wheels Up Experience Inc. (UP) erased recent gains after reporting Q2 results. The company has simplified its customer offering, while also adding new flier perks with Delta that may help to turn around membership trends. Margins have improved and losses are slimming as the company focuses its flight routes on a more profitable core, which better utilizes its maintenance and repair facilities.

Redwood Trust Recently Issued 2 Notes Maturing In 2029

Redwood Trust, Inc. (RWT) operates as a specialty finance company in the U.S., with a diverse portfolio including residential and multifamily investments. Investors have the opportunity to buy bonds maturing in 2029 at current interest rates, locking in today’s interest rates and YOC. My Buy rating goes to the Redwood Trust, Inc 9.00% Senior Notes due 2029 (RWTO) as having the best combination of yields and Call protection.

Rumble’s Litigation Against Google Is An Interesting Litigation Trade

Rumble Inc. (RUM) filed a second lawsuit against Google (GOOG) (GOOGL) in May 2024, and the 2021 lawsuit against Google is expected to go to trial in May 2025. Rumble and Elon Musk filed lawsuits against GARM, which closed down a few days after the lawsuit filings, for withholding ads for political reasons. Even a modest win against Google could have a significant positive impact on Rumble.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here

")

")

")

")