")

")

There are several different traits that play a role in successful investing. One of the most important, I have found, is remaining honest with yourself. And another is being intellectually flexible in order to incorporate new data in as unbiased way as possible. When the picture changes, your stance on a situation should change. And even though I am far from perfect in this regard, I do my best to embody both of these traits when I put on my investment hat.

This article is an exercise in this vein. You see, back in November 2023, I wrote a bullish article about Haverty Furniture Companies (NYSE:HVT), a fairly small player in the retail furniture space. Even at that time, the company was showing a weakening of financial results. Despite this, the surplus cash position of the company, combined with how cheap shares were, caused me to rate the company a ‘buy’. But since then, shares have risen by only 5.7% at a time when the S&P 500 has spiked by 20.1%. Looking into the most recent data provided by management, I almost reaffirmed my bullish stance on the company, thanks largely to the firm’s surplus cash position. But when you look at the picture a bit deeper, I think it’s time to acknowledge that this is a prospect that just didn’t play out well, and it has too much going against it to justify a bullish outlook. Because of this, I’ve decided to downgrade the company to a ‘hold’ until such time that we see some meaningful improvements.

A Tough Time For Haverty Furniture Companies

Author – SEC EDGAR Data

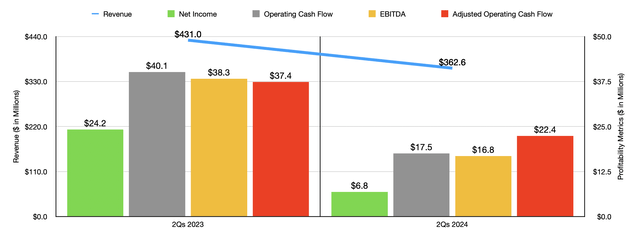

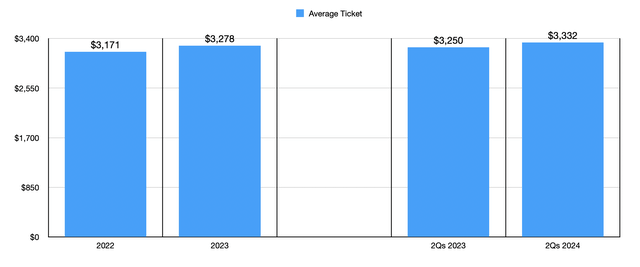

When I last wrote about Haverty Furniture Companies late last year, we only had data covering through the third quarter of the 2023 fiscal year. Results now extend through the first half of 2024. That might be a good place for us to start. During the first six months of the 2024 fiscal year, revenue for the company came in at $362.6 million. That represents a decline of 15.9% compared to the $431 million the business reported just one year earlier. This came about in spite of the fact that the average ticket size in the firm’s stores grew from $3,250 to $3,332. That is an increase of 2.5%. The real pain for shareholders, then, came from a decline in comparable store sales in the amount of 16.2%. With average ticket size growing, this decline can only be attributable to a reduction in overall traffic.

Author – SEC EDGAR Data

This kind of space is low margin in nature. And when revenues contract, especially because of a decline in comparable store sales, margin contraction is the raw as opposed to the exception. And that is exactly what we can see here. Net income in the first half of 2024 was a paltry $6.8 million. That was well below the $24.2 million reported the same time one year earlier. All other profitability metrics followed net profits lower as well. Operating cash flow was cut by more than half, from $40.1 million to $17.5 million. If we adjust for changes in working capital, we get a drop from $37.2 million to $22.4 million. And lastly, EBITDA for the business declined from $38.3 million to $16.8 million.

Author – SEC EDGAR Data

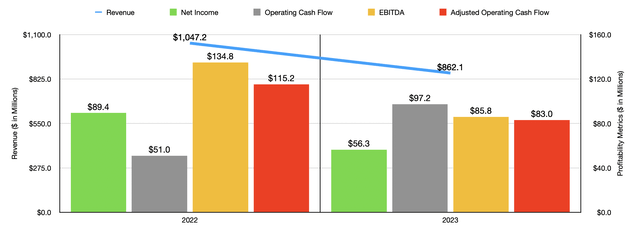

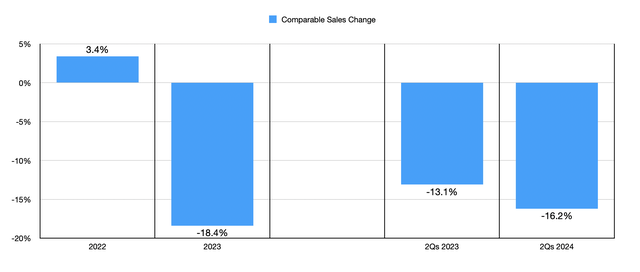

2024 is not the only time that has been difficult for the company. If you look at the chart above, you can see financial performance for 2023 relative to 2022. Revenue dropped 17.7% from $1.05 billion to $862.1 million. This was in spite of the fact that the average ticket size grew nicely from $3,171 to $3,278 for a year-over-year gain of 3.4%.

Author – SEC EDGAR Data

However, comparable store sales plummeted 18.4%. That compares to the 3.4% improvement in comparable store sales seen from 2021 to 2022. The drop in revenue brought with it declining profits and cash flows. The one exception to this was operating cash flow, which nearly doubled from $51 million to $97.2 million. But once we adjust for changes in working capital, we get a drop from $115.2 million to $83 million. This overall trend is disconcerting to say the least.

