")

")

")

Investment Thesis

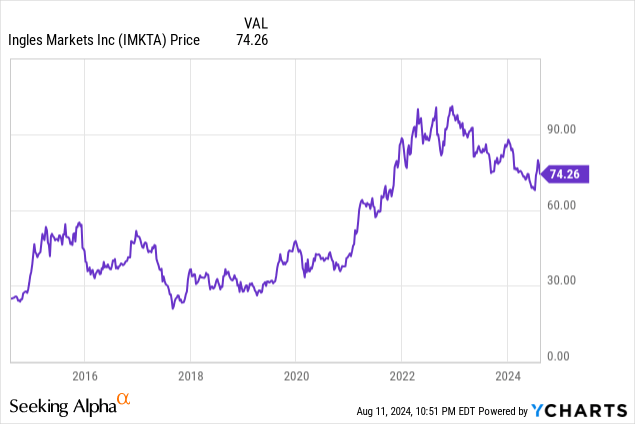

Ingles Market (NASDAQ:IMKTA) is a small American supermarket that has seen a 25% drop from its all-time highs reached at the end of 2022. This is because during COVID-19 it had wider profits than normal, but this has now mostly normalized.

Currently trading quite cheap, but I’d like to see a better growth strategy before recommending a purchase. Therefore, I think it’s a hold.

