")

")

Thesis

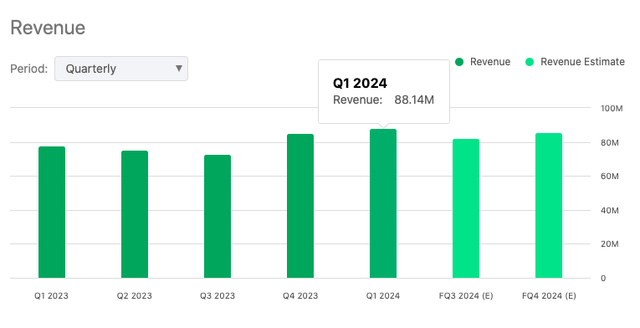

DoubleDown Interactive (NASDAQ:DDI), a top player in digital games, reported exceptional numbers in Q2 2024. They reported GAAP EPS of $13.39 and revenue of $88.24 million, beating expectations by $4.8 million. And despite a tough market, DoubleDown outperformed, with growth in their social casino games. My analysis shows the company’s strong financials and smart moves, like buying SuprNation, set them up to seize market opportunities and close the gap between their current low value and what they’re really worth.

About DoubleDown Interactive

DoubleDown Interactive is a leader in digital games, specializing in the mobile and web sectors of the industry. Started in 2010, the company is headquartered in Seoul, South Korea. DoubleDown is a pioneer in social casino games—games designed to deliver the “Vegas experience” on your screen. DoubleDown Casino, the company’s flagship game, is played by millions around the world. They have a portfolio of other games such as DoubleDown Fort Knox and DoubleDown Classic Slots, all of which are available on mobile.

Q2 2024 Highlights

DoubleDown Interactive posted solid Q2 2024 results, with revenue hitting $88 million.

Seeking Alpha

To put these numbers in proper perspective, they’re beating the industry trend, which has been on a downward slide. On the earnings call, management noted that Eilers & Krejcik Gaming, a boutique research and consulting firm focused on servicing the gaming equipment industry, saw a big drop in social casino revenue this year. Overall, while online casinos and sports betting are on the rise, social casinos are losing steam, especially as more real-money gambling options pop up. The report says social casinos need to step up their game to win back players and keep their profits steady. But DoubleDown appears to be “stepping up their game” immensely as their social casino games brought in $80.3 million, and the iGaming business, SuprNation, added $7.9 million. This is the third straight quarter of year-over-year growth for their social casino business, up 7% from Q2, 2023.

CEO In Keuk Kim highlighted how the company increased profits and cash flow, she said:

In this second quarter, the social casino business also benefited from our initiative to provide players with greater options to buy chips from direct channels. Revenues from these efforts, which benefit our profitability are beginning to ramp noticeably. In summary, our strategy for social casino is to continue enhancing the entertainment value of DoubleDown Casino, while remaining disciplined in our user acquisition and R&D spend to drive strong profitability and free cash flow.

The company’s performance is on the up, too. ARPDAU (average monthly revenue per payer and payer conversion rate) shot up 27% year-over-year to $1.33. The payer conversion ratio climbed to 6.7% from 6.0% last year. Average monthly revenue per payer also jumped 23%, hitting $288, up from $235 in Q2 2023.

Turning back to SuprNation for a moment, the online casino DoubleDown purchased back in November 2023 for $36.5 million appears to be paying dividends. The company plans to use its game development and marketing skills to grow it even further by boosting profits while balancing growth and cash flow over the coming quarters.

CEO In Keuk Kim stated:

In this business (SuprNation), we believe we have many opportunities to leverage our core strengths, including our game developer’s expertise in game creation and our marketing platform to scale SuprNation profitably. And over the next several quarters, we expect to continue to find the investment sweet spot in the business to optimize both top-line growth and cash flow generation.