Author – SEC EDGAR Data

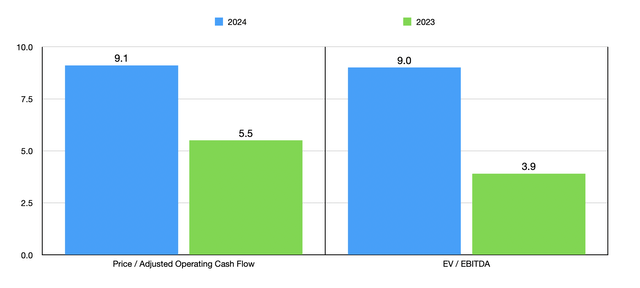

One of the two positive things about the company has been the fact that shares are quite cheap. In the chart above, you can see how the stock is valued using historical results from 2023. You can also see how the stock is valued using projected figures for 2024. These projections were taken by just annualizing the results seen for the first half of the year. But even in that case, shares look decently priced. In the table below, I then compared Haverty Furniture Companies to five similar enterprises. If we use the 2023 figures, then only one of the companies was cheaper than Haverty Furniture Companies on an EV to EBITDA basis. Meanwhile, using the price to operating cash flow approach, we get three of the five being cheaper than it. The ranking for price to operating cash flow remains unchanged if we use the 2024 estimates. But the EV to EBITDA ranking does change, with three of the five companies being cheaper than our candidate.

| Company | Price/Operating Cash Flow | EV/EBITDA |

| Haverty Furniture Companies | 9.1 | 9.0 |

| The Aaron’s Company (AAN) | 3.1 | 0.9 |

| Hooker Furnishings (HOFT) | 4.4 | 8.0 |

| Sleep Number (SNBR) | 35.1 | 11.8 |

| Kirkland’s (KIRK) | 2.2 | 9.8 |

| Arhaus (ARHS) | 10.1 | 8.4 |

Another really positive thing about the company is the fact that cash and cash equivalents is quite large. The company has $116.1 million allocated to cash. And it has no debt on its books. For a company with a market capitalization of only $452.8 million as of this writing, this can definitely be considered a positive for shareholders. This means that the firm does have plenty of capital at its disposal should times get tougher. But hopefully, it won’t come to that.

Author – Federal Reserve Data

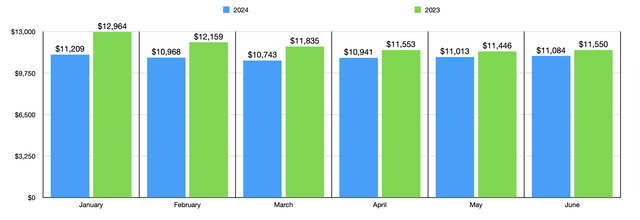

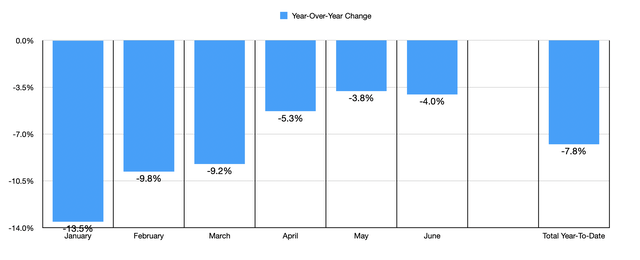

Revisiting the business, I initially thought that I would keep the company rated a ‘buy’, not only because of how cheap shares are, but also because of the surplus cash. All the company has to do is wait out this pain and it should be fine. This thought process was initially bolstered by the chart above. In it, you can see the month-to-month advance retail sales for the US, calculated by the Federal Reserve. In the chart below, you can see the year-over-year decline in overall sales for the first six months of this year compared to the first six months of last year. Even though overall sales are worse this year compared to last, the picture is gradually improving. In January, when things were at the worst, year over year sales were down 13.5%. And while the month of May was better, the decline seen in June was only 4%. This does show a gradual trend toward improvement from one month to the next. And that could be a sign of a turnaround.

Author – Federal Reserve Data

The deciding factor for me was the revelation of just how much worse comparable store sales declines have been for Haverty Furniture Companies than they are for the industry as a whole. Remember, earlier in this article, I mentioned that the comparable store sales decline for the first half of 2024 was 16.2%. That is significantly worse than the 7.8% drop seen by the industry as a whole for the first six months of this year. This indicates to me that Haverty Furniture Companies is in a worse position than the industry more broadly. This is worrisome to say the least. You don’t want to be the ugly duckling in an industry that is already facing problems.

Takeaway

As much as I would like to cling on to my original thesis, I don’t think that would do me or you any favors. To be clear, there are some positive signs that we are seeing when it comes to Haverty Furniture Companies and the furniture industry more broadly. But results have gotten quite a bit weaker, and the comparable store sales decline experienced by Haverty Furniture Companies has been significantly worse than what was seen for the industry. Despite all of the positives, I think that these negatives offset that enough to justify a downgrade to a ‘hold’ rating.

Editor’s Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.

Read the full article here

")

(JBFCF)")

(NYSE:PLTR)")