(JBFCF)")

(NYSE:PLTR)")

")

This is my initial article on Crinetics Pharmaceuticals, Inc. (NASDAQ:CRNX). It is an interesting clinical-stage biotech with strong liquidity and a hefty market cap of ~$3.81 billion. It is very much a high-risk bet with no product revenue and is entirely dependent on its late-stage therapies not only achieving FDA acceptance but also significant post-approval revenues.

In this article, I review the dynamics of the situation as revealed by its Q2, 2024 earnings reported on 08/08/2024 in its:

- Financial results and business update press release (the “Release”).

- Earnings conference call (the Call”).

- 10-Q (the “10-Q”).

- Presentation (the “Presentation”).

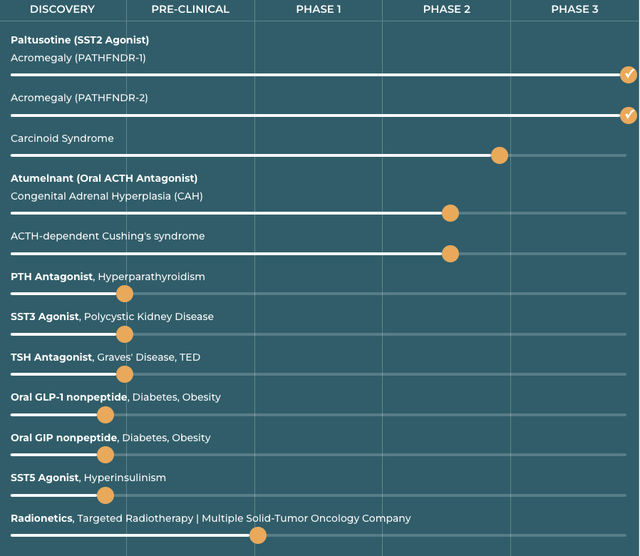

Late stage pipeline encapsulates Crinetics’s entire value proposition

General

Crinetics website accessed 08/08/2024 includes the following pipeline graphic:

crinetics.com

Its latest 10-K (the “10-K”, p. 9) notes that with limited exceptions its product candidates have been:

…discovered and developed internally and … [that it has] retained global rights to commercialize [its]… product candidates and ha[s]… no royalty or licensing obligations…

The noted exceptions refer to the following licenses granted by Crinetics per the 10-K, p. 6:

- Sanwa License — exclusive right to develop and commercialize paltusotine in Japan;

- Radionetics License — exclusive right to its radio therapeutics technology in accordance with the license — this deal is discussed in greater detail below;

- Loyal License — exclusive right to develop and commercialize CRN01941, a separate SST2 agonist licensed to Cellular Longevity Inc., doing business as Loyal, for veterinary use.

Paltusotine

The 10-K (p. 3) describes paltusotine (SST2 Agonist) as Crinetics’ lead therapy establishing:

…a new class of oral selective nonpeptide somatostatin receptor type 2, or SST2, agonists designed for the treatment of acromegaly and carcinoid syndrome associated with NETs. Somatostatin is a 3 neuropeptide hormone that broadly inhibits the secretion of other hormones, including growth hormone, or GH, from the pituitary gland.

Clinicaltrials.gov lists two Crinetics’ phase 3 paltusotine acromegaly trials:

- Pathfinder 1 — NCT04837040 is a small study with an enrollment of 58 subjects with acromegaly previously treated with somatostatin receptor ligand (SRL) based treatment regimens, the actual primary completion date was 07/10/2023;

- Pathfinder 2 — NCT05192382 is a larger trial with an enrollment of 111 treatment-naive subjects, the actual primary completion date was 01/20/2024.

During the Call CMO, CDO Pizzuti gave a run-down on Crinetics’ ambitious plans for paltusotine in the treatment of acromegaly noting:

- It remains on track to submit its NDA for paltusotine in its first indication, acromegaly this year;

-

Based on the success of both Phase 3 PATHFINDER studies, it will seek approval for all patients, including those switching from the standard of care injected SRLs to paltusotine as studied in PATHFINDER-1 and those who are not currently treated as studied in PATHFINDER-2;

-

It is conducting health economics and outcome studies to further demonstrate the value proposition of paltusotine in the treatment of acromegaly to support the commercial team’s efforts as they engage with payers, physicians, and patients.