DoubleDown Interactive’s adjusted EBITDA jumped 34%, hitting $37 million with a 41.9% margin, up from 36.7% in Q2 2023. Cash flow from operations was solid at $34.4 million, a big change from last year’s $37.6 million net cash outflow. DoubleDown Interactive closed the quarter with $339 million in cash and investments, and a net cash position of around $303 million. The company is eyeing growth in other gaming areas, looking at both internal projects and possible M&A deals, backed by its strong finances.

Valuation

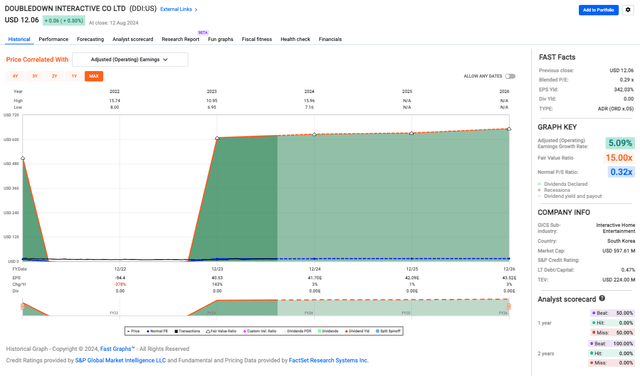

DDI’s current P/E ratio of 0.29x is strikingly low, especially compared to a fair value of 15.00x. This tells me that the market might be seriously undervaluing the company’s earnings, and normally, a P/E this low means the market expects future earnings to either tank or it has bigger worries about the business. But from what’s we’ve just read in the highlights, and an EPS yield of 342.03%, the numbers simply don’t match up with what’s might be considered a “struggling” company. In other words, it looks like the market might be missing something or underestimating the company’s value.

Fast Graphs

The adjusted earnings growth rate of 5.09% shows modest growth. It’s not flashy, but it’s steady. In the unpredictable world of online casinos, steady can be a good thing as it signals consistent performance instead of risky, unsustainable growth. In my view, the big challenge for DoubleDown Interactive is closing the gap between its current market value and its fair value. So If the market starts to see the company’s earnings potential, things could shift upward rapidly.

Risks & Headwinds

The company did hit very minor bumps along the way. Operating expenses climbed to $52 million in Q2, 2024, up from $47.7 million last year. Part of that jump came from the costs of running SuprNation, but things seem to be on the up and up there, so I’m not too concerned. Sales and marketing expenses dropped 15% year-over-year to $11.1 million, and they were down 25% from the previous quarter. But this drop might be less about cost-cutting measures and more about the “fine-tuning” management noted on the call that’s about leveraging their marketing efforts more efficiently.

Most of the sales and marketing are directed toward acquiring new players. Based on the 27% year-over-year increase in ARPDAU, DDI is doing an impressive job. But I did see that the company also chose to extend a $35 million loan from their main shareholder for another two years instead of paying it off. Even though their financials are strong, this suggests they want to keep cash on hand. This doesn’t appear to be about any major bumps down the road, but more about being prudent.

Finally, as mentioned earlier, the social casino segment is dealing with industry-wide challenges. Thus, even with DoubleDown’s recent growth, where companies in the space are seeing declines and DoubleDown is doing better than most, the overall downturn could catch up to them and bring risks down the line. Even though DoubleDown Interactive locked in exclusive licenses for popular IGT games, new competitors with similar deals could affect their market share.

Specifically, the company’s core business still relies heavily on the social casino segment, which is up against shifting consumer preferences and competition from other online gaming options like Sweepstakes. CFO Joseph Sigrist commented that right now DDI is too focused on their own business success, especially with DoubleDown Casino. He couldn’t comment on their peers’ situations, like Sweepstakes, because they’re concentrating on maintaining their momentum in the social casino market.

Rating

I’d call DoubleDown Interactive a “BUY.” They’re a good bet with solid financials, beating earnings, and growing their social casino segment. Grabbing SuprNation was a smart move, and they’re playing it exceptionally well with user acquisition and R&D. Sure, as always, there are some risks in the market, but with their strong cash flow, prudent debt management, low valuation, and steady growth, I think the market’s sleeping on them.

Read the full article here

")

")