")

")

")

")

")

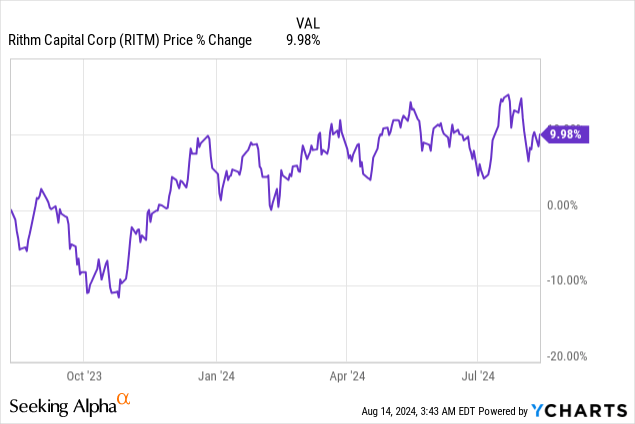

Rithm Capital (NYSE:RITM) represents a promising high-yielding investment opportunity in the mortgage REIT business as the company supports its earnings available for distribution and is growing its business in new areas. Considering that the REIT delivered 1.88X distribution coverage in the second-quarter and that Rithm Capital’s shares are undeservedly trading at an 11% discount to book value, I believe the risk profile for Rithm Capital is skewed to the upside. I am also upgrading my rating on Rithm Capital to strong buy after Q2 earnings, as I see a pathway for the mortgage REIT to grow its revenues in the relatively new asset management business.

Previous rating

A broadening investment scope and a core investment focus on mortgage servicing rights were two reasons why I rated mortgage REIT Rithm Capital as a buy in June: A Deep-Value Investment With A 9% Yield. The REIT repositioned its portfolio in recent quarters and gradually diversified into other non-mortgage investments, which creates a lever for growth. The dividend is also very well-supported by earnings available for distribution.

Diversified portfolio, potentially growing asset management focus

Rithm Capital owns a diversified portfolio of mostly mortgage-related investments, including mortgage servicing rights/MSRs. These rights represent an opportunity for Rithm Capital’s subsidiaries to service mortgage pools and allow the REIT to capture recurring fee income.

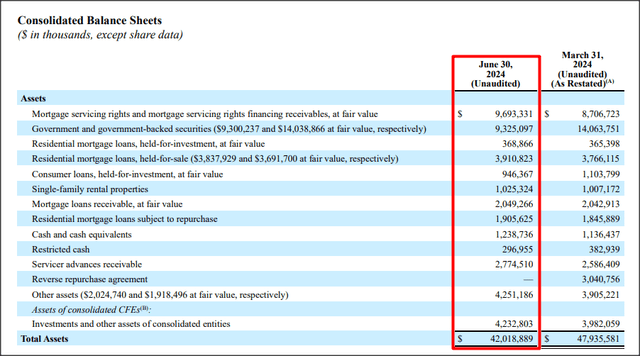

As the Federal Reserve increases the federal fund rate, mortgage servicing rights become more valuable to the holder as the net present value of servicing fees increases. Mortgage servicing rights were the largest investment on Rithm Capital’s balance sheet at the end of the June quarter, with a total fair value of $9.7B, and they have been instrumental in the company’s evolution as a mortgage investment company.

Rithm Capital

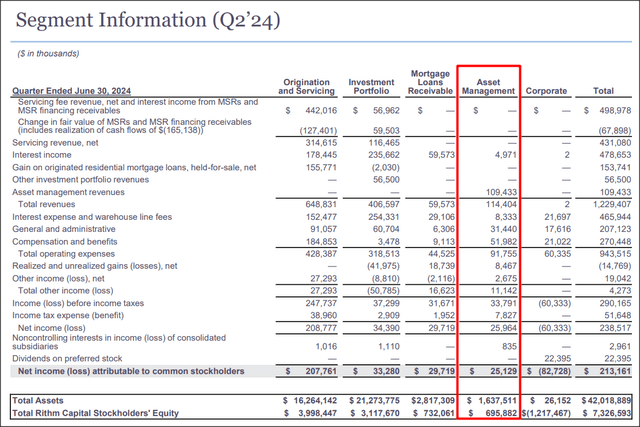

Rithm Capital generates the majority of its income from origination and servicing-related activities, but one segment is coming up rapidly, which is the asset management franchise. Rithm Capital bought out asset management firm Sculptor Capital last year, after presenting sweetened deal terms. This acquisition marked the REIT’s entry into the asset management realm and Rithm Capital is seeing some positive momentum here: segment revenues totaled $114.4M (+51% Q/Q) and represented about 9% of consolidated revenue in Q2’24. The asset management division was also widely profitable, contributing a $25.1M profit to Rithm Capital’s bottom line in the second-quarter. In Q1’24, the segment lost $27.4M, so the turnaround here so shortly after last year’s acquisition is positive and suggests that the REIT has a significant earnings growth catalyst here.

Rithm Capital

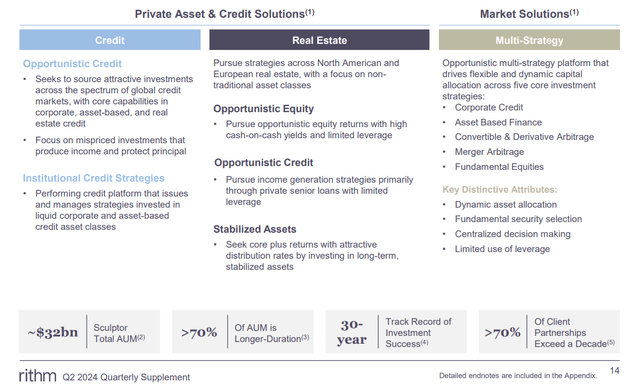

A key lever for earnings growth here relates to Sculptor expanding its platform reach and grow its assets under management, especially the portion of long duration funds. The asset management platform is focused chiefly on credit and real estate opportunities and managed $32B as of the end of the June quarter (more than 70% of those assets had long durations, meaning initial commitment periods of 3 years or longer). Asset under management growth as well as new investment funds could be driving catalysts for Sculptor to make even higher revenue contributions to Rithm Capital going forward.

