")

")

")

")

Topgolf Callaway Brands Corp. (NYSE:MODG) has been in for a turbulent ride – the company reportedly released its Q2 report prematurely for a moment. The final results were still reported on the 7th of August, showing a mixed financial performance in the quarter coupled with a very notable guidance shift downwards – underneath, Topgolf’s same-venue sales are deteriorating rapidly, understandably concerning investors.

The company has also now initiated a strategic review process, looking at alternatives for the Topgolf segment.

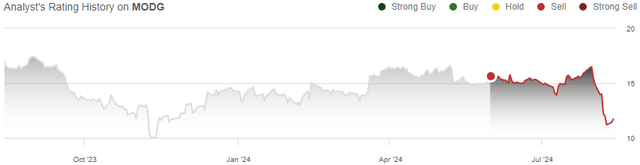

In my previous article on the stock, “Topgolf Callaway’s Growth Likely Isn’t On A Sustainable Foundation”, I expressed concerns of the incredibly high debt and poor cash flows amid Topgolf’s continued venue investments. After the article was published on the 31st of May with a Sell rating, the stock has now lost -25% of its value compared to S&P 500’s small return of 3% in the same period, as the stock fell primarily after the lackluster Q2 report.

My Rating History on MODG (Seeking Alpha)

Topgolf’s Same-Venue Sales Is a Notable Weak Point in Q2 Financials

Topgolf Callaway reported $1157.8 million in revenues in Q2 at a -1.9% year-on-year decline, similar to Q1’s -2.0% decline. The adjusted EPS came in at $0.42, up $0.04 year-on-year from improving Topgolf operating income. While revenues missed Wall Street analysts’ consensus by $33.4 million, the adjusted EPS came in at a surprisingly good level, beating the consensus by $0.15.

As Topgolf continues to open venues, the Topgolf segment’s revenues grew by 5.0% to $494.4 million. Driven by revenue growth and operating efficiencies, the segment’s operating income grew impressively by 27.5% to $56.1 million, despite same-venue sales shrinking -8%.

I think that Topgolf’s -8% same-venue sales performance is highly concerning, though – with the business model’s large amount of fixed costs, keeping up good traffic is critical over the longer term to sustain healthy earnings. The company reported a near-similar -7% figure in Q1, and has related the weakness to macroeconomic worries. Yet, Bowlero (BOWL) only reported a -2.1% same-store revenue growth in the Q1 period, and while Bowlero hasn’t yet reported the more recent results, Topgolf’s -8% Q2 performance seems likely to again underperform by a clear margin. Although Bowlero’s bowling and Topgolf’s golf venues aren’t the same, they should in my opinion perform similarly in relation to macroeconomic turbulence, providing a benchmark that Topgolf is deteriorating against. As such, Topgolf Callaway’s simple relation to macroeconomic cycles doesn’t seem to completely hold water, even though it clearly plays a part.

The Golf Equipment segment also showed a poor performance year-on-year at a -8.2% revenue decline into $413.8 million. I believe that the segment’s performance is better explained, though – in the prior year, Topgolf Callaway released Big Bertha clubs, making for a tougher comparison period in the segment. Acushnet (GOLF), a typically very well-growing golf ball & club manufacturer, also reported quite a weak -0.8% growth in Q2 driven by weak golf club sales. The segment’s operating income understandably fell by -19.7% into $77.4 million due to the weaker sales. I don’t believe that the Q2 decline is a worrying sign for the segment’s future, as the industry seems to show similar results.

The Active Lifestyle segment, on the other hand, showed a very good sequential improvement from a -15.2% revenue decline in Q1 into just a -3.2% decline in Q2 at the reported revenues of $249.6 million. The segment’s operating income still fell by a clear -24.6% into $14.7 million. While the revenues still declined due to weak Jack Wolfskin wholesale revenues, I believe that the clear sequential improvement is a very good sign in the quarter, providing a recovery path into better growth.

To summarize, the quarterly performance was mixed. Overall financials came in fine compared to expectations. Topgolf’s operating income grew well, but the performance was still concerning underneath due to deteriorating traffic trends. Golf Equipment revenues and income fell understandably due to seeming industry pressures and tough comparison financials, and the Active Lifestyle saw a great sequential improvement closer to positive growth.

Lowered Guidance Underlines Topgolf Worries

Topgolf Callaway lowered the 2024 financial guidance with the Q2 report, being a more notable part in the report than the financials in my opinion. The revenue range was lowered into $4200-4260 million from $4435-4475 million previously, primarily due to weaker expected Topgolf same-venue sales – the same-venue sales guidance went down into “down very high single digits to low double digits” from “slightly positive to down low single digits” previously, being an incredibly dramatic shift – the company doesn’t expect a recovery in 2024 that it did after Q1.

The profitability is also ultimately expected to take a hit from the lower same-venue sales, as the adjusted EPS range was lowered to $0.11-0.21 from $0.31-0.39 previously.