In sum, it has paltusotine in the treatment of acromegaly all teed up with a near-term NDA filing planned. The first check of how this is progressing will come ~60 days after its NDA filing when the FDA either accepts or rejects the filing.

As for its phase 2 paltusotine trial in the treatment of carcinoid syndrome, in response to a question Pizzuti reminded that it had:

… showed highly statistically significant results demonstrating the potential of paltusitine to treat people living with carcinoid syndrome.

He went on to advise that;

Building on this success, we are preparing to discuss the Phase 2 results with the FDA and align on the design of a Phase 3 protocol. We expect to initiate the Phase 3 trial by the end of 2024.

At this stage, it is far too early to assess a timeline for paltusotine in treatment of carcinoid syndrome. The Presentation slide 9 pegs its launch as an indefinite 2026+.

Atumelnant (CRN04894)

Atumelnant is listed on Crinetics’ pipeline slide above as its second lead therapy in two phase 2 trials in the treatment of congenital adrenal hyperplasia [CAH] and Cushing’s syndrome. Clinicaltrials.gov lists Crinetics’:

- CAH trial as NCT05907291 — a phase 2 trial with an estimated enrollment of 30 and an estimated completion date of 03/2025 and

- Cushing’s syndrome trial as NCT05804669 — a phase 1b/2a trial with an estimated enrollment of 18 and an estimated completion date of 10/2026.

During the call, CEO Struthers was particularly effusive about atumelnant recounting that the:

… Endocrine Society annual meeting in June proved to be an impactful meeting for us. We were thrilled to share highly encouraging initial results from the ongoing Phase 2 studies of our second development candidate Atumelnant in both Congenital Adrenal Hyperplasia and Cushing’s disease. These unprecedented data were very well received by the endocrinology community. This reinforced already strong confidence in the potential of Atumelnant.

He went on to note:

… we are committed to realizing Atumelnant’s full potential as a revolutionary new treatment paradigm for people suffering from CAH and Cushing’s disease.

As was the case for the paltusotine trial in the treatment of carcinoid syndrome Presentation slide 9 lists these as 2026+ launches, only further out in time.

Radionetics

The 10-K, p.7 describes a complicated series of transactions whereby Crinetics joined others in forming Radionetics Oncology. Its purpose was to create a company to develop radiopharmaceuticals for the treatment of a broad range of oncology indications.

Crinetics granted Radionetics a license to its technology for the development of radio therapeutics and related radio-imaging agents. It received an equity stake, milestones up to >$1 billion, and single-digit royalties on net sales. As of 12/31/2024, Crinetics owned a 26% interest in Radionetics.

During the Call Struthers advised that Radionetics had:

…entered into a strategic relationship with Eli Lilly and Company…whereby Radionetics received $140 million upfront, and Lilly obtained a warrant for the exclusive right to purchase Radionetics for $1 billion. Crinetics currently owns approximately 25% of Radionetics. If Lilly were to exercise its right to purchase Radionetics, Crinetics would receive its pro rata share of the $1 billion purchase price. Crinetics is also entitled to single-digit royalties and commercialization milestones for the three programs currently in development at Radionetics.

If Lilly exercises its option that would be a big deal for Crinetics. Not only would it get a part of the purchase price, but its milestones and its royalties would also ramp up in significance.

Ample liquidity supports Crinetics as it works to commercialize its products

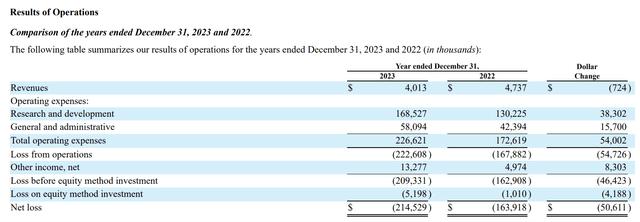

As is clear from the above report, Crinetics is unlikely to see much in the way of product income before 2026. Its results of the operations table from the 10-K show the great financial stresses represented by Crinetics’ current operations:

seekingalpha.com (seekingalpha.com)

