")

Immunocore Holdings plc (NASDAQ:IMCR) is a commercial-stage biotechnology company that develops immunotherapies for cancer, infectious diseases, and autoimmune conditions. Its leading commercial product, KIMMTRAK, is a bispecific protein for HLA-A*02:01-positive adults with unresectable or metastatic uveal melanoma. KIMMTRAK is currently approved in 38 countries, including the US, EU, Canada, Australia, and the UK, showing a promising revenue trajectory in 2024. Additionally, IMCR has a diverse pipeline with IMC-F106C for cutaneous melanoma, IMC-M113V for HIV, and several other drug candidates at various clinical trial stages. I believe IMCR’s financials are robust, with positively trending cash flow figures. Despite its premium valuation risks, I ultimately rate IMCR as a “buy” for long-term investors who understand the embedded biotech risks.

KIMMTRAK: Business Overview

Immunocore is a commercial-stage biotech company headquartered in Abingdon, United Kingdom. IMCR was founded in 1999 and went public in February 2021. It specializes in immunotherapies for cancer, infectious diseases, and autoimmune conditions. IMCR’s IP portfolio includes tebentafusp-tebn, commercially known as KIMMTRAK. It is a bispecific protein indicated for HLA-A*02:01-positive adult patients with unresectable or metastatic uveal melanoma.

Source: Corporate Presentation. June 2024.

KIMMTRAK is approved in the US, the EU, Canada, Australia, and the UK and has regulatory clearance in 38 countries. KIMMTRAK targets gp100, an antigen expressed in melanocytes and melanoma cells. The protein combines a soluble T cell receptor [TCR], which binds to cancer cells, with an anti-CD3 effector function that activates T cells against targeted cancer cells. It’s worth highlighting that KIMMTRAK is the first FDA-approved targeted treatment specifically for metastatic uveal melanoma, a type of aggressive melanoma affecting the eye. Previously, available therapies for uveal melanoma often focused on managing symptoms rather than directly addressing the melanoma itself.

More recently, in June 2024, IMCR announced new Phase 2 and Phase 3 trial data showcasing KIMMTRAK’s promising results for uveal melanoma. The Phase 2 trial enrolled 26 patients, from which six had a partial response. Patients showed reduced tumor sizes, reduced circulating tumor DNA (ctDNA), and increased survival rates. Phase 3 included patients treated with KIMMTRAK and achieved stable disease or tumor reduction, with a median duration of 11 months. This duration was similar to patients with a partial or complete response. This data corroborates KIMMTRAK’s effectiveness for tumor reduction and increasing survival rates. Thus, KIMMTRAK looks promising for patients with partial or complete responses and those with stable disease.

Beyond KIMMTRAK: Promising Pipeline

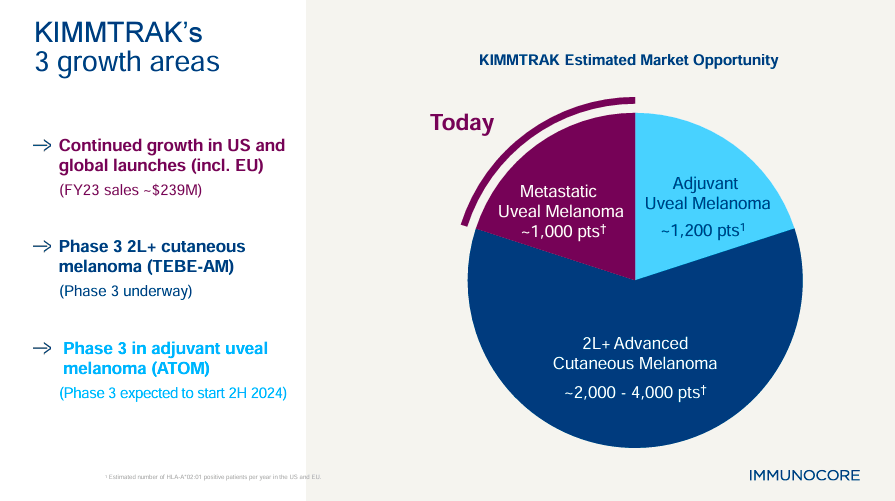

Moreover, IMCR’s pipeline includes three overarching programs in oncology, infectious diseases, and autoimmune conditions. In oncology, IMCR’s ATOM trial investigates KIMMTRAK for an additional indication in adjuvant uveal melanoma. This treatment could prevent recurrence in patients treated with primary therapy for uveal melanoma. Note that this oncology program is sponsored by the nonprofit European Organization for Research and Treatment of Cancer [EORTC]. Currently, ATOM’s Phase 3 trial is expected to commence by 2H2024.

