")

")

")

MPW stock: 12% dividend yield in jeopardy

I last analyzed Medical Properties (NYSE:MPW) about three months ago. As you can see from the screenshot below, the article was entitled “Medical Properties Trust: Dividend Trap Turned Into Value Trap” was published by Seeking Alpha on May 16, 2024. As the title suggests, I considered the stock a value trap with the Steward bankruptcy and argued for a sell rating. Quote:

The current short interest on Medical Properties Trust stock sits around 38%, but you should not be on a short squeeze. Turnarounds do happen from time to time, but not nearly as often as many of us think. Our optimism for a successful turnaround is largely the result of survivor bias. In any case, for turnarounds to work, they always take time – which I don’t think MPW has much, judging by its liquidity and balance sheet.

Seeking Alpha

Since that writing, the stock price has fallen by about 9% (against a 4% gain of the SP500 index). Despite the price decline, I think the stock’s return prospect has actually further worsened, judging by the developments in its financials since then. Thus, the goal of this article is to detail these new developments, reiterate my sell rating, and also describe a sell strategy via the use of call options to take advantage of its price volatility.

Many investors probably are drawn to the stock by its high dividend yield (currently around 12.8% at the price of writing). However, I am very concerned about the sustainability of the yield given the worsening financials since my last writing. To wit, the chart below compares the operating cash flow and dividend payments for MPW stock in recent quarters, showing a very concerning trend. Cash from operations has declined substantially from $74.3 million in the previous quarter to the current level of $35.3 million. On the other hand, the common and preferred stock dividends payments, despite the large recent cut, are still hovering around $90 million. With such a significant gap, I am very concerned about MPW’s ability to sustain dividend payments and see large odds for another sizable cut in the near future.

Its debt situation further compounds the risks, as detailed next.

Seeking Alpha

MPW stock: Debt in focus

The chart below shows the long-term debt and interest expenses for MPW stock in recent quarters. As seen, to its credit, the company has been deleveraging its debt. The current long-term debt sits around $9.37B, compared to about $9.73B a year ago. However, the debt reduction is too insignificant and much of its impact has been offset by the rising borrowing rates. As a result, the interest expenses stayed stubbornly elevated. Total interest expense has risen from $94.0 million in 2021 to a peak of $108.7 in the March 2024 quarter. The expenses in the last June quarter were $101.4 million, far exceeding the organic cash generation analyzed above.

Seeking Alpha

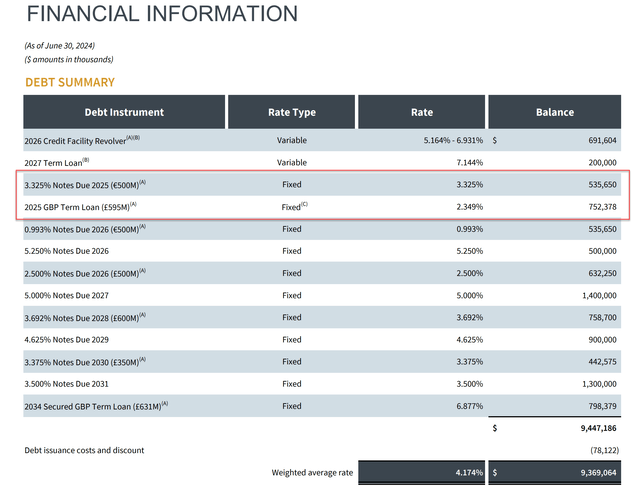

To make things worse, the company has about $1.2 billion worth of debt maturing in 2025 as you can see from the chart below. I am not exactly sure about what the company’s plan is here. But I really do not see a good choice here. Note that these debts happen to enjoy very low borrowing rates. The borrowing rates are in the range of 2.3% to 3.3%, far below both its average borrowing rates of 4.2% and the prevailing debt yield at its credit rating. With its current liquidity and cash generation, I don’t think repayment is a viable choice. It could choose to issue new debt. In this case, I expect the new borrowing would come at far higher rates and further exacerbate its cash flow allocation issues.