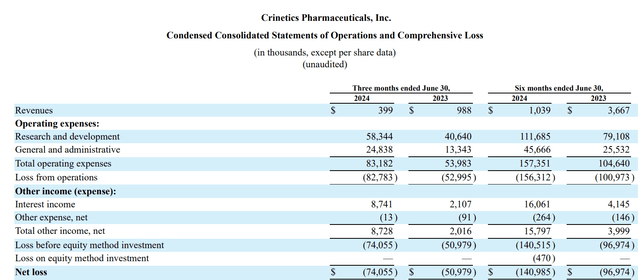

The 10-Q excerpt below shows its latest quarterly results:

seekingalpha.com

In terms of cash burn, the 10-K lists net cash used in operating activities as $166.3 million and $115.2 million for the years ended December 31, 2023, and 2022. The 10-Q (p. 27) provides interesting insights into its cash situation with the following cash flow table:

seekingalpha.com

Cash burn is a multifactor issue. Operationally it’s chewing up cash at a furious clip approaching $200,000 a year. This is in line with CFO Wilson’s expectation of a quarterly cash burn of between $50-60 million for the balance of 2024 as stated in the Call.

Crinetics’ cash runway is more complicated than suggested during the Call

During the Call, CFO Wilson advised:

Crinetics continues to be in a strong financial position, having ended the second quarter with approximately $863 million in cash and investments. Our solid financial foundation is projected to fund our current operating plan into 2028. This includes plans to commercialize paltusitine for acromegaly, the initiation of multiple later-stage clinical trials in additional indications with paltusitine and Atumelnant, as well as continued investment in our pipeline.

This points to a nice clean cash runway into 2028. Under the heading “Liquidity and Capital Resources” the 10-Q, p. 28-29 sets out some risks faced by its shareholders:

Until such time, if ever, as we can generate substantial product revenues to support our cost structure, we expect to finance our cash needs through equity offerings, debt financings, or other capital sources, including potentially collaborations, licenses, and other similar arrangements. To the extent that we raise additional capital through the sale of equity or convertible debt securities, the ownership interest of our stockholders will be or could be diluted, and the terms of these securities may include liquidation or other preferences that adversely affect the rights of our common stockholders. …

Crinetics’ value is a reach that challenges fundamental analysis

When I look at Crinetics, I see definite value in the following:

- Its cash of ~$863 million as of 6/30/2024;

- Its Radionetics stake;

- Its pipeline with a near term-filing planned for paltusotine in the treatment of acromegaly.

I have great difficulty in stretching these to $3.81 billion. To do so requires pegging items 2 and 3 at a combined ~$3 billion. Lacking any timeline on either Lilly’s option or on any milestones it is hard to peg this as supporting any current material sum in my opinion.

The laboring oar to support $3 billion in market cap belongs to paltusotine in treatment of acromegaly. This is a tough one. It depends on FDA approval, always a wild card, and a subsequent successful launch.

During the call, CCO Hassard cited the following attributes it will emphasize during its launch:

The paltusitine data that have been generated to date puts us in a unique position to demonstrate a highly differentiated clinical profile across multiple dimensions, including biochemical control, symptom control, tolerability, and the overall patient experience. We know what is important to patients to the physicians, who treat them, and to the healthcare system, and we believe in the value proposition of paltusitine, which serves each of these constituencies well.

In this regard, potential investors need to be aware of the sobering contents of the “Competition” section on page 15 of the 10-K. It is clear from this section that FDA approval alone will not ensure that Crinetics is a successful investment. If it is approved for the treatment of acromegaly it will launch into a crowded marketplace.

Conclusion

By my estimation I consider Crinetics to be substantially overvalued. This does not automatically make it a “Sell” for current owners. It has strong support on Wall Street as reflected by Seeking Alpha’s Wall Street Analysts’ ratings tab. The Average Price Target of the 14 Wall Street Analysts is $69.00 for a +44.84% Upside.

From a straight metrics point of view based on Seeking Alpha’s biotech quant ratings universe on 08/11/2024 Crinetics is a “Hold”. Although I note that the quant’s grade for valuation is D+.

Conflicted, I am going to rate Crinetics as a “Hold”. Over time, I expect Crinetics to drift lower. However, without a specific catalyst to cause it to reverse its current course, I am loath to urge current owners to reverse their decision and to sell.

I can say with conviction that anyone considering the acquisition of shares in Crinetics should weigh their decision with great care. Forewarned is forearmed.

Read the full article here

(JBFCF)")

(NYSE:PLTR)")

")