Business Model

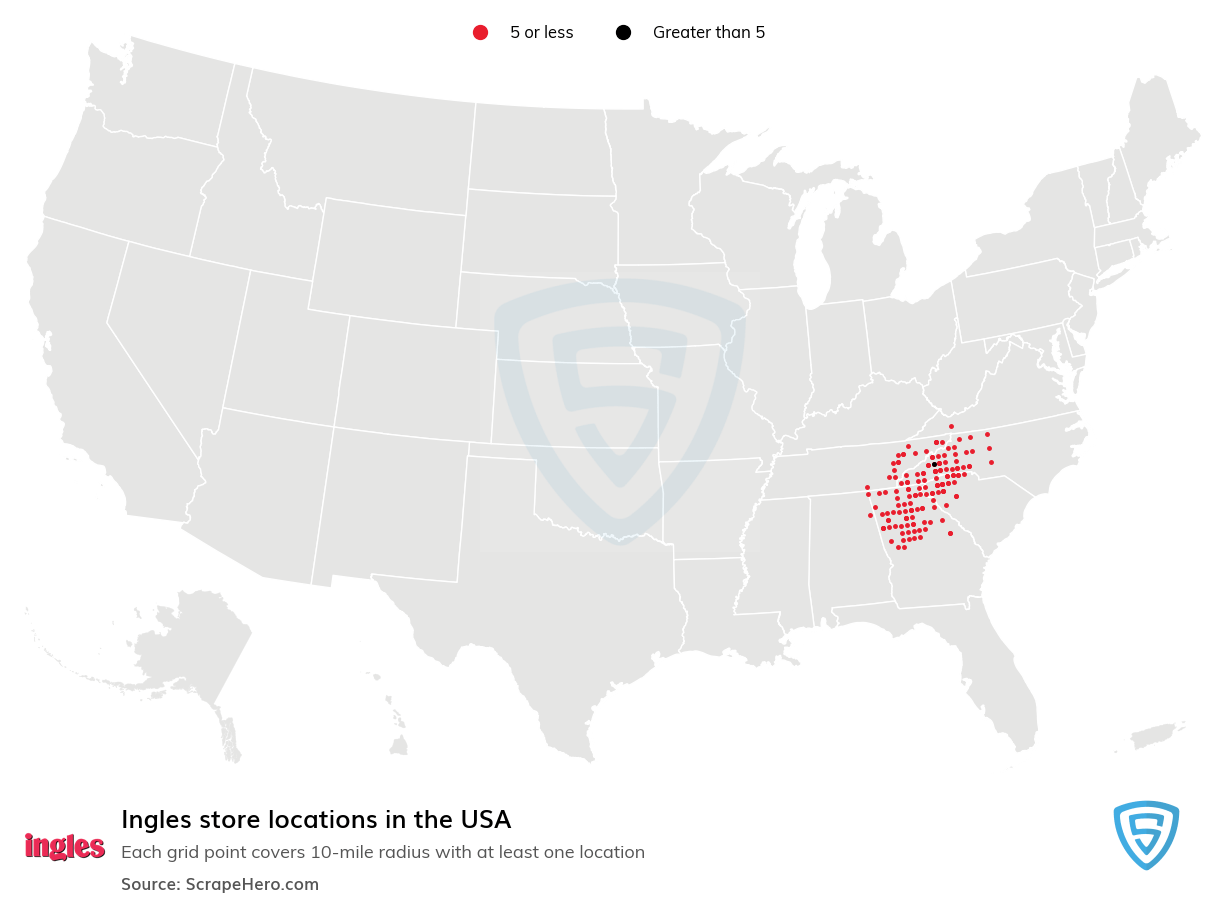

It’s a small supermarket chain that operates in the southeastern United States, especially in less populated regions such as North Carolina, South Carolina, Georgia, and Tennessee.

Despite being small, it was founded in 1963, so it’s the same age as supermarkets like Walmart and older than Whole Foods. However, it clearly hasn’t expanded as much as its peers. In the following map can be seen where its 198 locations are distributed, a number which hasn’t moved at all in the last five years and that’s very far from Walmart’s (WMT) +4,600 stores, Kroger’s (KR) +1,200 or Whole Foods’ +500.

Ingles store locations (ScrapeHero)

This is an aspect that I don’t like so much about the company, since it seems to me that they could be more ambitious and seek to expand the footprint. At the end of the day, you cannot depend solely on raising prices due to inflation, which is why between 2014 and 2019 revenue has grown only 2% annually.

Hidden Value in the Balance Sheet

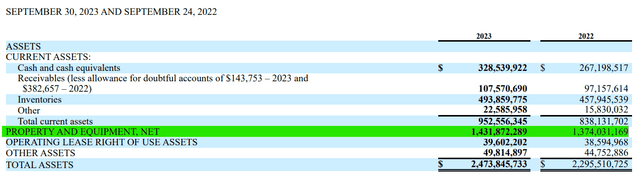

One explanation for why expansion has been so slow (or none, rather) is that the company usually prefers to buy the properties instead of renting the spaces. This requires greater investment to grow; therefore, growth is slower, but it also brings indirect benefits, such as the fact that the company owns $1.4 billion in properties (the same value as the current market cap) because it owns 167 of its 198 supermarkets and also 29 undeveloped sites.

Ingles Markets 10-K

Therefore, the possibility of selling the properties and then starting to rent them and with the surplus cash starting a more aggressive geographical expansion always remains. I don’t think this is going to happen anytime soon and there are no signs of it either, but it is a possibility.

Share Structure

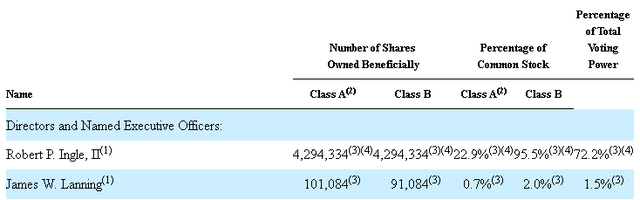

The company has 19 million shares outstanding. As of August 6, 2024, 14.5M shares were Class A and 4.5M were Class B. Class B shares are not listed and have greater voting power, so Mr. Robert P. Ingle II (son of founder Robert Ingle and current chairman of the board) owns almost 23% of the outstanding shares but 72% of the voting power. Meanwhile, the CEO James Lanning owns only 1.5% of voting power, therefore doesn’t have that much relevance in the company’s decisions.

