")

")

Stock: Bulls On Parade")

Harrow, Inc. (NASDAQ:HROW) is a name that has caught our eye, putting in new recent highs. This stock has some pretty significant short interest, and the shorts are being forced to cover. The covering rally can continue, but there is operational strength with this company.

It is tough to chase a stock when it has made such a move. However, bulls are in charge, and we suspect the stock can make a run to $50 this year, especially if the next two quarters go as swimmingly as the just-reported Q2 earnings went. We will discuss those earnings in this column.

For those of our many followers and members who may not be familiar with this name, Harrow is an eye care pharmaceutical company. Pharmaceutical stocks of all stages come with special risks and catalysts, namely via pipeline developments and data readouts, but sales also speak volumes for those with active products. Harrow has a position in discovering and developing innovative ophthalmic pharmaceutical products. It targets the North American market. Harrow has a comprehensive portfolio of prescription and non‑prescription pharmaceutical products that are used by millions of patients. Harrows’ products are used in surgical procedures, such as cataract and refractive surgeries, as well as large and growing chronic eye care markets, such as dry eye disease, glaucoma, allergies, and infections. Harrow and its affiliate ImprimisRx serve over 10,000 doctors, hospitals, and ambulatory service centers through an integrated national sales center.

Here is the deal. The company reported impressive Q2 growth. Long-time holders of this stock probably know that the recent success was many quarters in the making. Harrow is seeing strong performance across all of its operating segments. IHEEZO and VEVYE are firing on all cylinders. ImprimisRx, the affiliate, saw record revenues in Q2. The Anterior Segment business continues to perform. It is worth noting that Anterior Segment revenue in the second quarter of 2024 grew by over 40% from the first quarter of 2024. There will be quarter-to-quarter revenue variability, but the overall revenue trend for this part of the business is improving.

Further, the company continues to advance the relaunch of TRIESENCE this year. With TRIESENCE the company reported that initial analytical test results for the second process performance qualification batch had desirable results. The third batch is imminent. So TRIESENCE is another positive catalyst moving forward. We expect the company will see further revenue and profitability expansion in the coming quarters.

The quarter has many positives. IHEEZO quarterly unit volumes nearly doubled, up about 98% from last quarter. The company indicates they have now signed 24 supply agreements with strategic retina practice accounts this year, including 10 in Q2 and another 7 since June 30th. The company also had a recent agreement with the largest and highest volume retina practice group in the United States. VEYVE saw a massive increase in total prescriptions in Q2, increasing 212% from the sequential first quarter of this year. VEYVE is only in select geographies and territories, and there is significant room for expansion.

As we look ahead, the CEO, Mark Baum stated on the call:

Based on our overall operational momentum, we expect revenue in the back half of 2024 to outpace revenue in the first half of this year, and that’s especially true with TRIESENCE relaunched later this year. I remain confident that 2024 revenue will be greater than $180 million, excluding any TRIESENCE’s contribution. And at this point, I believe the question is just how much greater than $180 million we will print.

This is an incredibly bullish statement. So H2 will be better than H1, but the volume of sales will be so strong that the projections are open-ended, as evidenced by it being unclear how much more than $180 million in revenue they will generate. Very bullish.

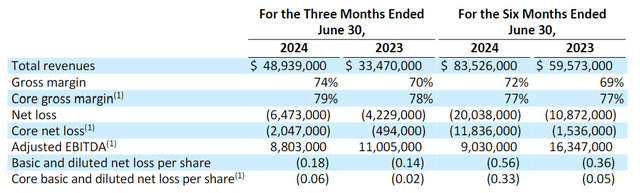

So, in Q2, revenues were $48.9 million, beating estimates by $7 million, and through H1 revenues have hit $83.5 million. There is a real inflection higher in sales this year. This quarter’s revenues were up 46% from a year ago. Moreover, the company is enjoying margin expansion. Gross margins were 74%, up 400 basis points from last year’s Q2. Adjusted gross margin was up to 79% from 78% last year.

HROW Q2 Shareholder Letter

Now, bears hone in on the fact that the company is still losing money, but the company is clearly moving toward being earnings positive as volumes ramp up and margins expand. Now, the company did see a higher net loss this year versus last year, as expenses surged with sales, despite better gross margin, however, the adjusted EPS, which was a loss of $0.06, this was $0.05 better than expected. As TRIESENCE comes to market and revenues balloon, we see 2025 as a year of positive earnings. Thus, we expect 2024 to be the last year of losses for the company.

Read the full article here

")

")

")