")

Key takeaways

- The fund underperformed its benchmark this quarter

- Class A shares at net asset value (NAV) declined during the quarter while the MSCI ACWI ex-US Index’s posted a gain.

- Corporate debt cost likely to rise

- As corporate debt borrowed at cheap interest rates matures over the next few years, companies will have to roll over that debt at more expensive levels. We are comforted that companies in the fund finance their growth from operating cash flow and do not rely on debt.

- We focus on the return on the fund’s invested capital

- We continue to judge companies based on their capital return track record and our opinion of their future potential.

Manager perspective and outlook

Equity markets opened the second quarter with a correction, giving back much of the gain they had made in the previous quarter. However, after bottoming in mid-April, the US and emerging markets regained all of the lost ground and advanced further while developed non- US equities lagged.

As in previous quarters, attention centered on the US Federal Reserve (Fed) and the outlook for US interest rate policy. Fed guidance signaled only one rate cut this year, and not before September “at the earliest.” To the surprise of many, equity markets rose following the announcement. In our opinion, this is evidence that valuations have largely been adjusted for the reality of higher capital costs. The variable effect of those costs on corporate earnings and returns is what we believe will increasingly matter.

We continue to judge companies based on their capital return track record and our opinion of their future potential. We invest in companies we believe are on the growth side of secular trends, are able to monetize those trends profitably and consistently for many years, and are able to fund their growth from their own cash flow rather than needing debt funding.

Portfolio positioning

We initiated three new positions during the quarter.

MonotaRO (OTCPK:MONOY) distributes machine tools, engine parts and factory consumables in Japan. It operates in a fragmented market, with fragmented sets of customers and suppliers, selling small average order value products to customers wanting near instantaneous availability. Monotaro’s one-stop-shop offers the market’s largest product catalogue and 24-hour delivery. In our opinion, the pricing power conferred on Monotaro by its market position is likely to continue.

BAE (OTCPK:BAESF) is a UK-based defense contractor supplying predominantly NATO clients. In response to increasing security threats, Allied defense spending has been rising and is likely to continue rising for some time. In our opinion, BAE is well-placed to benefit from this trend, given its diversified portfolio of equipment and services.

AstraZeneca (AZN) is a UK-based pharmaceutical firm. We like its drug portfolio, research and development capabilities, and oncology platform.

We exited four positions during the quarter.

Barry Callebaut (OTCPK:BYCBF) manufactures cocoa and chocolate products and is based – of course! – in Switzerland. Since we invested over 10 years ago, it has been one of the fund’s “Steady Eddie” performers. However, we believe future growth would need to come from a significantly larger base than when we first invested. We saw more attractive growth opportunities elsewhere.

Campari (OTCPK:DVDCF), an Italian beverage company known for its namesake liqueur, produces and markets more than 50 spirits, wine and soft drink brands globally. We bought the stock when the price plummeted during the COVID decline in 2020, after which the company had significant sales growth. Sales have recently slowed, and we saw better investment opportunities elsewhere.

HelloFresh (OTCPK:HLFFF), born in Germany, is the largest meal kit provider in the US and several other markets. Though we believe it is the one meal kit company with the scale to achieve attractive profitability, management has been taking longer to execute its growth plans than we expected when valuing the company. Therefore, we exited the position.

Legal & General (OTCPK:LGGNY), a UK-based insurer, provides pension administration and management services to corporations. We believe an expansion in the UK Regulator’s purview to include involvement in investing decisions is potentially negative for future returns, so we exited the position.

Top issuers (% of total net assets)

|

Fund |

Index |

|

|

Novo Nordisk A/S (NVO) |

6.06 |

1.81 |

|

ASML Holding NV (ASML) |

4.02 |

1.59 |

|

Reliance Industries Ltd |

3.79 |

0.44 |

|

Dollarama Inc (OTCPK:DLMAF) |

3.38 |

0.10 |

|

London Stock Exchange Group PLC (OTCPK:LDNXF) |

3.01 |

0.21 |

|

Epiroc AB (OTCPK:EPOKY) |

2.85 |

0.08 |

|

Compass Group PLC (OTCPK:CMPGF) |

2.69 |

0.18 |

|

Next PLC (OTCPK:NXGPF) |

2.68 |

0.05 |

|

Atlas Copco AB (OTCPK:ATLKY) |

2.63 |

0.29 |

|

Hermes International SCA (OTCPK:HESAY) |

2.58 |

0.28 |

|

As of 06/30/24. Holdings are subject to change and are not buy/sell recommendations. |

