(JBFCF)")

(NYSE:PLTR)")

: The Stock’s Selloff Is Overdone")

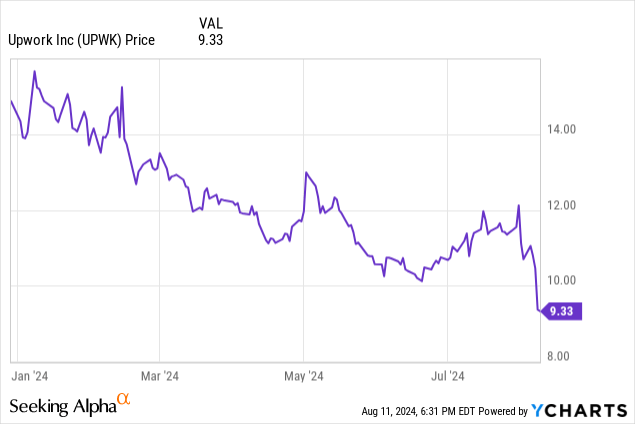

In light of the market shocks that have occurred over the past few weeks on an uncertain U.S. economy and wild rate-driven market activity in Japan, it’s natural that investors are on edge and sending down shares of stocks that didn’t have perfect news to report in Q2. But in many cases, a lot of these selloffs are overdone and not proportional to the news delivered.

Upwork (NASDAQ:UPWK), in my view, is one of these cases. The freelance marketplace has seen a ~20% correction since the start of August, pummeled by its guidance cut in Q2. Year to date, the stock is now down over 30%. It’s a great time, in my view, for investors to re-assess the bull case here.

Macro-Driven Guidance Reduction, but Many Reasons to Stay Optimistic

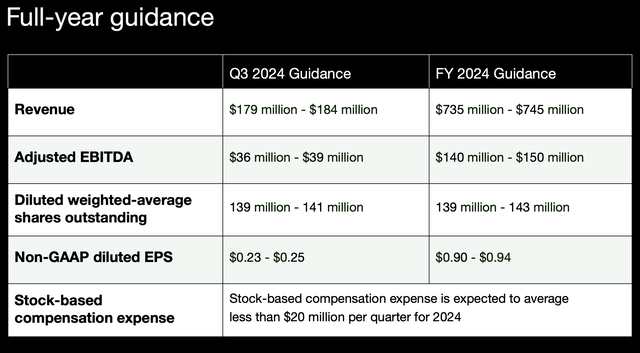

First things first: the main reason that Upwork fell post-earnings was its decision to reduce its full-year growth outlook to $735-$745 million (7-8% y/y growth), versus a much higher prior view of $770-$782 million (12-13% growth). The company attributed this drop to weakening activity among small business customers in the wake of a potential recession, which is the lion’s share of the company’s demand.

Upwork outlook (Upwork Q2 earnings deck)

I last wrote a bullish note on Upwork in June, when the stock was trading in the mid-$10s. While I am disappointed by the guidance cut, I remain at a buy rating here. On top of the appeal of the lower share price, I’m encouraged by the following factors:

- Despite the top-line guidance reduction, Upwork has maintained its $140-$150 million adjusted EBITDA outlook for the year. In fact, it has actually increased its pro forma EPS outlook to $0.90-$0.94, which is two cents higher than the prior range. As a mature tech business, Upwork’s valuation multiples are more based on bottom-line metrics than revenue anyway.

- Upwork is gaining clients despite macro headwinds, while core rival Fiverr (FVRR) is losing clients (more on this in the next section).

- The company also continues to see rapid growth in AI-related work engagements, which showcases that the company is capable of coexisting alongside automation tools.

To me, the fact that Upwork shares have fallen to YTD lows amid a bottom-line guidance increase is a good compromise for the risk of weaker SMB performance and slower top-line growth. At current share prices in the low $9s, Upwork now trades at a market cap of just $1.23 billion. After we net off the $497.7 million of cash and $357.0 million of debt on the company’s latest balance sheet, Upwork’s resulting enterprise value is $1.09 billion.

This puts the company’s valuation multiples at 7.5x EV/FY24 adjusted EBITDA, and 10.1x FY24 P/E – both considerably lower than the market, despite the fact that Upwork is still growing its top line in the double digits.

Beyond these shorter-term drivers and the compelling valuation, here’s a refresher on my longer-term bull case for Upwork:

- Rising take rates and monetization. The company has not only boosted its pricing but it’s also focused on tertiary revenue opportunities such as signing up high-volume freelancers for a premium subscription product and offering Boosted Listings and Boosted Proposals to increase their visibility, for free.

- Active client growth. Despite pricing increases, Upwork has continued to gain active clients, which indicates that the Upwork marketplace is also gaining market share versus rival Fiverr.

- Profitable growth too. Upwork has managed to drive mid-teens growth while at the same time dramatically expanding its adjusted EBITDA margins, the result of focusing on enterprise-oriented sales as well as reducing its headcount.

