The biggest move on the Federal Reserve balance sheet this past banking week was the large decline in the factors absorbing reserves in the commercial banking system.

The General Account of the U.S. Treasury declined by $68.8 billion.

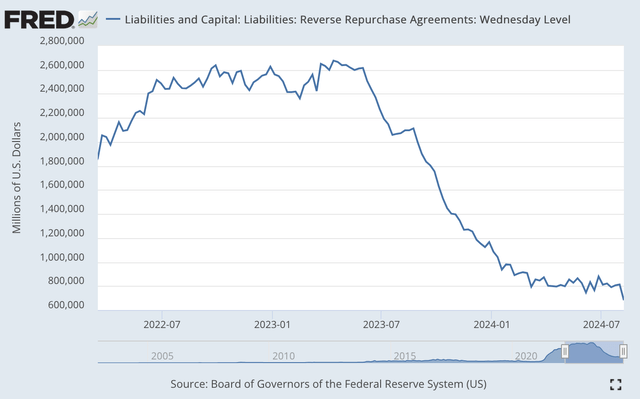

And, the use of Reverse Repurchase Agreements fell by $131.4 billion.

Thus, the release of funds back into the banking system totaled just over $200.0 billion.

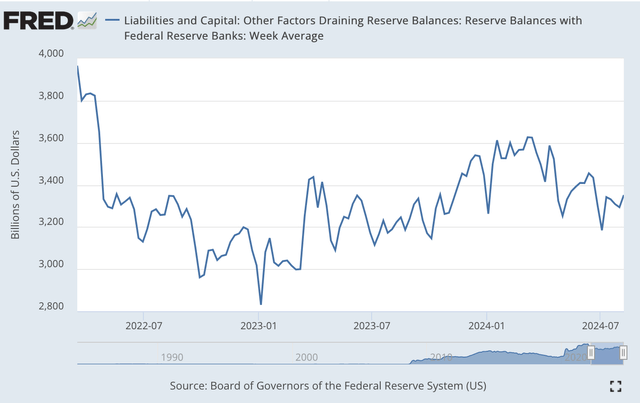

Reserve Balances with Federal Reserve Banks, a proxy for the excess reserves in the commercial banking system, are up by just over $194.0 billion, to just under $3,373.0 billion… or just under $3.373 trillion.

These movements allow us to summarize the whole quantitative tightening program which began on March 16, 2022, in just three numbers.

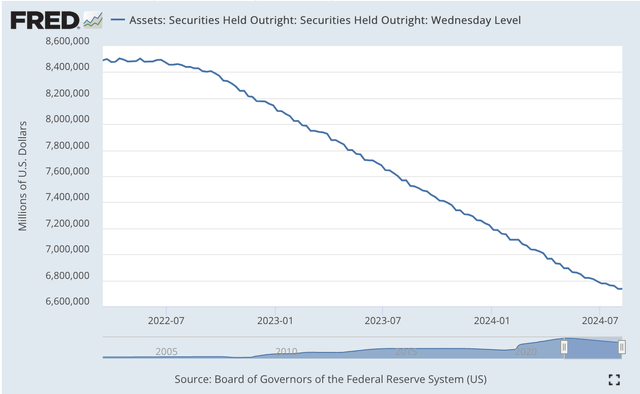

Since March 16, 2022, the securities portfolio of the Federal Reserve has declined by $1,756.3 billion.

The decline in the use of reverse repurchase agreements amounted to $1,182.7 billion.

The difference between these two numbers is $573.6 billion, which matches up very closely with the actual decline in commercial bank reserve balances of $520.5 billion.

That is, the management of the Federal Reserve balance sheet reduces to just two numbers over the 28 months that quantitative tightening has been in place.

The Federal Reserve is not reducing the size of its securities portfolio by as large an amount each month as it did through May of this year. But quantitative tightening is still in place.

This chart shows the results of the quantitative tightening on the securities portfolio of the Federal Reserve

Securities Held Outright (Federal Reserve)

Next, we see how the Reverse Repurchase Agreements of the Fed performed during this time period.

Reverse Repurchase Agreements (Federal Reserve)

And, here is the view of what happened to the Reserve Balances in Commercial Banks… the excess reserves in the banking system.

Reserve Balances With Federal Reserve Banks (Federal Reserve)

So, this is what the Federal Reserve has been doing over the past 28 weeks in terms of managing the reserve position of commercial banks.