Source: Corporate Presentation. June 2024.

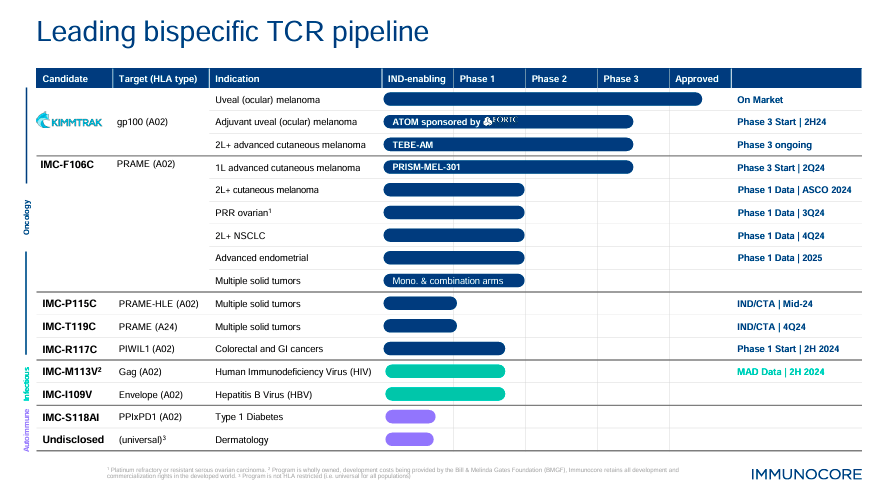

Additionally, IMC-F106C targets PRAME, an antigen different from gp100. PRAME is an antigen expressed in melanoma, so IMC-F106C theoretically helps the immune system detect and kill cancer cells expressing this antigen. It’s also worth mentioning that while Tebentafusp (KIMMTRAK) specifically benefits patients with the HLA-A*02:01 allele, IMC-F106C is designed to target PRAME-expressing cancers. Therefore, IMC-F106C could provide extra therapeutic benefits in broader patient populations, potentially including both first-line and second-line settings. So, if IMC-F106C is successfully developed and commercialized, it could have an even greater market acceptance than KIMMTRAK, making it an important value driver for IMCR.

Source: Corporate Presentation. June 2024.

On the other hand, IMCR’s pipeline includes IMC-P115C for solid tumors, with an Investigational New Drug/Clinical Trial Application [IND/CTA] planned for mid-2024. Also, IMC-T119C for solid tumors with IND/CTA is expected in Q4 2024. IMC-R117C targets colorectal and gastrointestinal [GI] cancers and has Phase 1 trials planned for 2H2024. Additionally, IMC-M113V is indicated for Human Immunodeficiency Virus [HIV], with multiple ascending doses [MAD] data from Phase 1 expected by 2H2024. Lastly, IMCR has IMC-I109V for hepatitis B Virus [HBV] in Phase 1 and IMC-S118AI for Type 1 diabetes in preclinical stages. IMCR also has an undisclosed dermatology drug candidate in preclinical trials.

Interestingly, during IMCR’s latest earnings call, management highlighted the PRISM-MEL-301 Phase 3 trials evaluating Tebentafusp in combination with nivolumab. This would be a first-line treatment of advanced cutaneous melanoma. IMCR also noted its TEBE-AM trials on KIMMTRAK with pembrolizumab as a second-line therapy for advanced cutaneous melanoma. It’s worth mentioning that IMCR also stated that its IMC-M113V Phase 1 trial enrolled three cohorts for HIV treatment.

Source: Corporate Presentation. June 2024.

