")

(DKNG)")

")

")

Some time ago, back in the middle of October 2023, I wrote an article that took a bullish stance on US Foods Holding Corp. (NYSE:USFD). The company, for those who are not familiar with it, serves as a massive food distributor. The firm has a long history, dating back more than 150 years. And since its founding, it has grown to generate tens of billions of dollars a year in revenue and to have a market capitalization of $12.56 billion.

In my bullish article about the business, I acknowledged that the stock had seen some weakness leading up to that point. This was in spite of strong revenue growth and improved profitability. And based on my own assessment of the firm, I expected that trend to continue. So far, the ‘buy’ rating I assigned it back then has paid off well. The stock is up and impressive 36.6% at a time when the S&P 500 is up 24.3%. Given this outperformance, you might think that I would finally be ready to downgrade the company to something more modest. But based on current expectations provided by management, and how shares are priced on a forward basis, I would argue that some additional upside is probably on the table. Because of this, and in spite of the fact that shares look to be more or less fairly valued compared to comparable firms, I’m keeping the company rated a ‘buy’ for now.

Recent results are encouraging

To be honest with you, I am quite surprised by the fact that shares of US Foods Holding Corp rose by only 0.4% on August 8th. This is because, before the market opened on that day, management announced financial results covering the second quarter of the company’s 2024 fiscal year. Revenue and earnings came in higher than anticipated, while adjusted earnings fell in line with what analysts expected. Guidance provided by management looks promising and shares are attractively priced.

Author – SEC EDGAR Data

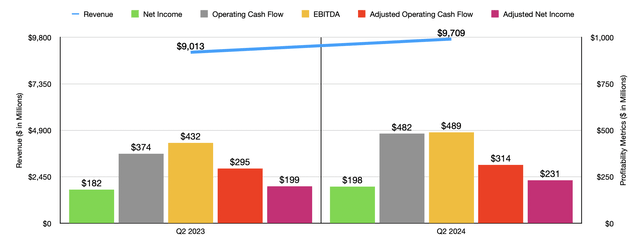

On the revenue side of things, we get a reading of $9.71 billion for the quarter. This represents an increase of 7.7% compared to the $9 billion the company reported one year earlier. The revenue reported by management also happens to be $120 million greater than what analysts expected. This upside was driven mostly by a 5.2% rise in total case volume, and a 5.7% increase in independent restaurant case volume. Management said that organic case volume growth of 1.9%, with organic independent restaurant case volume growth of 3.2%, played a role in this upside. However, the company also benefited to the tune of 2.9% from the combination of acquisitions and food cost inflation. Clearly, with a growing population, the food economy is certain to see stronger demand from one year to the next.

On the bottom line, the picture also looked better year over year. Earnings per share came in at $0.80. That is slightly above the $0.73 per share reported for the second quarter of 2023. It also happens to be $0.10 greater than what analysts anticipated. This reading translated to a rise in net profits from $182 million to $198 million. Management also reports adjusted net income. But I am not a fan of this metric when management includes certain expenses like depreciation and amortization. That is because we are getting closer to a proxy for operating cash flow as opposed to earnings. But I digress. During the quarter, adjusted earnings per share came in at $0.93. That’s up from the $0.79 per share reported one year earlier, and it happens to be in line with what analysts expected.

The adjusted earnings per share reported by management translated to a rise in adjusted net income from $199 million to $231 million. But these aren’t the only profitability metrics that matter. During the quarter, operating cash flow is $482 million. That’s a nice increase over the $374 million reported one year earlier. If we adjust for changes in working capital, we get a more modest rise from $295 million to $314 million. And lastly, EBITDA for the company popped up from $432 million to $489 million.

Author – SEC EDGAR Data

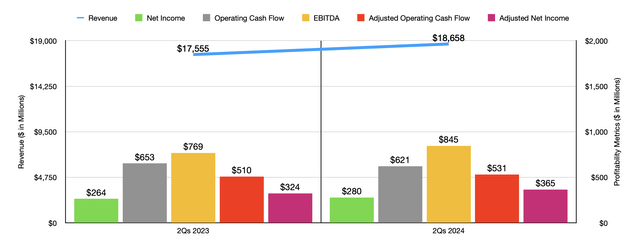

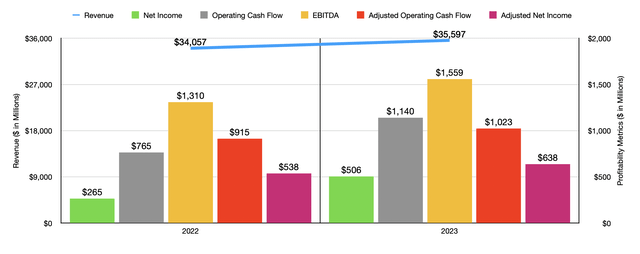

Beyond any doubt, the second quarter of the 2024 fiscal year was a good time for shareholders. But this is only part of a longer and more impressive trend that the company has been on. In the chart above, you can see financial results for the first half of this year relative to the same time last year. This shows consistent revenue, earnings, and cash flow growth. The one exception is with operating cash flow. But on an adjusted basis, we do get a year-over-year improvement. In the chart below, meanwhile, we can also see results for 2022 relative to 2023. And without exception here, revenue, earnings, and cash flows, have all increased nicely. Consistent growth more or less across the board is always a great thing for investors to see. And that is because this reduces risk and serves as a testament to the quality of the operation in general.

