")

")

Orion S.A. (NYSE:OEC) recently published their Q2 2024 earnings results on August 1.

In this article, I will provide my rationale on why I believe the 22% panic selloff following the earnings release was exaggerated by shareholders.

I will cover the recent headwinds in their rubber segment, including a surge in tire supply from Southeast Asia, and a decline in cogeneration profitability.

I considered including an outlook section, where I will revise their financial results, and recent insider trading activity, which led me to my Buy rating.

As always, I begin with a brief company overview section for those readers new to this stock.

Company Overview

Orion is a Luxembourg-based company, with headquarters in Spring, Texas, specializing in the manufacturing of carbon black powder.

This powder is used to enhance the physical, electrical, and optical properties of different materials, among them lithium-ion batteries, plastic pipes, tires, and belts.

Their operations are grouped into two segments:

- Rubber segment: this powder is primarily used in tires and mechanical rubber goods, mainly to reinforce them.

- Specialty segment: this segment focuses on a different type of carbon black for specialized applications in polymers, batteries, printing inks, and coatings.

Revenue-wise, their main segment is the rubber carbon black, accounting for 68% of the annual revenue in 2023.

| Year | Segment | Net Sales (Million $) | Adjusted EBITDA (Million $) |

|---|---|---|---|

| 2023 | Rubber Carbon Black | 1,283.3 | 221.6 |

| 2023 | Specialty Carbon Black | 610.6 | 110.7 |

| 2022 | Rubber Carbon Black | 1,355.5 | 168.4 |

| 2022 | Specialty Carbon Black | 675.4 | 143.9 |

Author’s compilation from the latest 10-K.

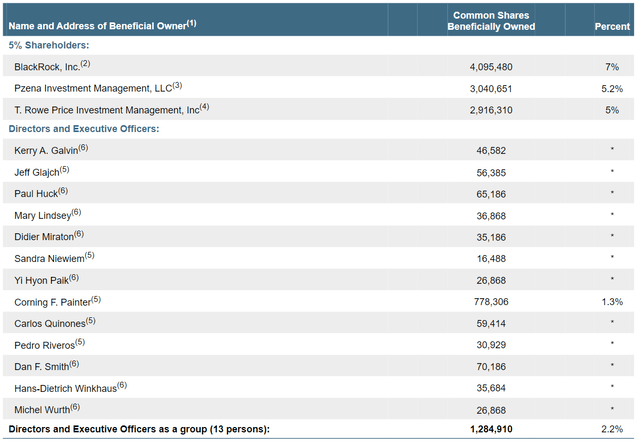

In regards to the ownership of the company, I have to highlight that the total beneficial ownership of all directors and executive officers is only 2.2%.

This is something I generally don’t like seeing in a company, as I like to see management having skin in the game. However, I make an exception to this rule, and that is when insiders purchase a significant amount of shares following a steep decline in the share price. More on this in the outlook section.

I have included below a snippet from their latest 14A.

SEC

As an additional note, Corning Painter, the CEO, has the largest stake among all directors and executive officers. He joined Orion as CEO in September 2018, bringing over 35 years of experience from previous leadership roles.

Recent Performance

I’ll start with the dessert.

Orion’s rubber segment was hit by a decline in volume of 2% YoY, and a decrease in gross profit per metric ton of 8.6% YoY.

I find this concerning, given that one of the drivers for this decline was a sharp increase in tire imports from Southeast Asia into the North American and European markets.

I’m sweating about this because Orion’s customers, especially those in the passenger car tire manufacturing, are losing market share to new, lower-quality competitors.

Since American and European consumers prefer cheaper tires, local tire manufacturers must adjust their production to lower demand. This impacts Orion’s revenue, as they supply black carbon to these manufacturers.

Essentially, Orion’s performance is tied to several layers of external factors that they have no control over.

Another headwind within the rubber segment was related to a decline in the cogeneration profitability due to lower European power prices, and intermittent downtimes at their plant in Louisiana.

As a side note to readers who haven’t heard before about cogeneration, this is a process that involves using by-product gases from black carbon manufacturing to produce energy.

Despite management confirming that their cogeneration plant in Lousiana will extend its downtime well into the third quarter, I am not excessively worried about this issue given that this is an internal disruption that management has the capability of fixing, unlike the surge in Chinese tire imports into Europe and North America.