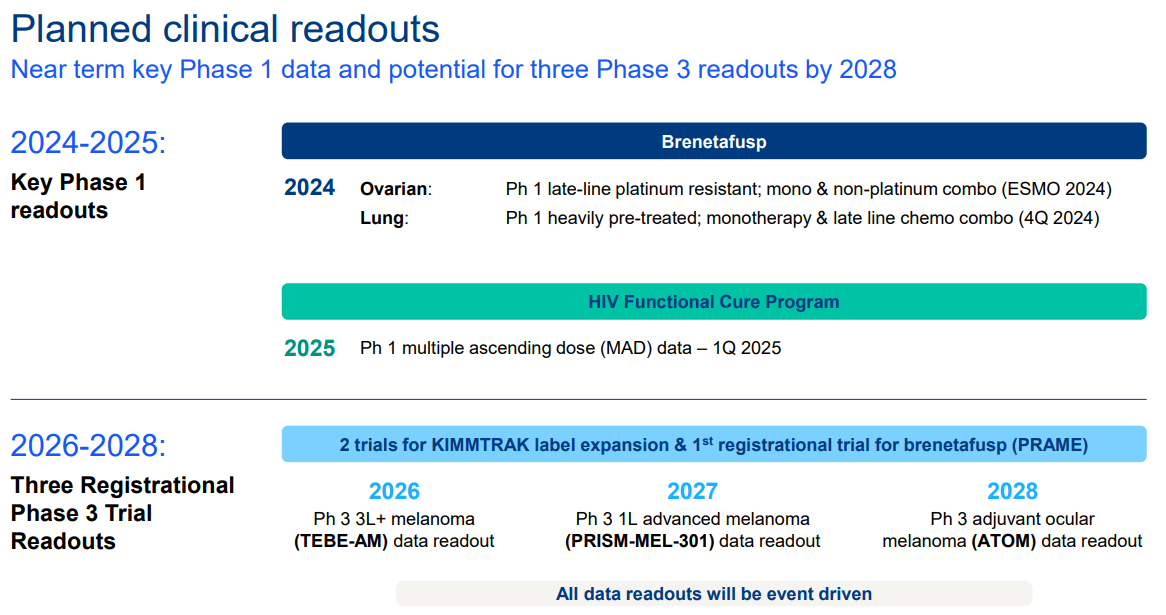

This trial’s approach is an immunotherapeutic strategy targeting CD4+ cells, which serve as reservoirs for persistent HIV infection. The therapy could theoretically reduce the number of persistently infected CD4+ cells to achieve sustained viral suppression. If further testing corroborates such results, it could pave the way towards a potential functional HIV cure. But for the most part, IMCR’s strategic focus appears to be centered around KIMMTRAK’s commercialization and extending its approval across more jurisdictions. Hence, I think it’s reasonable to conclude that KIMMTRAK is the company’s main value driver at the moment.

Worth the Premium: Valuation Analysis

From a valuation perspective, IMCR has a market cap of $1.9 billion, making it a relatively mid-sized biotech in its sector. Its balance sheet holds $505.0 million in cash and equivalents and $354.6 million in marketable securities. IMCR’s total available short-term liquidity is $859.6 million, compared to $438.1 million in long-term loans. Also, its book value is now $359.1 million, resulting in a P/B multiple of 5.2. For comparison, the sector’s median P/B is 2.4, indicating that IMCR appears relatively expensive.

Nevertheless, I estimate IMCR generated a positive cash flow in Q1 2024 of roughly $23.2 million by adding its CFOs and Net CAPEX. Still, if we look at its quarterly TTM figures, it has a cash burn of $15.1 million using the same approach. This suggests that IMCR is becoming a more sustainable company, but I’ll use the TTM figures for a more conservative cash runway estimate. In my view, $15.1 million in TTM cash burn seems tiny compared to its available short-term liquidity of $859.6 million, indicating that IMCR has adequate financing for the foreseeable future.

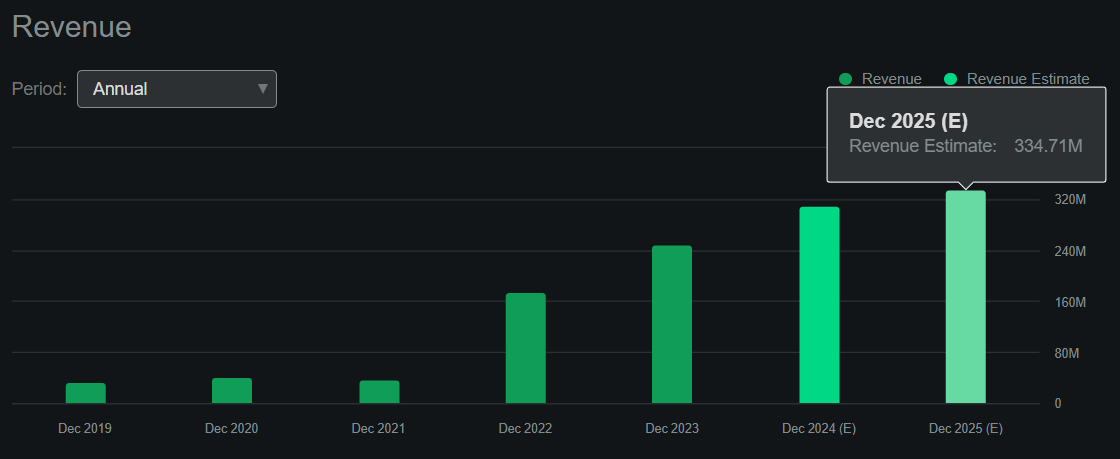

Source: Seeking Alpha.