The company pays $0.66 dividend per share for class A shares and $0.60 for class B; therefore, the payout ratio would be 19% in the last twelve months, not the 7.68% indicated in Seeking Alpha, which only takes into account the class A shares. At the current price, the dividend for class A shares would have a yield of less than 1%; therefore, it doesn’t seem so relevant.

Shares ownership (Ingles Markets DEF 14A)

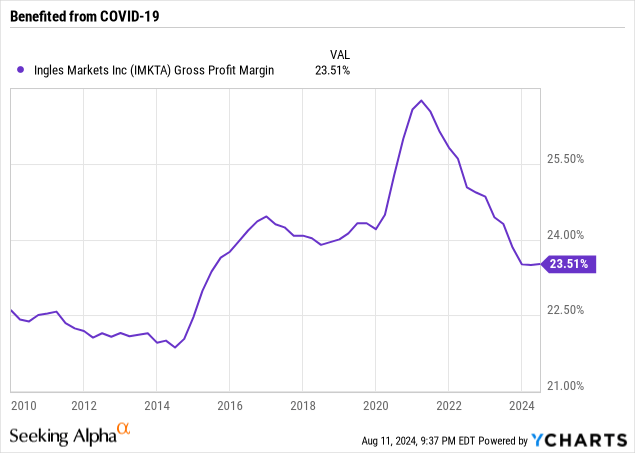

Benefited from COVID-19

For some reason, when the COVID-19 pandemic hit, the company benefited and was able to sell its products with a higher margin than usual. This is especially accentuated in the gross profit margin, which went from 23-24% between 2014-2019 to 25-26% between 2020 and 2022.

This clearly didn’t seem like something sustainable, but it led to excess cash arriving than usual. Now this margin has already normalized, even being a little lower than in 2019, which, personally, I think isn’t permanent either and is an effect of inflation that is now also beginning to normalize. Therefore, I believe that margins should stabilize at the 23-24% mentioned above.

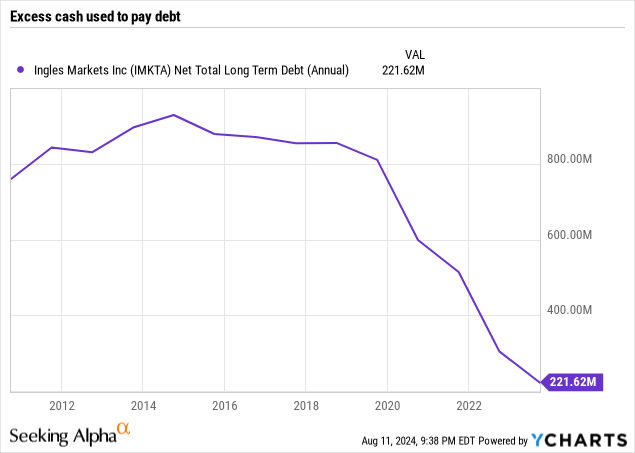

In a rather astute move, management knew that these wide margins wouldn’t be permanent, so it began aggressively paying down debt. In this way, at the end of this positively abnormal period the company emerged with a cleaner balance sheet and with only $221M of net debt, less than 0.7 times the EBITDA of the last twelve months (LTM) or just over 2 times LTM free cash flow.

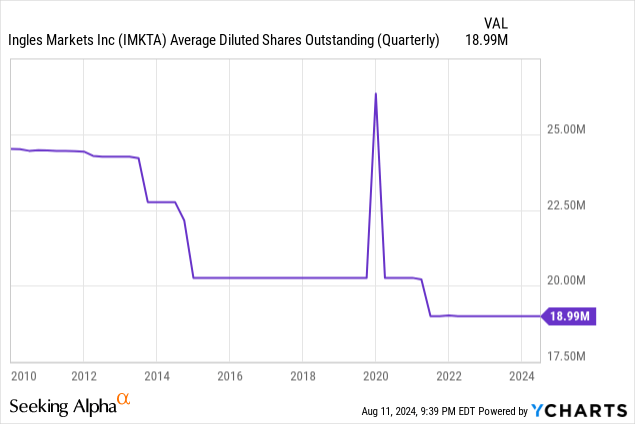

They also took the opportunity to reduce outstanding shares by 6%, something they hadn’t done since the 2013-2015 period.

