")

Over the next 6 years, data centers are expected to go from consuming 3% of the United States’ power supply to 8%.

This is a massive shift, which should lead to significant change across a number of markets, not least of which the power supply market, which is where our focus is today.

One of the main beneficiaries of this shift is expected to be Vistra (NYSE:VST), the midsize electric utility company. The company’s stock has gone on an incredible run over the last year as a result of this expectation, rallying more than 160% in almost a straight line:

Seeking Alpha

While the performance has been impressive, the question remains: Can VST grow into this new valuation, capturing this amazing opportunity? Or will the company fumble the bag as larger players circle the kill?

Today, our goal is simple: to figure out whether or not VST has what it takes to deliver on its new, impressive (and perhaps inflated) market expectations.

Will the company sink or swim? Let’s dive in and decide.

Vistra’s Financials

If you’re unfamiliar with VST, then you’re not alone. Prior to the company’s massive run over the last year, the utility company was a relatively small, insignificant player in the overall electricity landscape of the USA.

The company’s origins go back to Texas Competitive Electric Holdings, which was a utility company until 2016 when it went bankrupt. Vistra emerged from the ashes in May of 2017 with significantly less debt and a better operating plan.

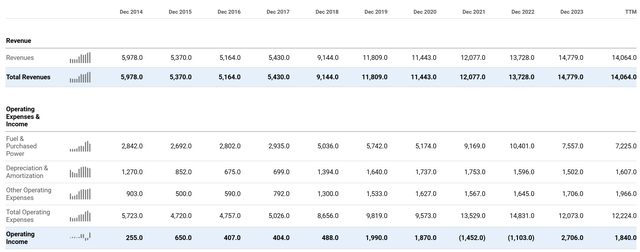

Since then, the company has performed well, generating significant revenue growth and operating profits through a mix of organic growth, acquisitions, and margin improvements:

Seeking Alpha

Much of this comes from lower interest payments on long term debt, along with continued fleet optimization and a strengthened hedging strategy.

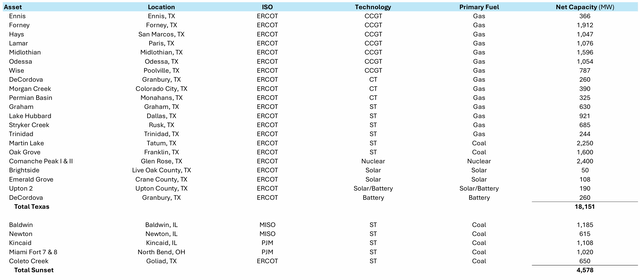

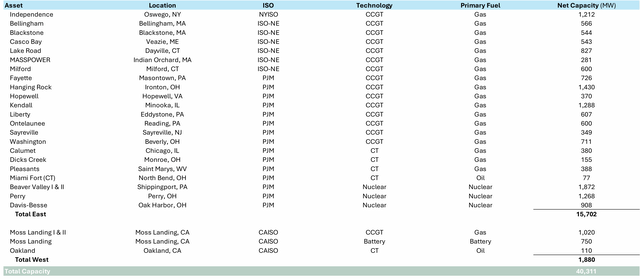

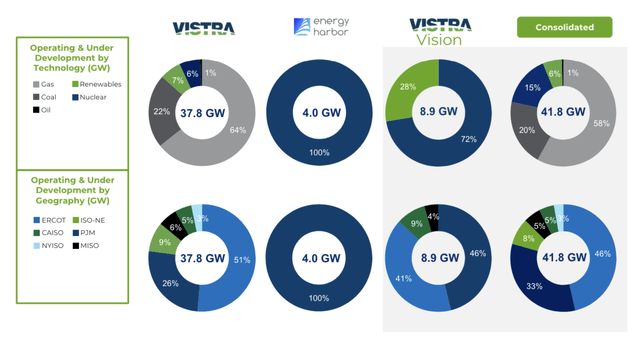

Speaking of the fleet, the company owns a mix of Nuclear, Gas, Oil, Coal, and Renewable generation sources, across the U.S. but primarily within the US’s geographic east and Texas:

Quarterly Presentation

Quarterly Presentation

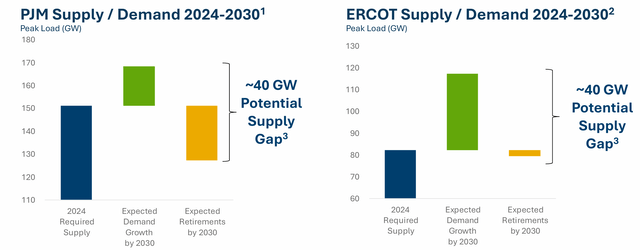

While everything looks somewhat ho-hum so far for the average electric utility, the real bull case, in one slide, is the following graph showing projected power supply gaps emerging in the market over the next few years in key VST markets:

Quarterly Presentation

Gaps of this size will be expensive to plug in terms of Capex, and so there’s every expectation that companies that are able to meet this massively higher demand will reap significant rewards in terms of cash flow.

But why is electricity use projected to expand so much?

Data centers. More specifically? AI.

Much ado has been raised about this recently as more and more news publications have picked up on the fact that AI-powered data centers will suck a lot more power than the grid can currently handle, which could cause disruptions and issues looking ahead.

Not only that, but data center operators, like Google (GOOG) Amazon (AMZN), and Microsoft (MSFT) also have green pledges that will likely cause them to contract with green energy sources, which is a unique wrinkle.

Luckily for Vistra, more than 20% of the company’s power generating capacity is ‘green’, and another nearly ~60% is powered by relatively lower-carbon natural gas, which means that the firm is in a good spot to cash in on this secular surge in power demand:

Vistra IR

In addition, with the company’s recent acquisition of Energy Harbor (and the resulting nuclear facilities) VST is now in a good position to structure ‘behind the meter’ deals where big players buy electricity directly from generation facilities. Many analysts have speculated that this will happen, and we think it’s only a matter of time until deals begin closing on this front.

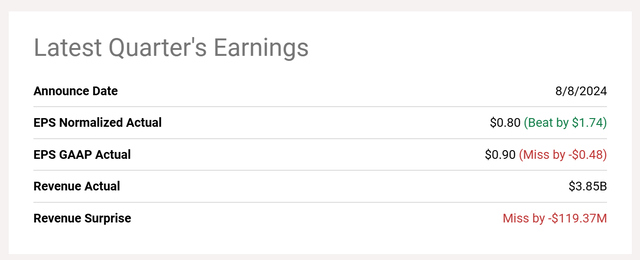

Recent earnings also strengthened our belief in the company looking ahead.

While the numbers for Q2 came in somewhat mixed versus inflated expectations, management remained bullish overall:

Seeking Alpha

On the call, CEO Jim Burke had the following to say:

Turning to guidance. We are reaffirming our guidance range for 2024 ongoing operations adjusted EBITDA of $4.550 billion to $5.050 billion. Based on performance to date and our forecast for the remainder of the year, we are confident in our ability to deliver towards the upper end of this range.

Moving to our long-term outlook…

Given our hedging activity over the past several months and the recent 2025-2026 PJM planning year auction results, we are raising our estimated 2025 ongoing operations adjusted EBITDA mid-point opportunity range by $200 million to $5.200 billion to $5.700 billion.

Said differently, as a result of the tailwinds in the sector, management sees an even better operating picture in the coming ~18 months.

Finally, as was referenced in the call above, a recent power auction in PJM, one of the larger interconnections in the US, and one in which VST has generation capacity, showed a 9x price in power over the last year, which is quite something.

Add it all up, and the bull case for Vistra is an enticing cocktail of surging demand, being at the right place at the right time, and strong financial management over the last ~7 years, all of which should allow for higher profitability into the second half of the decade.

Vistra’s Valuation

As things sit now, the company currently stands on a stable financial platform to deliver on this opportunity. With the bankruptcy in 2016 behind it, VST is now a lean, mean, power generation machine, with strong profitability and ROE to boot.

The income statement can get a bit muddy given all the recent M&A, but once you strip out working capital changes, the recent Energy Harbor deal, and D&A, VST is highly cash generative, with nearly $4 billion in cash from operations over the last twelve months alone.

On a straightforward basis, this puts the company, which is trading at a $27.6 billion market cap, at a roughly 7x cash gen multiple.

However, VST is a highly asset-heavy business, and so using a more traditional FWD P/E puts you a lot closer to 16x, which is a lot higher, but not overly so.