MPW Q2 Investor Presentation

MPW stock: Consider the use of option

For existing shareholders who really cannot let it go, I suggest you consider the use of covered-call options. Given the stock’s large price volatilities, the use of call options could generate sizable income and partially offset your losses. As you can see from the next chart below, even for call options with 1 1-month duration, you can collect a sizable income. For instance, a near-the-money (NTM at the price of $4.88 of this writing) call option with a $5 strike price and an expiry date of September 13 currently trades at $0.22. The premium is thus about a 5% return based on the current stock price – for a month. It is far more than the cash dividend yield (which is, again, very likely to be cut in my view) when annualized. If the option is not exercised, you could keep selling similar NTM options to collect income – a strategy that many funds adopt. Furthermore, you still get to collect the cash dividends meanwhile unless/until your shares are called (and bear in mind that the shares can be called before the expiration date for American options). If the option is exercised, then your effective sell price will be $5.22 ($5 strike plus the $0.22 premium).

Merrill Edge

MPW stock: Other risks and final thoughts

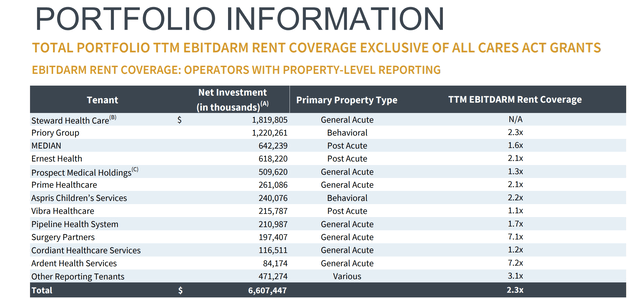

Besides the risks of dividend cuts and debt mentioned above, another downside risk is the potential of other MPW tenants running into financial troubles. The chart below shows the EBITDARM rent coverage of MPW’s current tenants. For readers new to the jargon, EBITDARM stands for earnings before interest, taxes, depreciation, amortization, rent, and management fees. Instead of the more common EBITDA, the REIT industry often quotes the EBITDARM. The idea is that, by excluding rent and management fees, EBITDARM provides a clearer picture of the PROPERTY’s underlying profitability.

As seen, for MPW’s portfolio, the EBITDARM rent coverage ratio is 2.3x on average (with Steward excluded). As a rule of thumb, I consider a coverage ratio of 2x or better to be healthy for the healthcare industry, which is higher than the threshold of ~1.5x I used to evaluate the REIT sector in general. I prefer a higher coverage ratio for healthcare REITs, especially hospital REITs, for a few reasons. First, this specialty sector faces higher uncertainties regarding reimbursement rates, regulations, and policies. Second, they require higher capital intensity. In particular, hospitals require significant capital investments for specialty equipment, technology, and infrastructure, which can impact cash flow and profitability. Finally, hospitals also face higher liability risks compared to other property types, potentially leading to sizable legal settlements.

MPW’s overall ratio of 2.3x is thus quite solid. However, there is quite a bit of variance among its tenants. Even some of the large tenants (such as MEDIAN and Prospect Medical Holdings) are currently operating on rent coverage ratios significantly below 2x as seen.

MPW Q2 Investor Presentation

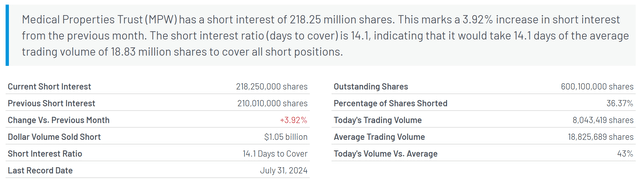

On the upside, a short squeeze represents a key antithesis. As mentioned in my previous article, investors should include the extreme short interest on the stock in their decision. As you can see from the chart below, MPW currently has a short interest of 218.25 million shares, translating into a percentage of shares shorted of over 36%. It would take 14.1 days of the average trading volume to cover all short positions. Thus, if a squeeze happens, it is very likely to be a violent squeeze. Finally, to revisit my options strategy above, the risk calculus of trading options can be vastly different from trading shares. Even with the covered-call strategy I described, your potential loss could be unlimited when you interpret the missed price appreciation (such as in the case of a short squeeze) as a loss.

All told, I think the downside risks far outweigh the upside potential (which is too speculative in my view). The business fundamentals have deteriorated so much since my last writing that I begin to be concerned not only about its dividend sustainability in the near term but also its liquidity and debt serviceability. Thus, I see even higher risks, not lower, despite the price corrections since my last writing.

MarketBeat.com

Read the full article here

")

")

")

")