")

")

")

We previously covered Blue Bird Corporation (NASDAQ:NASDAQ:BLBD) in May 2024, discussing its robust prospects, thanks to the pent-up demand for school bus replacements after multiple delays over the past three years.

Combined with the improved sales across electric/ low-emission school buses against its competitors, compared to the massive electrification trend over the next decade, we had initiated a Buy rating upon a moderate retracement for an improved margin of safety.

Since then, BLBD has retraced by -13.9%, well underperforming the wider market at +1.2%, as the market rotated from high growth stocks and sentiments turn pessimistic attributed to numerous market forces.

Even so, we believe that the stock continues to offer a compelling investment thesis for those seeking to buy the dip, thanks to the management’s raised FY2024 guidance and promising FY2027 projections, which have been well supported by the growing multi-year backlog.

We shall discuss why we are maintaining our Buy rating here.

Growing Confidence In BLBD’s Long-Term Investment Thesis

BLBD 1Y Stock Price

Trading View

With the $65B Bipartisan Infrastructure Law signed into law on November 15, 2021, BLBD had finally started to reap those rewards since December 2023 as the management reported robust FY2023 results and raised their FY2024 guidance.

This was attributed to the $5B allocated for the Environmental Protection Agency’s Clean School Bus Program between FY2022 and FY2026, aimed to replace existing school buses with zero-emission and clean school buses.

This development has already triggered BLBD’s double beat FQ3’24 earnings call, with overall revenues of $333.4M (-3.6% QoQ/ +13.2% YoY) and adj EBITDA of $48.2M (+5.2% QoQ/ +72.1% YoY).

At the same time, the flattish unit delivery of 2,151 unit (-4.5% QoQ/ +0.6% YoY) also imply higher estimated ASPs of $143.20K (+1.5% QoQ/ +13.2% YoY) while resulting in the much richer FQ3’24 adj EBITDA margins of 14.4% (+1.2 points QoQ/ +4.9 YoY).

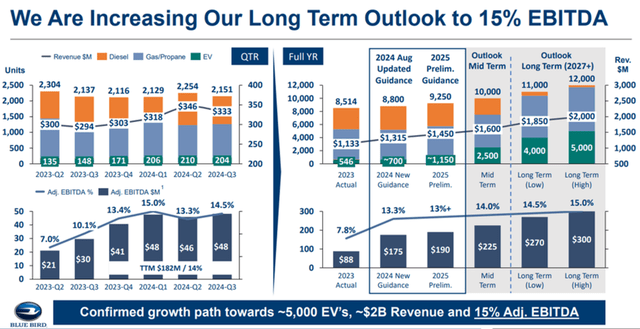

Most importantly, we believe that BLBD’s higher ASPs are also embedded in its order backlog of over 5,200 units (-11.8% QoQ/ inline YoY), as it nears the completion of the first round of the Clean School Bus Program, with orders from the second and third rounds already flowing in.

The management has already commented that the backlog is worth over $775M in revenues, implying average prices of $149.03K, compared to the $93.6K reported in FY2021 and $86.43K in FY2019.

This development is highly promising indeed, since it implies that BLBD’s FY2024 adj EBITDA guidance of 13% (+5.3 points YoY) and long-term margin guidance of 15% are not overly aggressive indeed, compared to the 4.9% reported in FY2021 and 8% in FY2019.

Its profitable growth prospects are significantly aided by the ongoing expansion plans as well, with the management putting in $80M in capex through 2026 (on top of the $80M DOE grant) to support a +40% growth in annual production capacity to 14K units.

The Consensus Forward Estimates

Tikr Terminal

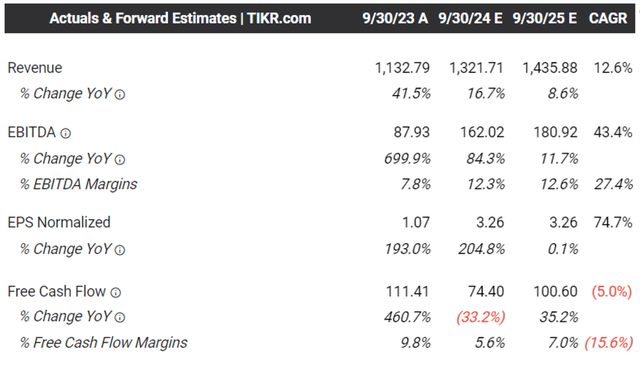

The robust FQ3’24 performance has already triggered the BLBD management’s raised FY2024 guidance, with net revenues of $1.315B at the midpoint (+16.3% YoY), adj EBITDA of $175M (+99% YoY), and adj Free Cash Flow of $85M (-23.6% YoY).

This is up from the original revenue guidance of $1.15B (-2.6% YoY) and adj EBITDA of $85M (-3.2% YoY) offered in the FQ3’23 earnings call, respectively, with the growing backlog naturally lending great insights into its near-term execution.

