")

Thesis

The New America High Income Fund (HYB) is a fixed income closed end fund we have covered extensively in the past, with our last piece highlighting the reasons for which we were holding the name as part of our portfolio (kindly note the disclosure in the article that we actually owned the security). The article articulated our reasons for continuing to hold, including the large discount to NAV, the conservative fund build and our thoughts on how to run down some of the leverage given the fund composition.

If you were a holder of the name, you would have noticed a large +7% jump in price on Friday, August 9, 2024. In this article, we are going to analyze the background for such a significant one-day move and articulate what holders should do give the current changes.

Saba does it again, managing to close the discount via a corporate action

Saba Capital is an activist hedge fund that focuses on closed end funds (‘CEFs’). We have covered the name in the past in respect of large positions taken by the fund in certain beaten down CEFs, and the subsequent price action (see our piece on the MLP CEF EMO).

With HYB, we have another successful corporate action undertaken by Saba:

The New America High Income Fund, Inc. ((NYSE: HYB)) has announced a proposed reorganization into the T. Rowe Price High Yield Fund, subject to shareholder approval at the Annual Meeting in November 2024. The Fund’s Board of Directors has approved this proposal, and shareholders will receive a combined proxy statement and prospectus with detailed information in Q3 or Q4 2024.

Additionally, the Fund has entered into a standstill agreement with Saba Capital Management, L.P. Under this agreement, the Board will work to secure shareholder approval for the reorganization, while Saba has agreed to withdraw its director nominations and vote in favor of the reorganization and director elections.

The T. Rowe Price High Yield Fund (PRHYX) is an open-ended mutual fund from T. Rowe, and thus does not have the same structural issues presented by a CEF. By merging the CEF into a mutual fund, Saba has managed to instantaneously close down the discount to NAV:

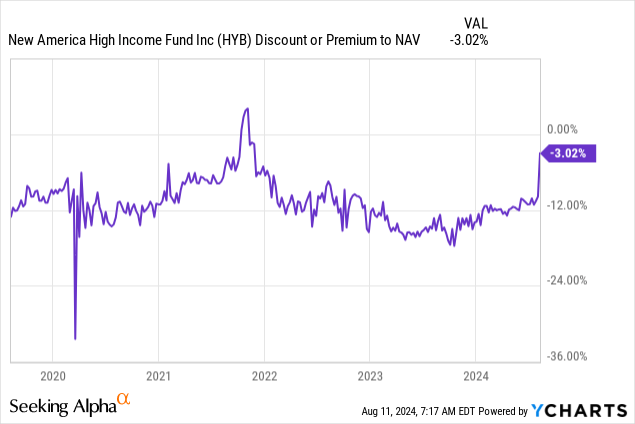

We can see the CEF usually trading at a long-term discount to net asset value of roughly -12%, with the zero rates period in 2021 being the only point in time when the fund was flat to NAV.

Saba fulfills a very important role in the market, namely closing unjustified arbitrage opportunities. Closed end funds, by definition, are management companies with a set number of shares outstanding, and more often than not, their way of running the business goes unchecked outside the discount or premium assigned by the market. If an individual retail investor has an issue with the way a CEF is run, they have very little sway in making any changes.

Large funds like Saba can leverage their expertise and lawyers to take a large position in a CEF and then try to implement corporate changes in order to force the management company to take actions favorable to the shareholders. Ultimately, they do what small investors cannot, and when they are successful, all shareholders benefit, just like in this case.

The large one-day move we saw on August 9, 2024, was not driven by credit spreads or market risk-on moves, but by the announced corporate action which signaled the CEF will trade flat to NAV very soon. Via their structures, open-ended funds do not allow for large discounts to net asset values; thus the market is now pricing for HYB to be priced at the value of its assets. There is still a small discount left, allowing for the probability of the corporate action not going through. We are of the opinion that the action will move through swiftly, and we will see the last 3% gap closed as well.

What happens next?

As per the corporate action announcement, while the Board of Directors has approved the merger, it is still subject to shareholder approval. The proxy materials will be sent out, and a vote will take place. We are of the opinion that shareholders will vote in favor of the merger; otherwise they might see the price of the CEF immediately drop back down by -7% or more.

While HYB does not need to take any actions until the corporate action is fully validated by shareholders, we believe we will witness some reduction in leverage going forward, since an approval of the corporate action will actually result in the elimination of the entire leverage position. Since the fund does not have term funding but rolls repos, the un-leveraging should be fairly straightforward.

How can a retail investor take advantage of the Saba IP

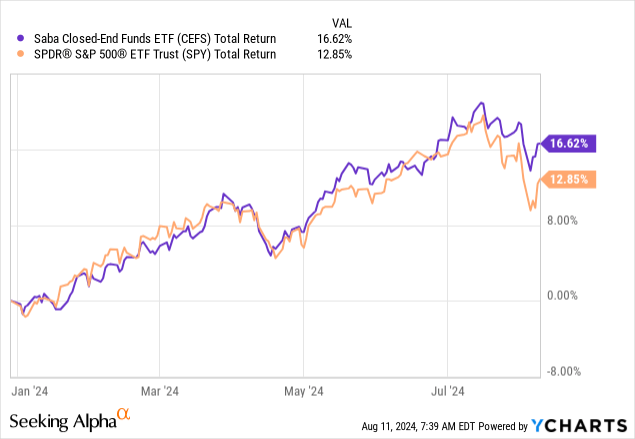

There are several ways to profit from the corporate actions undertaken by Saba. A very straightforward way is to invest in their exchange-traded fund Saba Closed-End Funds ETF (CEFS) which contains many names where they are actively trying to close down unjustified discounts to NAV.

CEFS is up 16.6% this year from a total return perspective, beating the S&P 500:

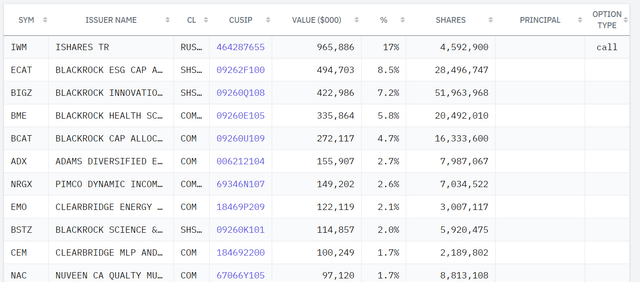

A second way of investing along-side Saba is via their 13-F filings, which can be found here. Per the Q1 2024 filing, the following are the largest positions held by the fund:

13F (13f.info)

Investors can scour the next 13-F filing for the latest additions to the fund, to the extent Saba does not publicly disclose them as part of their corporate actions campaign.

Conclusion

HYB is a fixed income closed end fund. The vehicle has historically traded at a large -12% discount to NAV due to the actions taken by the CEF management team. The fund had a brief period of trading at NAV during the 2021 zero rates environment, but moved back to a large discount in 2022. The fund was targeted by activist hedge fund Saba Capital, which took a position in the name in order to target the presented arbitrage opportunity. Subject to shareholders’ approval, the CEF is set to merge into the T. Rowe Price High Yield Fund. This corporate action was responsible for the CEF’s large one-day gain of 7% on Friday, August 9, 2024. There is still a small 3% NAV gap to be filled, a gap which accounts for the probability of the corporate action not going through. We are of the opinion that shareholders will approve the merger and the gap will be filled as well. The article also presents several methods of following Saba’s strategies.

Read the full article here

")

(JBFCF)")

(NYSE:PLTR)")