Author – SEC EDGAR Data

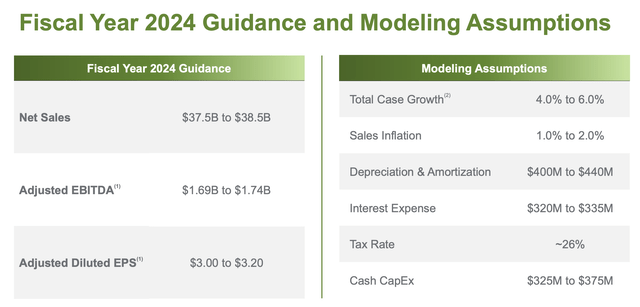

If all goes according to plan, growth for the company will continue this year and in the years to come. For this year, management is forecasting revenue of between $37.5 billion and $38.5 billion. At the midpoint, this would be 6.8% above what the company saw in 2023.

US Foods Holding Corp

They also expect adjusted earnings per share of between $3 and $3.20. At the midpoint, this implies adjusted net income of $769.8 million. If GAAP income scales up at the same rate, then this would translate to net profits of about $592 million. Management is also forecasting EBITDA of between $1.69 billion and $1.74 billion. At the midpoint, this would be $1.715 billion. And that should translate to adjusted operating cash flow of around $1.125 billion.

Author – SEC EDGAR Data

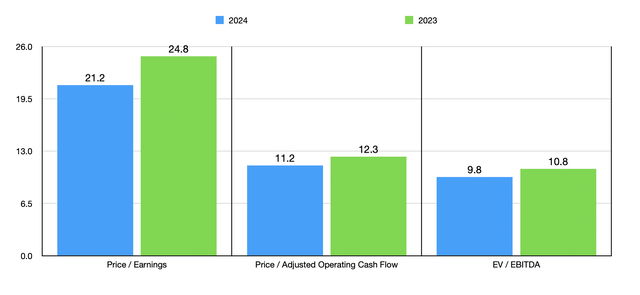

With these figures, as well as historical results from 2023, you can see in the chart above how the stock is valued. Relative to earnings, I would definitely agree that the stock is a bit lofty. But when it comes to the other two profitability metrics, especially considering the quality of the operation we are dealing with, I would say that shares are mildly attractively priced. When it comes to comparable firms, I looked at five such businesses in the table below. On a price to earnings basis, two of the five ended up being cheaper than US Foods Holding Corp. The same held true on an EV to EBITDA basis, though in that case, one other company was tied with it. And lastly, on a price to operating cash flow basis, four of the five firms ended up being cheaper than our target.

| Company | Price / Earnings | Price / Operating Cash Flow | EV / EBITDA |

| US Foods Holding Corp. | 21.2 | 11.2 | 9.8 |

| Performance Food Group (PFGC) | 24.3 | 9.0 | 9.8 |

| United Natural Foods (UNFI) | 40.6 | 2.8 | 11.5 |

| The Chefs’ Warehouse (CHEF) | 37.4 | 16.3 | 12.3 |

| The Andersons (ANDE) | 16.2 | 2.1 | 5.3 |

| SpartanNash Company (SPTN) | 12.6 | 5.2 | 5.9 |

If everything goes according to management’s plans, growth will continue beyond just this year as well. The company is forecasting annualized revenue growth of about 5% for the foreseeable future, with a timeframe on that extending from 2025 through 2027. With management’s efforts on keeping costs under control, they expect this to bring with it EBITDA expansion of about 10% per annum, and for adjusted earnings per share to grow at around 20% per annum. Of course, this won’t be cheap. After all, organic growth can only take you so far in such a mature industry. It is highly probable that management will also rely on acquisitions. In fact, in order to achieve its targets, it hopes to allocate around $4 billion toward growth initiatives between 2025 and 2027. But management is not waiting for 2025 to roll around in order for this to occur. In the second quarter of this year, the company acquired IWC Food Service, a broadline distributor focused on serving the Nashville, Tennessee area. That particular purchase cost investors $220 million.

US Foods Holding Corp

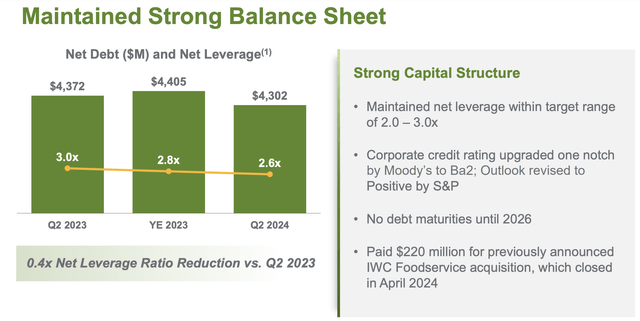

Of course, we always need to be wary of the company overextending itself by growing too rapidly. The good news has been that net leverage has actually dropped over the past year. Back in the second quarter of 2023, the firm’s net leverage ratio was 3. But today, that number is 2.6. Management’s goal is to keep it within the 2-3 range. At the same time, the company is also being active in buying back stock. On June 1 of this year, for instance, the company authorized a new share repurchase program of up to $1 billion. In June alone, the company repurchased $21 million worth of shares. And for the third quarter of the year ending on August 7th, it purchased another $61 million worth of stock.

Takeaway

Based on all the data provided, I must say that US Foods Holding Corp. looks to be a fairly tasty opportunity. Management is growing the company while buying back stock and reducing leverage. The overall financial track record of the company is impressive, and shares are attractively priced on an absolute basis. They do look closer to being fairly valued relative to comparable firms. But that’s not enough to stop me from rating the business a soft ‘buy’ at this time.

Read the full article here

")

(DKNG)")

")