The new guidance reiterates the fact that Topgolf is underperforming structurally. The company discussed Topgolf’s same-venue sales in detail in the Q2 earnings call, reflecting the performance to inflation, weak consumer discretionary spending, but also clearly communicating that the result is highly disappointing.

In July, same-venue sales were down approximately -11%, sharpening the decline. I believe that the guidance shift is a very worrying sign, especially if Topgolf Callaway doesn’t start showing improvements in tandem with better consumer spending and Bowlero. Continued declines could deteriorate the Topgolf growth story, and the Q2 result and 2024 outlook show beginning signs of such.

Strategic Alternative Process Was Initiated for Topgolf

With the disappointing Topgolf performance, the company is starting a strategic alternative process for the Topgolf business, looking at both organic and inorganic alternatives. Topgolf Callaway’s CEO, Chip Brewer, communicated the following in the Q2 press release:

“…we have been disappointed in our stock performance for some time, as well as the more recent same venue sales performance. As a result, we are in the process of conducting a full strategic review of Topgolf. This review includes the assessment of organic strategies to return Topgolf to profitable same venue sales growth, as well as inorganic alternatives, including a potential spin of Topgolf. Our strategic review of Topgolf is being conducted with the help of outside advisors and is focused on maximizing long-term shareholder value. We are active in this work at present and expect to complete our strategic review of Topgolf expeditiously. We will report back on this when the work is complete.”

I believe that the strategic review’s initiation underlines Topgolf’s expected future weakness in addition to the Q2 call’s remarks, guidance change, and weak Q2, piling onto Topgolf worries’ potentially structural nature. A potential spin-off could be the best alternative for the business, creating a better focus on improving Topgolf. It seems that while the company is diligently going through many alternative outcomes from the strategic process, a spin-off is likely in mind.

Updated Valuation: Still Unattractive

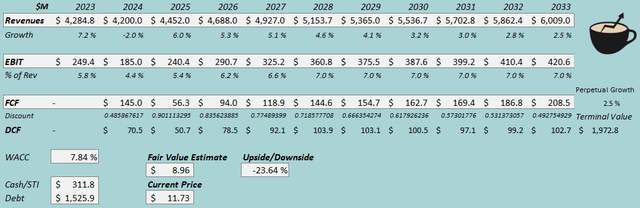

I updated my discounted cash flow [DCF] model. I now estimate -2% revenue growth in 2024 at the lower bound of the new guidance range, and a total CAGR of 3.4% from 2023 to 2033 as compared to a 4.4% CAGR estimate previously – the same-venue sales performance notably lowers my growth expectations for the company.

The weak same-venue sales are likely having an adverse impact on margins as well, countering some of the good expected Topgolf operating leverage. As such, I now estimate the EBIT margin to only expand to 7.0% compared to an 8.0% estimate previously.

With working capital decreases, the 2024 cash flows look to be improved from my previous estimates. Afterwards, I have adjusted cash flow expectations with slightly higher lease interest expenses factored into cash flows, but slightly lower Topgolf capital expenditures behind the lower estimated growth.

For more thorough explanations, I refer to my initial article.

DCF Model (Author’s Calculation)

The estimates put Topgolf Callaway’s updated fair value estimates at $8.96, 24% below the stock price at the time of writing – I believe that amid the incredibly weak Topgolf performance, the stock still has room to go down after an already weak price action. The strategic alternative process could streamline shareholder value, but doesn’t likely create a significant upside from my estimates.

The fair value estimate is down from $10.60 previously.

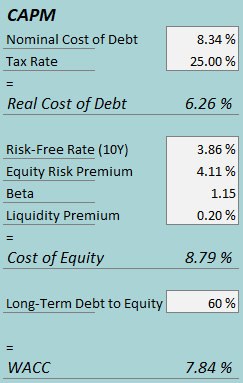

CAPM

A weighted average cost of capital of 7.84% is used in the DCF model, down from 8.85% previously. The used WACC is derived from a capital asset pricing model:

CAPM (Author’s Calculation)

I now use Topgolf Callaway’s 2023 Term Loan B’s 8.34% interest rate as the long-term estimate, being the company’s notable debt and due in only 2030. I again estimate a 60% long-term debt-to-equity ratio, as the company still has an overleveraged balance sheet.

To estimate the cost of equity, I use the 10-year bond yield of 3.86% as the risk-free rate. The equity risk premium of 4.11% is Professor Aswath Damodaran’s estimate for the US, updated in July. I have kept the beta estimate at 1.15. With a liquidity premium of 0.2%, the cost of equity stands at 8.79% and the WACC at 7.84%.

Takeaway

After Topgolf Callaway reported weak Topgolf sales, expecting the weakness to persist throughout 2024, the company’s financial outlook has worsened considerably. Weak consumer spending is related as a primary reason, but I believe that the relation doesn’t completely hold water, and the traffic trends show worrying signs of structural Topgolf demand. Amid the company’s initiated strategic alternative process for the Topgolf business to streamline shareholder value, I remain bearish on the stock with my new, lowered financial estimates. As such, I remain with a Sell rating for Topgolf Callaway.

Read the full article here

")

")

")

")