: Can It Balance E&P And Renewable Investments With Competitive Dividends")

")

Summary

Following my coverage of Casella Waste Systems (NASDAQ:CWST) in May’24, which I recommended a buy rating due to my expectation that EBITDA growth will remain strong into FY25 given the prevailing pricing momentum, cost savings, and volume growth, this post is to provide an update on my thoughts on the business and stock. I continue to give a buy rating to CWST as I am still optimistic about the EBTIDA growth outlook, in which I expect topline to continue growing at high single-digits (driven by both pricing and volume recovery), further margin expansion, and the same level of M&A activity in FY25.

Investment thesis

On 01-08-2024, CWST released its 2Q24 earnings, which saw revenue of $377 million, a 30% annual growth on a reported basis but 6% organically. Collection revenue saw $224 million, with solid waste pricing growth of 5.7% offset by a solid waste decline of 1.8%. Disposal revenue saw 2.3% y/y growth to $65 million, with landfill pricing up 5.2% but offset by a -10.4% y/y volume decline. Total 2Q24 EBITDA saw $92 million at a margin of 24.3%. Overall, CWST remains one of my favorite picks for this industry as pricing growth remains strong, volume growth has potential to accelerate from here, and EBITDA should expand in the coming periods.

On pricing, both the collection and disposal segments continue to see solid pricing growth, at 6.2% and 4.8%, respectively, sustaining the same level of strength seen in 1Q24. This is in line with how the industry price index is trending, and as I have noted previously, using this same trend, CWST should continue to deliver mid-single-digit pricing growth. That said, CWST could drive pricing growth higher than it is today if it decides to turn aggressive on its acquired businesses, which are seeing a more gradual price increase.

The price cost spread for the existing business has been pretty consistent. Over 100 basis points in the base business. In the acquired businesses, we intentionally take a more sort of cautious and gradual approach with price increases. So the effect of our pricing programs is really felt in the base business. 2Q24 earnings results call

On volumes, if we just look at the headline volume performance, it may seem disappointing as it is still negative 1.8%. However, upon deeper assessment, the situation is actually not so bad, and the potential for volume growth to improve seems increasingly likely. In my opinion, the main constraint on growth is the weak macro environment, which I am expecting to get better in the coming quarters. Take specialty waste, construction, and demolition [C&D], for instance. Both verticals continue to see volume declines because of macro-uncertainty as projects get delayed (mostly project-based volumes), and this negative impact was felt by all players. However, note that CWST’s specialty waste pipeline remains strong. This indicates that underlying demand remains strong; it’s just that it is not materializing today. For C&D, the closure of a large competitor landfill remains set to close at the end of the year, so volume will eventually increase. As the macroeconomy gets better, volumes from both of these verticals should recover. I also reiterate that CWST is still shedding contracts (on the residential side, which has low volume). I continue to think this is the right strategy as it improves revenue quality and margin, and as this revenue becomes a smaller mix of total revenue, the impact on volume growth should increasingly become minimal.

Aside from all these macro factors and self-inflicted volume damage, I also highlight that CWST is still not fully utilizing its assets yet. There are multiple projects that should start to ramp up over the next 1 to 1.5 years, such as Mckean, Wllimantic, and RNG.

- Regarding Mckean, CWST’s investment in rail service is nearly complete, and they recently received their first test loads at the site in 2Q24 to test equipment. If all goes well, I expect CWST to ramp up volume here. Note that the incremental contribution from Mckean is not included in the guidance.

- Regarding Willimantic, the recycling facility is on track to open in 2H24, so that should help with 2H24 volume performance and 1H25 given the easy 1H24 comp base.

Combined the above points together, it will not be difficult to see revenue grow at mid- to high-single-digits for the foreseeable future (pricing growth mid-to-high-single-digits + volume improving from negative to historical low-single-digits).