So, the allocation of capital has been reduced to paying debt, buying properties, and repurchasing shares at very specific times. However, I’d again like to comment that I think this would be a good time to start growing more aggressively now that the balance sheet is clean, and they’re not using the capital for anything else.

Valuation

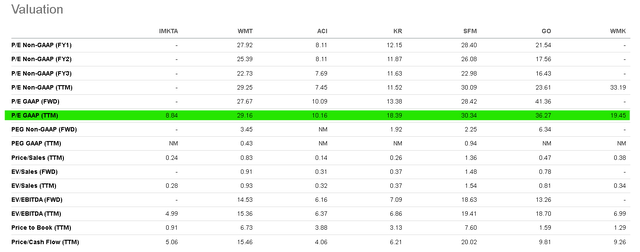

Something that may catch the attention of anyone who starts looking at Ingles Markets is its low valuation. The P/E for the last twelve months is less than 9, while the rest of the supermarkets usually trade at 20 times on average, so I’d like to do a comparison exercise to conclude if this apparently low multiple is deserved or not.

Seeking Alpha

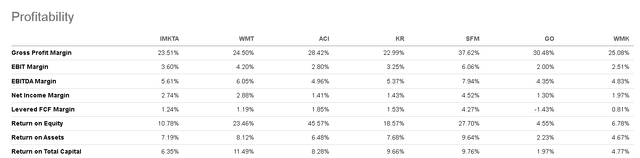

In terms of profitability and considering that the gross margin is already normalized, Ingles Markets is the one with the lowest gross margin, except Kroger, although the EBITDA and net margin are good compared to the rest of the supermarkets.

On the other hand, the returns on capital and equity are not as impressive and are even lower than those of Kroger, a company with worse margins.

Seeking Alpha

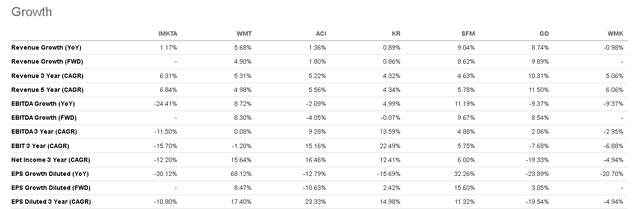

In terms of growth, Ingles is one of those that has grown its revenue the most in the last 5 years, although in the last year, it’s one of the least, and it’s also the only one that has seen its profitability so affected in the last 3 years, decreasing Net Income, EBIT and EBITDA in double digits in this period.

Therefore, while it doesn’t seem to deserve a particularly high multiple since it isn’t the one that stands out the most, it doesn’t seem to be the worst either and the P/E multiple of 8 times (and 11 times FY2024 earnings, according to my estimates) is quite low and would deserve a re-rating to at least 12-15 times earnings.

Seeking Alpha

I think that this year revenue will decrease between 1 and 2% according to what was reported in the first three quarters, this would result in a revenue of $5.8 billion for FY2024. Furthermore, the net margin should normalize to around 2.5%, which would represent a net income of $145 million, divided by the 19M shares outstanding would represent an EPS of approximately $7.5.

With a P/E of 12, the price per share would be around $90 USD, representing an upside of more than 20% from the current price. With a P/E of 15, the price would be around $110 USD, representing an upside of almost 50%.

The Bottom Line

The company has a fairly solid and predictable business; however, I don’t love that they aren’t focused on growing, having so much space within the United States and a balance sheet with very controlled debt.

Despite this, growth and margins look fairly in line with peers, so it appears to be cheap currently even considering normalization of growth and margins, so it could be a buying opportunity. In my case, I prefer to see some fundamental change in the growth strategy first; therefore, I’ll assign a hold rating.

Read the full article here

")

")