||

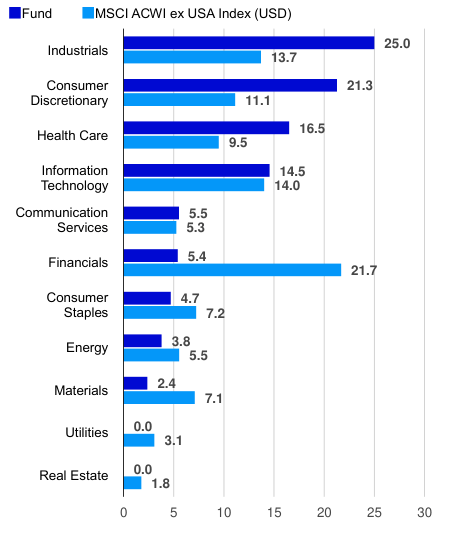

Sector breakdown (% of total net assets)

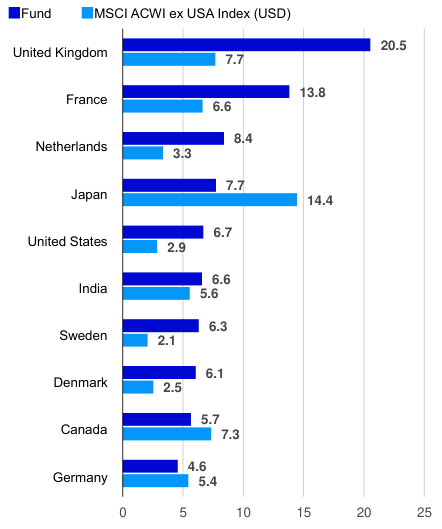

Top countries (% of total net assets)

Performance highlights

The fund outperformed most in the industrials sector due to stock selection, and in energy and real estate due to its usual underweights in those sectors.

The fund underperformed most in the information technology sector due to stock selection, in the consumer discretionary sector due to the overweight position, and in financials due to both stock selection and the usual underweight position.

Contributors to performance

Novo Nordisk in Denmark is the world’s leading maker of care products and insulin for diabetes. Novo has also introduced weight loss drug Wegovy. Clinical trial results for Wegovy’s reduction of coronary disease risk have exceeded expectations.

Dollarama, a Canada-based discount retailer, is part of our “Reorganization of

Retail” theme. We believe the shift to online buying benefits retailers at the very high and low ends of the pricing spectrum.

Hitachi (OTCPK:HTHIY) in Japan has been restructuring itself to provide a higher return on capital. Those efforts have been bearing fruit.

ASM, a Dutch company, makes equipment used in semiconductor production. ASM’s leading product is atomic layer deposition equipment, which delivers 50% of the company’s revenue on a 50% world market share. We believe ASM is well placed to benefit as demand for layered semiconductors rises.

Taiwan Semiconductor Manufacturing Co. (TSM) is a leading semiconductor foundry, particularly in chips that are seven nanometers and smaller – a nanometer is about the size of an atom. During the quarter, TSMC announced plans to expand capacity.

Detractors from performance

EPAM (EPAM) offers businesses a wide range of IT services. During the quarter, EPAM lowered its guidance and the share price reacted unfavorably. We think EPAM is likely to benefit from the rising demand we anticipate for IT consulting as companies strive to take advantage of AI.

Sartorius Stedim (OTCPK:SDMHF), a French company, provides specialized equipment and supplies for biologic drug production and research. Sales have slowed after a period of above- trend growth; in our opinion, this is due to inventory destocking.

LVMH (OTCPK:LVMHF), a French luxury brand owner and manager, is one of the best in the business, in our opinion. Luxury stocks have been volatile after rising repeatedly to new highs over the past few years. This quarter, concerns about a potential slowdown in spending caused investors to take profits.