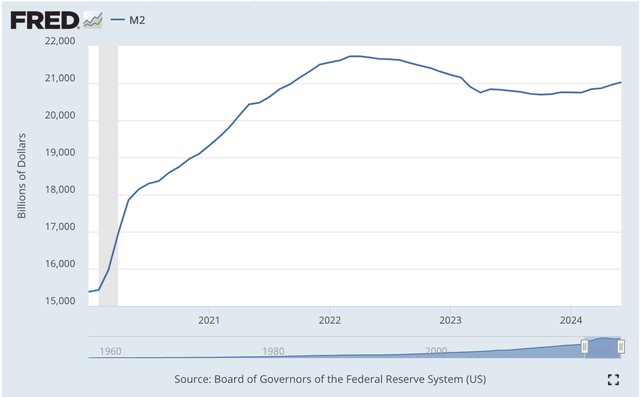

Money Stock

The behavior of the money stock has been getting more and more attention these days.

The immediate concern that is being expressed is that the growth of the M2 money stock has been pretty tepid in recent months.

The worry is that if the M2 money stock is not growing, the economy will head into a recession.

Let’s look…

M2 Money Stock (Federal Reserve)

One can see from this chart that the M2 money stock began to decline around the same time that the Federal Reserve began to impose its program of quantitative tightening.

So, the analysts are focusing on the past 28 months or so is expressing their concern with the slowdown of monetary growth.

To fully comprehend the current situation, I believe that it is necessary to return to an earlier time to get the full picture of where monetary policy is relative to the economy.

The Federal Reserve’s effort to fight the effects of the Covid-19 pandemic and the following recession resulted in a massive increase in reserves into the banking system.

This massive increase in reserves into the banking system resulted in a massive increase in the M2 money stock that immediately followed the injection of reserves.

However, this influx of money into the banking system did not fully spill over into the economy.

Why?

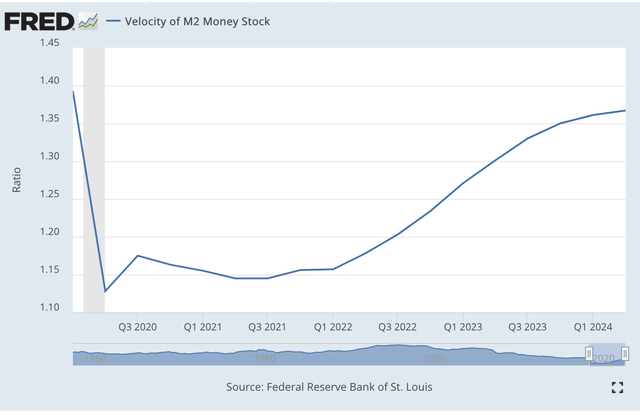

Well, the spending velocity of the monetary injection did not take place right away.

The velocity of circulation of the M2 money stock dropped and, although it has increased substantially since that time, it has not fully recovered to earlier levels.

In other words, a lot of the money injected into the banking system did not flow into the spending streams of the economy.

Velocity of M2 Money Stock (Federal Reserve)

This is one of the reasons that can be given for the continued growth in the economy that has surprised almost everybody.

The money was in the banking system… the Federal Reserve had put it there during the “pandemic” and its following recession, but the funds were not fully used at the rate the economy experienced before the problems hit.

If one looks at the money stock figures over a longer period of time, one can contend that the compound rate of increase in the money stock extending into the current period was more in the 7%-8% range for the full-time period going back to 2020.

Thus, the banking system has lots and lots of reserves, injected during the period the Fed was “saving” the economy… and, for the most part, these reserves remain in the banking system at the present time.

The reduction in the Fed’s portfolio of securities has only removed a relatively small of amount of the reserves pumped into the banking system to “save” it.

In fact, the economic system can still have enough liquidity to carry its expansion on for several more years.

Should The Fed Lower Its Policy Rate?

I am not on the side of the debate that favors the Fed lowering its policy rate of interest.

I don’t see problems right now relating to interest rates being too high.

The banking system has plenty of reserves on its balance sheets.

The business world has lots of money on its balance sheets.

Economic growth, although modest, can continue on.

The Federal Reserve needs to take its time.

The Federal Reserve needs to see banking reserves return to a more “prudent” level.

The Federal Reserve needs to see the financial system adjust to a more modest rate of operation.

The United States has experienced quite a few years of massive upheaval.

It’s time to return to a period of more stable financial markets, so the attention can be focused on innovation and technological advancements. The world is going through an incredible transition and needs to keep its full attention on building the future and not on the instability and volatility of financial markets.

I believe that the leaders of the Federal Reserve are trying to help us achieve this “new” world, and we should let them have their space to steadily let the system work.

Read the full article here

")

")