- Enterprise partnerships. What additionally distinguishes Upwork has been its efforts to strike up meaningful enterprise partnerships that drive revenue and partner-sourced leads. The company has deals with both Microsoft (MSFT) and SAP (SAP) in place, which are some of the largest companies in the software sector.

To me, there’s still a vibrant bull case in Upwork. Stay long here and use the dip as a buying opportunity.

Q2 Download

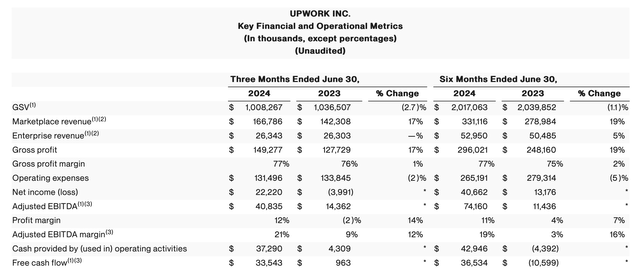

The company’s Q2 earnings print was completely shadowed by its full-year revenue cut and management’s bleaker commentary on the state of the SMB space, but when we put those aside for a moment, we find many things to like about Upwork’s Q2 results. Take a look at the earnings highlights below:

Upwork Q2 highlights (Upwork Q2 earnings deck)

Total revenue grew 15% y/y to $193.1 million, driven by strong expansion in marketplace take rates but tempered by flat y/y enterprise demand. We do note that revenue growth decelerated four points from 19% y/y growth in Q1.

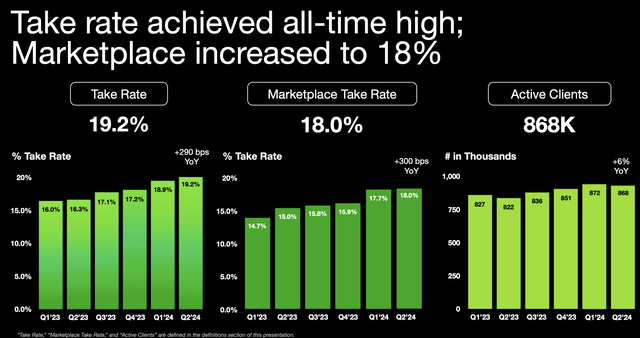

Take rates hit an all-time high at 19.2%, up 290bps y/y. Improving take rates were driven by two main factors: higher adoption of Upwork ads and monetization features, as well as raising subscription pricing for the Freelancer Plus plan, which includes additional AI functionality.

Upwork core customer metrics (Upwork Q2 earnings deck)

But perhaps the most impressive result in Q2 is that Upwork is still growing active clients on a y/y basis to 868k while seeing a sequential decline in active clients of only 4k (a seasonal trend, whereas in the prior-year Q2, the company lost slightly more clients at 5k).

In the same quarter, meanwhile, Upwork’s main rival Fiverr saw a -6% y/y reduction in active buyers (versus Upwork’s +6% y/y), while sequentially it lost 112k active buyers.

Fiverr client trends (Fiverr Q2 shareholder letter)

Macro trends are impacting the entire industry, and industries beyond freelance as well. But to me, the disparity in fortunes between Upwork and Fiverr suggests that Upwork is the more durable platform in the age of AI (and Upwork noted that AI-related work engagements saw 67% y/y GSV growth in Q2).

It’s still useful to consider management’s softer outlook in the context of a softer macro. Per CEO Hayden Brown’s remarks on the Q2 earnings call:

This challenging environment showed through with softer top-of-funnel activity than expected in the second quarter. A leading indicator of this softness that we track internally is clients seeking work, which is a measure of the number of clients engaging in an action that leads to a new contract. In Q1, this number accelerated 11% quarter-over-quarter, while in Q2 this number decelerated 6% sequentially, with particular impact in May and June, along with the mix shift of active clients towards very small businesses. While we applaud the resiliency of smaller businesses outperforming other cohorts on our platform, small businesses’ historical characteristics of lower spend per contract and fewer contracts per client lead us to have more caution about performance expectations for the remainder of the year.

We believe it’s prudent to assume that the changes in client activity due to macroeconomic conditions that we observed in Q2 will remain for the rest of 2024. And we have factored those changes into lowered 2024 full-year revenue guidance, while reiterating our 2024 full-year adjusted EBITDA guidance.”

Still: we can’t ignore the fact that in light of these softer macro trends, Upwork nearly tripled its adjusted EBITDA y/y to $40.8 million, while adjusted EBITDA margins hit 21%, a twelve-point y/y improvement. Pro forma EPS of $0.26 also beat Wall Street’s expectations of $0.23 with 13% upside. So while it’s true that the company is suffering from cyclical macro trends, we should anchor our focus on the profitability metrics that are still improving and providing tremendous valuation support for Upwork.

Key Takeaways

With market share gains and healthier client activity versus Fiverr, a raised pro forma EPS outlook for the year despite lower revenue, and rising AI-related use cases and successful price increases, there’s a lot to like about Upwork, especially as the recent dip has dropped the stock to deep value levels. Stay long here and buy the dip.

Read the full article here

(JBFCF)")

(NYSE:PLTR)")

")