James Hardie (JHX), is an Australia-based global manufacturer of Hardie Plank, a fiber cement siding, and a stucco substitute. Earnings announced during the quarter fell short of management’s guidance. Longer term, we view James Hardie favorably given the housing shortage in most developed markets.

Airbus (OTCPK:EADSF) has benefited from steadily rising demand for air travel and its strong market position. During the quarter, Airbus announced it will lower its plane delivery target for this year due to supplier issues.

Top contributors (%)

|

Issuer |

Return |

Contrib. to return |

|

Novo Nordisk A/S |

13.26 |

0.72 |

|

Dollarama Inc. |

19.81 |

0.56 |

|

Hitachi Ltd. |

22.56 |

0.34 |

|

ASM International N.V. |

25.69 |

0.34 |

|

Taiwan Semiconductor Manufacturing Company Limited |

22.18 |

0.30 |

Top detractors (%)

|

Issuer |

Return |

Contrib. to return |

|

EPAM Systems, Inc. |

-31.88 |

-0.58 |

|

Sartorius Stedim Biotech S.A. |

-41.91 |

-0.56 |

|

LVMH Moet Hennessy Louis Vuitton SE |

-13.87 |

-0.46 |

|

James Hardie Industries plc |

-21.41 |

-0.41 |

|

Airbus SE |

-24.14 |

-0.37 |

Standardized performance (%) as of June 30, 2024

|

Quarter |

YTD |

1 Year |

3 Years |

5 Years |

10 Years |

Since inception |

||

|

Class A shares (MUTF:OIGAX) inception: 03/25/96 |

NAV |

-1.73 |

2.70 |

7.40 |

-2.30 |

5.79 |

3.83 |

7.26 |

|

Max. Load 5.5% |

-7.13 |

-2.95 |

1.48 |

-4.13 |

4.60 |

3.24 |

7.05 |

|

|

Class R6 shares (MUTF:OIGIX) inception: 03/29/12 |

NAV |

-1.64 |

2.89 |

7.81 |

-1.92 |

6.21 |

4.26 |

6.34 |

|

Class Y shares (MUTF:OIGYX) inception: 09/07/05 |

NAV |

-1.69 |

2.83 |

7.65 |

-2.07 |

6.05 |

4.08 |

6.31 |

|

MSCI ACWI ex USA Index (‘USD’) |

0.96 |

5.69 |

11.62 |

0.46 |

5.55 |

3.84 |

– |

|

|

Total return ranking vs. Morningstar Foreign Large Growth category (Class A shares at NAV) |

– |

– |

69% (266 of 398) |

53% (185 of 383) |

57% (166 of 334) |

83% (185 of 224) |

– |

|

Expense ratios per the current prospectus: Class A: Net: 1.10%, Total: 1.10%; Class R6: Net: 0.73%, Total: 0.73%; Class Y: Net: 0.86%, Total: 0.86%. Performance quoted is past performance and cannot guarantee comparable future results; current performance may be lower or higher. Visit Country Splash for the most recent month-end performance. Performance figures reflect reinvested distributions and changes in net asset value (NAV). Investment return and principal value will vary so that you may have a gain or a loss when you sell shares. Returns less than one year are cumulative; all others are annualized. As the result of a reorganization on May 24, 2019, the returns of the fund for periods on or prior to May 24, 2019 reflect performance of the Oppenheimer predecessor fund. Share class returns will differ from the predecessor fund due to a change in expenses and sales charges. Index source: RIMES Technologies Corp. Had fees not been waived and/or expenses reimbursed in the past, returns would have been lower. Performance shown at NAV does not include the applicable front-end sales charge, which would have reduced the performance. Class Y and R6 shares have no sales charge; therefore performance is at NAV. Class Y shares are available only to certain investors. Class R6 shares are closed to most investors. Please see the prospectus for more details. For more information, including prospectus and factsheet, please visit Invesco.com/OIGAX Not a Deposit Not FDIC Insured Not Guaranteed by the Bank May Lose Value Not Insured by any Federal Government Agency |

Read the full article here

")