Additionally, according to Seeking Alpha’s dashboard on IMCR, the company should generate $334.7 million in revenues by 2025. This would represent an 8.0% YoY increase in 2024, which is promising but slightly below the sector’s median revenue growth of 8.7%. However, such a top-line increase, coupled with its promising cash flow signs, suggests IMCR is well-positioned to start compounding shareholder value through its IP. Still, it also implies a forward P/S multiple of 5.6, which again is higher than the sector’s median forward P/S ratio of 3.6.

Source: Corporate Presentation. June 2024.

Consequently, I think it’s reasonable to conclude that IMCR is somewhat expensive at this juncture. However, it also appears financially robust, and key metrics are trending positively. In the short term, the stock might need to digest its current premium valuation, but it has the ingredients to deliver shareholder value over the long run. Especially because its IP is diverse and KIMMTRAK is commercially promising, so IMCR could also be a viable takeover target for larger pharmaceutical companies looking to strengthen their IP portfolios. Therefore, I lean bullish on IMCR, rating it a “buy” for investors who understand the embedded biotech risks.

Investment Caveats: Risk Analysis

Naturally, the main risk to the bull case is KIMMTRAK, which is IMCR’s primary revenue source. While IMCR generates some collaboration revenues, product sales still account for over 99% of the company’s revenues. Thus, if KIMMTRAK’s market acceptance declines or the company fails to achieve its commercial objectives, it could lead to a P/S compression and shareholder losses. Additionally, IMCR’s current premium valuation may already reflect its potential as a takeover candidate. If management were to dismiss this possibility, it could cause a stock price decline due to reduced speculative appeal.

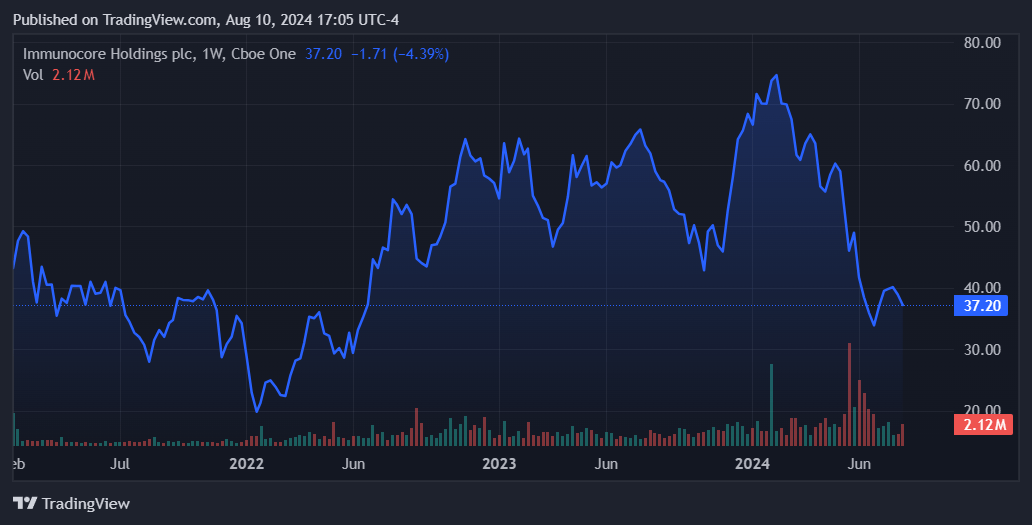

Source: TradingView.

It’s important to note that IMC-F106C and IMC-M113V still carry considerable clinical trial risks, unlike KIMMTRAK. This portion of the company’s IP portfolio is less proven, so disappointing trial data could lead to the discontinuation of these research projects. This would also negatively impact the company’s investment appeal, which, coupled with its premium valuation, could lead to significant downside. Nevertheless, IMCR’s robust balance sheet and steady revenue growth somewhat mitigate these risks. Over the long run, IMCR is well-positioned to navigate the inherently risky biotech landscape and deliver shareholder value.

Premium “Buy”: Conclusion

Overall, I think IMCR is a promising biotech with a commercially proven product with KIMMTRAK. It also has a diverse IP portfolio across oncology, infectious diseases, and autoimmune conditions, which adds to its potential takeover candidate appeal. IMCR’s financials also appear robust, and its cash flow is trending positively. Despite the valuation risks I discussed, I think IMCR ultimately emerges as a viable “buy” for long-term investors who understand the inherent biotech risks.

Read the full article here

")

(JBFCF)")

(NYSE:PLTR)")