As a result, it is unsurprising that the consensus have raised their forward estimates, with BLBD expected to generate an accelerated top/ bottom-line growth at a CAGR of +12.6%/ +74.7% through FY2025, as the management raised their “long-term profit outlook towards an Adjusted EBITDA margin of 15% (up +3 points) on ~$2 billion in revenues.”

This is compared to the original consensus estimates of +12.1%/ +44.6% and the historical growth at +2.8%/ -1.3% between FY2016 and FY2023, respectively.

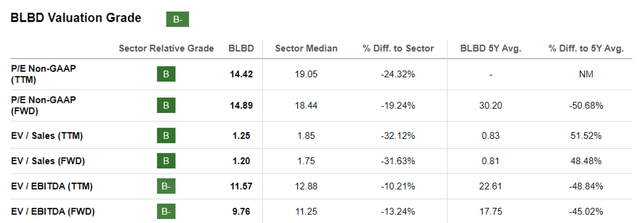

BLBD Valuations

Tikr Terminal

And it is for these reasons that we believe BLBD is cheap at current levels of FWD EV/ EBITDA valuations of 9.76x, compared to the previous article at 11.07x and the June 2024 peak of 12.51x, though elevated compared to its 3Y pre-pandemic mean of 7.85x.

When compared to its direct competitors, such as Thomas Built Bus, a subsidiary of Daimler Trucks North America (OTCPK:DTRUY) at FWD EV/ EBITDA valuations of 8.12x with the projected adj EBITDA growth at a CAGR of +0% and IC Bus, a subsidiary of Traton SE (OTCPK:TRATY) at 5.70x/ -3.4%, it is apparent that BLBD’s double digit growths are still reasonably valued.

This is significantly aided by BLBD’s much lower net debt position of $7.74M (-90.4% YoY) and moderating net-debt-to-EBITDA-ratio of 0.05x, compared to 0.88x in FQ3’23, 7.85x in FY2021, and 1.88x in FY2019.

So, Is BLBD Stock A Buy, Sell, or Hold?

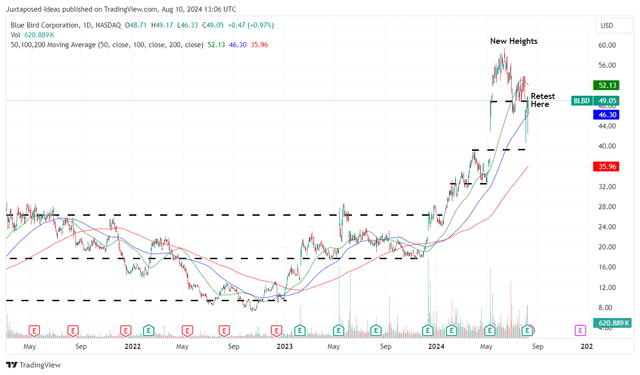

BLBD 3Y Stock Price

Tikr Terminal

For now, BLBD has hit new heights of $59.40 before drastically pulling back to its Q2’24 support levels of $46s and trading nearer to its 100 day moving averages.

For context, we had offered a fair value estimate of $51.80 in our last article, based on the management’s FY2024 adj EBITDA per share guidance of $4.68 and the FWD EV/ EBITDA valuations of 11.07x. This is on top of the long-term price target of $67.20, based on the consensus FY2026 adj EBITDA per share of $6.07, implying that the stock remains cheap at current levels.

Based on the raised guidance to an estimated FY2024 adj EBITDA per share guidance of $5.20 and the discounted FWD EV/ EBITDA valuations of 9.76x, it is apparent that BLBD is still trading below our updated fair value estimates of $50.70.

Based on the management’s new FY2027 adj EBITDA guidance of $285M at the midpoint and the resultant FY2027 adj EBITDA per share of approximately $8.46, we are looking at an excellent long-term price target of $82.50 as well, with it implying a promising upside potential of +69.8% from current levels.

BLBD’s Medium/ Long-Term Targets

BLBD

Therefore, while BLBD may be affected by the ongoing market correction and the uncertainty surrounding the US election, we believe that it may only be temporal, with sentiments likely to lift as it delivers on its medium and long-term targets.

As a result of the still attractive risk/ reward ratio, we continue rating the stock as a Buy.

For now, we recommend interested investors to observe BLBD’s stock movement for a little longer before pulling the trigger. This is because the stock’s short interest continues to grow to 5.98% by the time of writing, up from 4.8% in the start of the year and 2.1% a year ago.

While the bulls have continued to lend strength to its $46s support level during the recent correction, the stock market sentiments remain pessimistic with more volatility likely in the near-term.

Therefore, while we are optimistic about BLBD’s execution and the stock’s prospective capital appreciation, we believe that the market wide pessimism may continue to impact the stock’s near-term performance, prior to the start of the next recovery cycle.

Read the full article here

")

")