On EBITDA margins, just to note, CWST adj. EBITDA margin for 2Q24 is actually better than what was reported. The business saw $3 million in one-off expenses (which was an 80 bps margin headwind) related to higher leachate costs tied to wet weather and employee separation costs. If we exclude these expenses, EBITDA margin would’ve come in at 25.1% (20 bps improvement vs. 2Q23). Looking ahead, I do expect EBITDA margin to improve accordingly as volumes pick up, pricing stays strong, and the cost structure is lower. The last point is my focus here, as it is amazing that the cost of operations on a same-store basis was down 60bps vs 2Q23. Given that this was not due to overall inflation coming down (still sticky at >5%), I see this 60bps improvement as a structural one from improved productivity.

So, I think inflation has been a little stickier than we had predicted at the beginning of the year and we’re seeing trends generally flattish through the spring that not decreasing what we’re seeing inflation hang north of 5% roughly in our business.

From an operational standpoint, our fleet automation, route conversion, and onboard computer plans are driving higher productivity levels and improving operating cost metrics. 2Q24 earnings results call

Finally, CWST continues its M&A streak that further juices overall growth. On a year-to-date basis, CWST has completed five acquisitions, which are expected to contribute $100 million in annualized revenue (per the 2Q24 transcript). Importantly, nearly all of these acquisitions are in the Mid-Atlantic, where the company acquired GFL’s assets last year, so I am expecting to see a high incremental margin contribution (further supporting a positive EBITDA outlook) as CWST reaps the benefit of route density (management continues to look for acquisitions in this region). The pipeline remains very active, with potential for additional acquisitions in late 2024 and into early 2025. As such, I don’t see M&A growth contributions coming down anytime soon.

Valuation

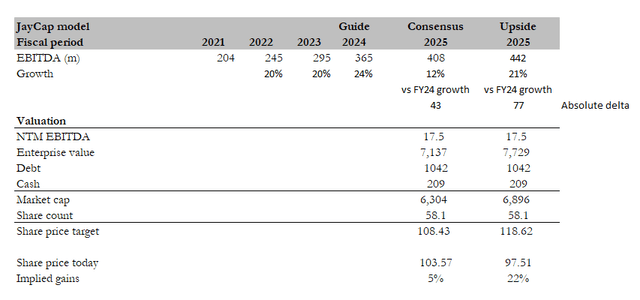

Own calculation

My model mechanics are the same as my previous model (this makes it easier for readers to follow up on my updates). There are only a few updates that I am going to highlight. Firstly, management has revised their FY24 EBTIDA guidance upwards by $10 million at the midpoint, so my FY24 EBITDA estimate now calls for $365 million. There are two scenarios from here for readers to consider. The consensus case is more conservative, which doesn’t seem to imply the same M&A momentum that CWST is seeing today. The 12% EBITDA growth can be easily bridged via high-single-digit revenue growth, margin expansion from fixed cost leverage, improved route density, and productivity savings.

The upside case (same >20% growth for FY25) is what I am betting on, in that CWST continues the same level of M&A activity in FY25. As mentioned above, CWST has acquired $100 million of annualized revenue in just seven months. Extrapolating this level for FY25 implies $200 million of annualized revenue, which can translate to an additional EBITDA contribution of ~$40 million (assuming the same blended EBITDA margin). This incremental $40 million bridges the gap between my upside case and the consensus estimate of $408 million.

More aggressive investors would assume a higher multiple than the 17.5x forward EBITDA that CWST is trading at today, but for my model, I think it is safer (and more conservative) to assume this level of valuation since it is the average over the past five years.

Risk

Prolonged macro uncertainty will cause C&D and specialty waste volumes to remain weak. Failure to integrate acquired targets will cause a delay in margin expansion (from improved route density). In the worst case, CWST will be operating a disparate number of non-integrated assets, which makes its competitive position weaker as resources are not being utilized effectively.

Conclusion

In conclusion, my rating for CWST is a buy rating. Despite near-term volume challenges, strong pricing, margin expansion, and an active M&A strategy underpin my optimism for strong EBITDA growth. Although I flagged M&A as a risk, CWST’s track record so far has been great in integrating these assets, so I am confident that future M&A will follow a similar trend.

Read the full article here

: Can It Balance E&P And Renewable Investments With Competitive Dividends")

")

")