")

Blade Air Mobility, Inc. (NASDAQ:BLDE) reported solid results in Q2, achieving its first positive adjusted EBITDA quarter as a public company. Medical revenue continues to grow and jet revenue bounced back in the second quarter. Overall growth is sluggish, though, as Blade has been pulling back from activities with questionable economics, creating a growth headwind.

I previously suggested that while Blade’s valuation was low, it was on a collision course with TransMedics Group (TMDX), which could create issues. There are no obvious signs of this yet, but it seems likely that this issue will come to a head over the coming quarters. I continue to think that even modest growth in the Medical segment or a boost from eVTOLs could provide material upside, but Blade needs to do more to limit dilution of existing shareholders.

Market Conditions

Within Blade’s Medical segment, technology and regulatory changes continue to drive solid growth in the demand for organ transportation. Heart, liver, and lung organ transplant volumes increased in the high single digit range in Q2. This appears to be a slight decline from the 9% YoY increase registered in Q1.

Figure 1: Organ Transport Volumes in the US (source: Blade)

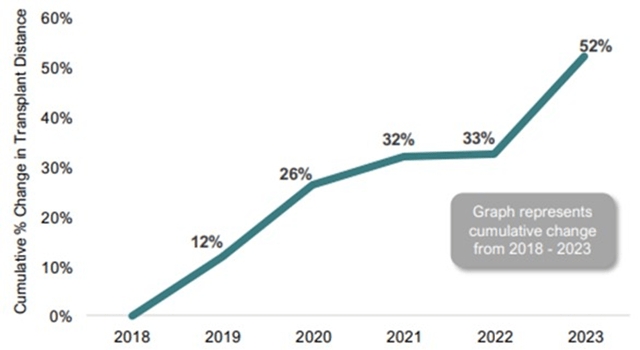

Perfusion technology is allowing organs to be transported further, directly benefiting Blade, both because it results in more air transport and because flights are often longer. While this is a positive, investors probably now need to start thinking about what happens when volume growth and distance travelled begin to stabilize again.

Figure 2: US Heart, Liver and Lung Transplant Distance (source: Blade)

Perfusion devices have primarily benefitted liver transplants so far, meaning there is still a large opportunity if this success can be replicated in other organs (lung and heart). There are clinical trials planned which could enable more lung and heart transplants, and for organs to be transported greater distances in the upcoming years.

Blade’s Medical segment is likely to face increased competition over time, and while I think there will remain an important place in the market for Blade, it may lose out on the most attractive segment of the market. Around 50 transplant centers perform over 70% of the lung, heart, and liver transplants in the US.

TransMedics is pursuing this market aggressively presently, and while it is primarily a perfusion device company, its expansion into logistics is helping it to maximize the value of its technology. TransMedics’ transplant logistics revenue increased 32% sequentially to $19.1 million USD. The company now owns 17 aircraft and doubled its pilot count in Q2. 11 aircraft were active in Q2 compared to 9 in Q1, and the company has a target of 20 by the end of the year.

Ground transportation has also been a growth driver for Blade within its Medical segment. There could still be further upside in this area as well. Blade estimates that the total addressable market, or TAM, of its ground transportation service is approximately $200 million USD. This market is more likely to remain fragmented than air transport, though, as it has lower barriers to entry.

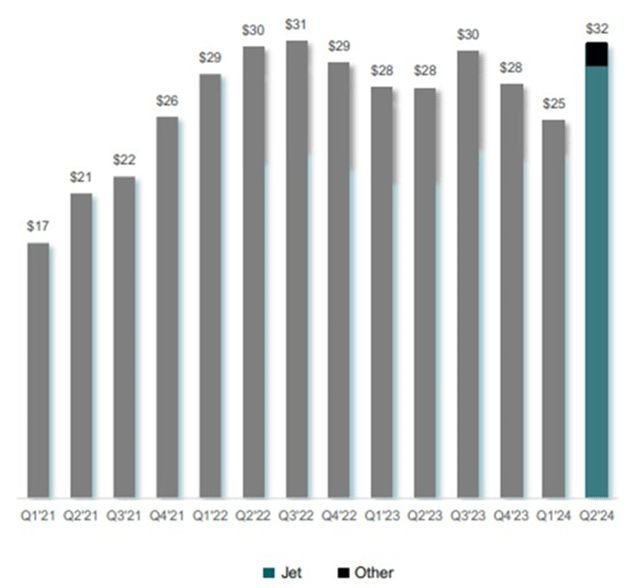

Blade’s Jet business had a strong second quarter and was an important driver of outperformance. This part of the business has been under pressure due to macro weakness and Blade pulling back on unprofitable routes. Whether Q2 represents a change in fortune for this part of the business or a temporary blip remains to be seen. Fundamentally, there is no real reason to believe the demand environment has materially changed, though.