Rithm Capital

Well-supported 9% dividend yield

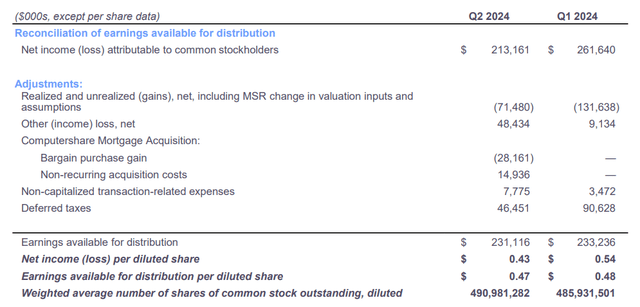

Rithm Capital supported its dividend, with earnings available for distribution (EAD) in the second-quarter. The distribution coverage ratio was 1.88X based off of $0.47 per-share in earnings available for distribution, compared to 1.92X in the previous quarter. Considering the increasingly diversified nature of Rithm Capital’s portfolio and income composition, I believe the dividend is very well-protected. Additionally, investors get to take advantage of a discount to book value that I don’t believe is deserved.

Rithm Capital

Rithm Capital’s valuation

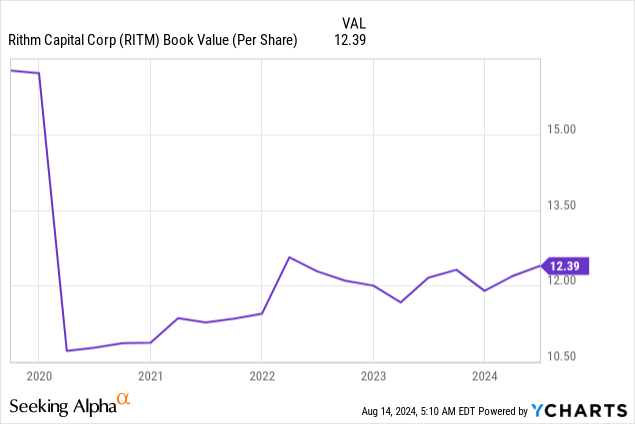

The mortgage REIT was forced to sell assets during the COVID crash in 2020 in order to boost its liquidity profile, which impaired Rithm Capital’s book value, but the REIT has since grown its book value quite consistently.

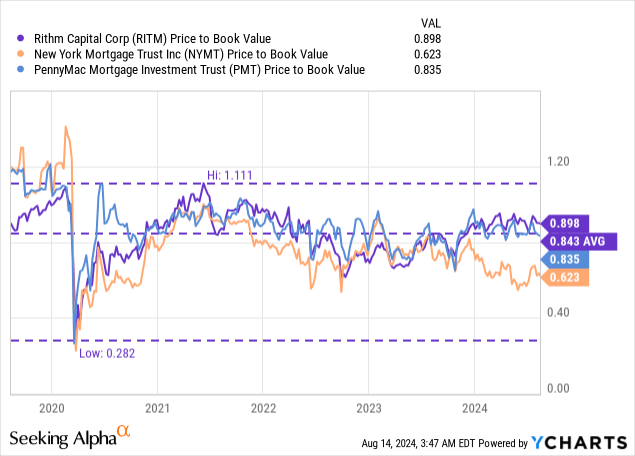

Currently, Rithm Capital is trading at a 10% discount to book value, which I don’t believe is warranted given the general positive trend in book value in the last three years. Further, Rithm Capital’s book value gained 1.6% Q/Q to $12.39 per-share in the second-quarter. Mortgage investment firms like PennyMac Mortgage Investment (PMT) and New York Mortgage Trust (NYMT) trade for even lower book value multipliers, but Rithm Capital has a growing, more diversified portfolio and significant excess dividend coverage. This should allow the REIT to revalue to a P/B ratio of ~1.0X in the longer term, in my opinion. A 1.0X P/B ratio implies a fair value of $12.39 per-share and 11% revaluation potential. Given that the dividend is so well-supported by earnings available for distribution, I believe the 9% yield is why income investors may want to consider an investment in Rithm Capital.

Risks with Rithm Capital

The biggest potential headwind for Rithm Capital is that a considerable portion of its investment capital is invested in mortgage servicing rights, which are rate-sensitive and which may decrease in value in a falling-rate environment. The REIT will also need to prove to investors that asset management-related revenues and income are durable and not subject to significant volatility on a Q/Q basis. Volatile asset management revenue/income may undermine the quality of Rithm Capital’s distribution coverage as well.

Final thoughts

Rithm Capital’s 9% yield is worth buying, in my opinion, chiefly because the mortgage REIT is expanding its investments and moving into ancillary services such as third-party asset management/investment funds. While Rithm Capital has a core focus on mortgage loan originations and servicing, I believe that the REIT also has a lever with the Sculptor platform to grow its assets under management and to diversify its investments away from its MSR-heavy orientation. Importantly, Rithm Capital solidly supports its dividend with earnings available for distribution. The fact that the REIT’s shares are also trading at a 10% discount to book value is a major advantage that I believe only makes Rithm Capital more attractive as an income buy.

Read the full article here

")

")

")

")