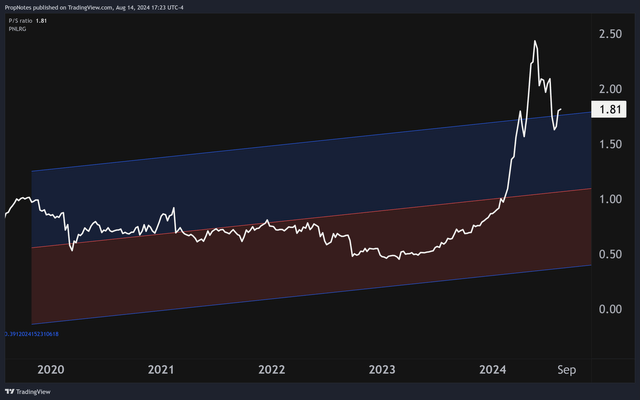

On the top side, the sales multiple recently spiked as the share price exploded, but much of this increase can be explained by the fact that investors are expecting increasing ROE off of the existing asset base, which gives the revenue a higher premium looking forward:

TradingView

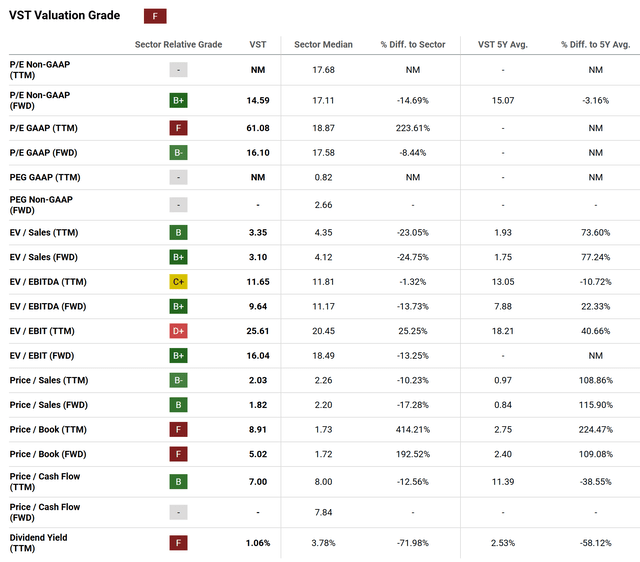

While Seeking Alpha’s quant score puts VST’s grade at an ‘F’, we’re not so sure we agree:

Seeking Alpha

It’s true that a number of these metrics don’t look good, including the ‘all important’ GAAP P/E number, but given the opportunity – especially when you tack on the revised estimates – and shares begin to look less expensive than expected.

For us, if you’re looking at VST on a combined sales & FWD P/E basis, we think there’s a lot of room for the valuation to expand further, as those metrics trade closer to industry averages.

Plus, with the expected organic sales & EBITDA growth coming over the next year or two, it’s easy to see how VST could have ~40% upside in the share price over the next twelve months.

It’s hard to overstate how large the shifts happening in the power market are right now.

Risks

That said, despite our projected upside, investing into VST does carry some risks, which should be mentioned.

First off, the company is highly indebted, which could be an issue with rates where they are right now. The company issued nearly $1.3 billion in debt in the last quarter alone, which isn’t ideal. Obviously, management thinks that the IRR of projects should be higher than the cost of this debt, but at current issuance prices, this may chip into ROE somewhat, which could dent the multiple down the line.

Second, the company operates in an asset heavy market, which comes with a lot of additional operational and execution risk. In short, things can go wrong at power generation facilities, the weather can act up, and swings in power prices can impact results in short order. The company has done a good job of managing these risks so far, but they could rear their ugly head overnight if things go wrong. It’s a moderate tail risk.

Finally, while we think the valuation looks reasonable for what’s on offer, the stock screens poorly on the valuation front as a result of backwards looking multiples, which could mute investor interest. This is despite improving results going forward. This isn’t a material loss risk in our view, but it could be a huge headwind on the upside we envision.

Summary

While there are some risks involved with Vistra at the current juncture, we think that overall, the company’s strong generating capacity, financial position, and AI / Nuclear tailwind are likely to continue propelling shares higher over the interim.

Thus, our ‘Buy’ rating.

Good luck out there!

Read the full article here

: Can It Balance E&P And Renewable Investments With Competitive Dividends")