Figure 3: Jet and Other Revenue – TTM (source: Blade)

Blade Business Updates

Blade has exited certain Passenger routes that weren’t economically viable. While this is creating a growth headwind, it should lead to improved margins in time. This includes restructuring its Canadian operations and, ultimately, preparing to exit the Canadian market. Blade has also been streamlining its commercial organization and cost structure in Europe.

Blade continues to expand its short-distance infrastructure and enter into partnerships that provide traffic. For example, Blade is launching a new codeshare with Emirates that provides seamless transportation between Dubai and Monaco. Blade also recently opened two new terminals at Nice Airport and a rooftop helipad at the Ocean Casino Resort in Atlantic City. Blade has a partnership with the resort to offer scheduled service in the summer months.

Blade closed 7 of the 8 previously announced jet aircraft acquisitions during the second quarter and believes that its fleet is generating a return on invested capital of over 30%. Around 10% of Blade’s Medical flights are expected to be performed by these aircraft in 2024.

While the majority of Blade’s flights will continue to be performed by third-party owned and operated aircraft, there is an opportunity for Blade to further expand its fleet. Blade has suggested it could add a low single digit number of aircraft over the next 6–12 months.

Blade also continues to expand its Medical ground logistics business, recently opening two new ground hubs, bringing the total to 8. The company currently has over 30 vehicles in its ground transportation fleet.

eVTOLs

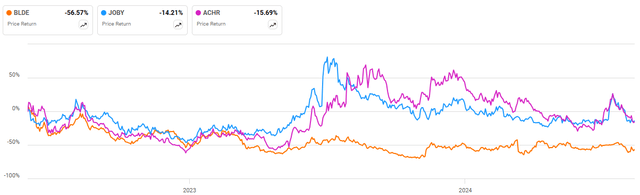

eVTOLs could be a growth driver for Blade in the upcoming years, but it is not clear that this is priced into the stock yet. For example, Blade’s share price hasn’t benefitted from hype around the progression of eVTOLs towards commercialization over the past 12 months.

Companies like Joby (JOBY) and Archer Aviation (ACHR) continue to progress through the certification process and are establishing manufacturing capacity. While these companies intend to operate air taxi services, the initial focus will be on aircraft sales, as this is the fastest path to profitability.

Joby and Archer are both focused on international markets like the Middle East, as this is probably the fastest road to commercialization. Blade believes that deployment there is likely to occur in 2025/2026, with a launch in the US more likely in 2026. It will most likely be 2027 before volumes begin to build, though.

Blade believes that the market will initially be constrained by access to landing zones, particularly in the larger markets which already have considerable traffic. This is likely to provide the company with an important advantage early on.

Figure 4: Blade Share Price Performance (source: Seeking Alpha)

Financial Analysis

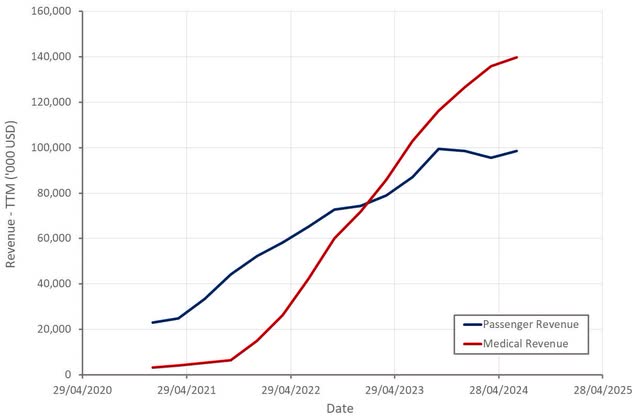

Blade generated $67.9 million USD revenue in the second quarter, an increase of 11.4% YoY. Excluding the impact from the discontinuation of BladeOne and a temporary jump in Medical revenue in Q2 2023, revenue growth was 17.5%.

Medical revenue was $38.3 million USD, up 11.5% YoY, driven by growth in hours flown and revenue per hour. While Medical growth remains solid, it is moderating rapidly, particularly outside of ground transportation. Medical ground revenue increased more than 50% YoY during the quarter and represented 12% of Medical revenue. Non-ground medical growth must therefore have only been around 8%.

Short-Distance revenue was $20.9 million USD in Q2, an increase of 9% YoY. This increase was attributed to Blade’s New York Airport transfer product and growth in Europe. Jet and Other revenue was up 17.4% YoY to $8.7 million USD.

Q3 is reportedly off to a strong start, although Blade hasn’t raised its full-year guidance. Blade expects $240-250 million USD revenue in 2024, an increase of roughly 9% YoY at the midpoint. Double-digit revenue growth is expected in 2025.

Medical revenue is expected to be fairly flat sequentially in Q3 before returning to low single digit sequential growth in the fourth quarter. Short-Distance revenue growth is expected to be in the single digits in the second half of the year, excluding the impact created by exiting Canada. Canada has been contributing around 10-15% of Blade’s Short-Distance revenue. Jet and Other revenue is expected to be around $5 million USD per quarter in the back half of the year.