During the earnings conference call, management attributed the decline in gross revenue to these two issues. While I remain pessimistic about the decline in sale volumes due to the Chinese tire imports in Europe and North America, I am positive about a turnaround in cogeneration by the end of this year. An increase in energy prices in Europe as we approach winter will certainly help, coupled with their planned end in Q3 of the downtime in their Louisiana plant.

Outlook

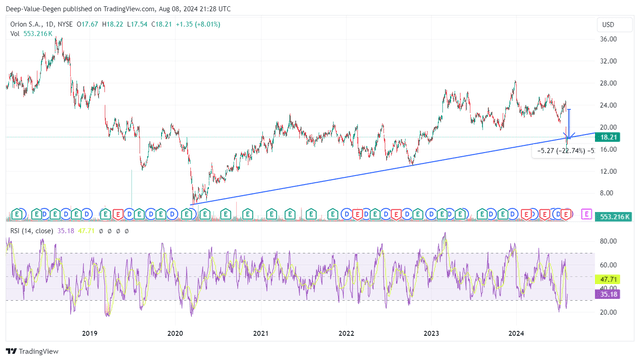

The share price dropped by 22% following their Q2 earnings release.

Trading View

Despite agreeing that their Q2 results were bad, I believe this selloff was exaggerated.

Let’s zoom out and focus on their financials.

Revenue-wise, they reported $477 million in Q2. This is a 4% YoY increase. Additionally, when comparing the revenue over the past 7 quarters, I don’t see a sharp decline in Q2.

Trading View

As I mentioned in the previous section, the volume in their rubber segment declined by 2%, however the volume in the specialty segment increased by 17.4% due to a recovery in the coatings and polymers end markets.

Regarding their net income, I like that they have had a positive net income values since (at least) 2017. Indeed, the trend has been declining since 2021, but not to concerning levels, as seen in the chart below.

Trading View

Their EBITDA has been going up consecutively over the past 4 years, which is something I highly favor. Additionally, their recently revised guidance for adjusted EBITDA ranges between $315 million and $330 million, which I see in line with the previous year.

Trading View

Again, this readjustment in guidance is not enough to justify a 22% selloff overnight.

Debt-wise, their quick and current ratios are 0.8 and 1.4, respectively. Additionally, their debt to assets ratio is 0.44, which I view as a good sign of not being too leveraged on debt.

I do have to admit that their cash flow statement doesn’t look very good. I weigh operating and free cashflows quite highly in my investment style, so seeing a constant decline, especially in operating cash flow, is somewhat concerning to me, especially considering that they have a quarterly dividend in place.

Trading View

The one thing that raised my attention was insider buying activity, by no other than their CFO, following the decline in the share price. Glajch Jeffrey bought a total value of $272,450 in shares, at an average price of $18.16, on August 7.

To put things into context, a week before his purchase, the share price was 26% higher.

Additionally, I am also encouraged about the $94k purchase by Quinones Carlos, SVP of global operations, in June this year. Also, back in June, Glajch Jeffrey bought $118,400 in shares.

So, despite the low (2.7%) beneficial ownership amongst all directors and executive officers, I view these opportunistic insider buying transactions as a positive indication of management’s confidence in the share price, especially following a panic selloff after earnings release.

Conclusion

Despite recent headwinds in the rubber segment, and the 22% selloff following the Q2 earnings release, I view a good potential in a mid-term long position.

In my view, their financial stability remains strong, with a consistent positive net income since 2017, and an upward trend in EBITDA over the past four years. I view their debt level as manageable considering their current ratio, and debt to assets ratio.

Despite the revised lower guidance in adjusted EBITDA, I consider the new guidance to align closely with the previous year’s performance.

Finally, I view the recent insider buying activity, particularly by the CFO, Glajch Jeffrey, and SVP, Quinones Carlos, as a strong indication of their confidence in the share price, especially after the CFO’s $270k purchase after the panic selloff following Q2 earnings release.

While I see some external pressures in the rubber segment, I believe the good performance in the specialty segment will overshadow the challenges.

For these reasons, my rating for this stock is a Buy.

Read the full article here

")

")