Figure 5: Blade Revenue (source: Created by author using data from Blade)

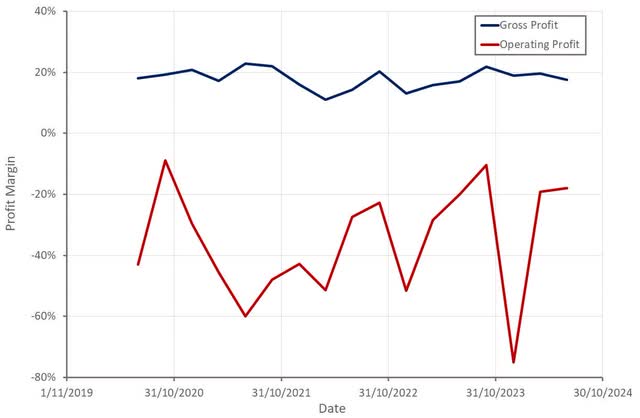

Blade’s Medical flight margin was 23.6% in Q2 and continues to edge higher. Blade has attributed margin expansion to pricing, the growth of its Ground Logistics business and its acquisition of aircraft. Blade has suggested that using its aircraft could result in a 10-20% improvement in flight margins, although this would only be on a fraction of Medical revenue.

The improvement in Passenger profit margin was attributed to pricing and efficiencies in Blade’s New York Airport transfer product, growth in Europe and improvements in Jet Charter.

Blade’s decision to exit the Canadian market resulted in a $5.8 million USD write-off of intangible assets, though. Excluding the impact of this, Blade’s operating profit margin would have been around -9% in Q2.

While Blade is progressing towards GAAP profitability, this is a slow process given the company’s current growth rate. Blade probably still needs to grow its top line exceeding 50% to be consistently profitable, which will take several years.

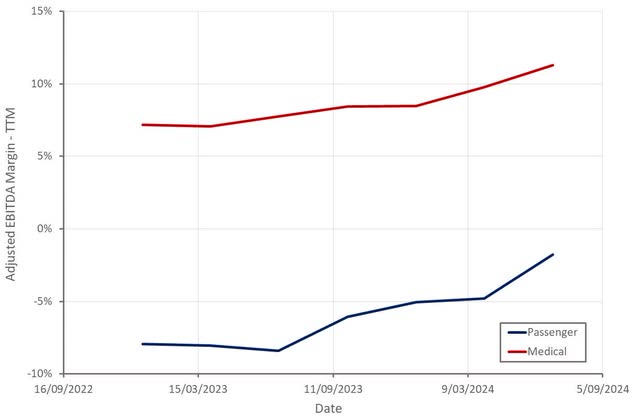

Figure 6: Blade Profit Margins (source: Created by author using data from Blade) Figure 7: Blade Adjusted EBITDA Margins by Segment (source: Created by author using data from Blade)

Excluding the accounting treatment of aircraft acquisitions, cash consumed by operating activities would have been less than $1 million USD. CapEx (inclusive of software development costs) was $16.9 million USD in Q2, driven by $14.6 million USD of payments for aircraft. Once Blade’s build out of its Medical infrastructure is complete (aircraft and ground transportation) the company should be fairly neutral from a cash flow perspective.

Conclusion

While Blade’s business is still expanding, growth is being hampered by the company’s decision to eliminate uneconomic activities in its pursuit of profitability. While this headwind will fade over the next 12–18 months, Medical growth is moderating.

This is important as Blade still has a profitability problem that will likely only be resolved with greater scale. While Blade’s adjusted EBITDA was positive in the second quarter, and cash consumed by operating activities was minimal, its GAAP operating losses are still sizable. The difference is largely due to stock-based compensation, which was around 8% of revenue in Q2. As a result of this, and Blade’s low valuation, dilution is an issue at the moment.

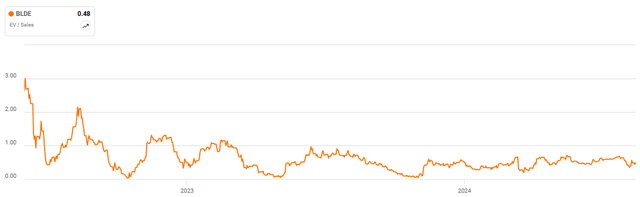

While dilution is a concern, Blade’s EV/S multiple is only around 0.5, meaning there is little priced into the stock in the way of growth or profitability. The company has around $140 million USD of cash and short-term investments and no debt, although there is over $20 million USD of operating leases.

Blade probably needs to reduce its CapEx, return its Passenger segment to consistent growth, demonstrate that Medical growth is sustainable and continue to move its margins higher before the stock rerates higher.

Figure 8: Blade EV/S Multiple (source: Seeking Alpha)

Read the full article here

: Can It Balance E&P And Renewable Investments With Competitive Dividends")