")

")

")

")

")

Entergy Corporation (NYSE:ETR) is a regulated electric utility that primarily operates in the U.S. states of Texas, Louisiana, Arkansas, and Mississippi:

Entergy Corporation

Texas, in particular, has been making headlines quite a lot lately due to several companies relocating to the state from elsewhere. For example, we recently saw Chevron (CVX) announce that it will be moving its headquarters to Texas from California. SpaceX recently made a similar announcement. The movement of industry to the state has been attracting people to the region, who naturally want to move to where jobs are. These two trends are acting as tailwinds for Entergy’s profitability. After all, the new businesses and residents need electricity, and this has been increasing the load on Entergy’s network. All else being equal, this results in rising revenues and profits. I explained this in my last article on Entergy, which was published in the middle of September.

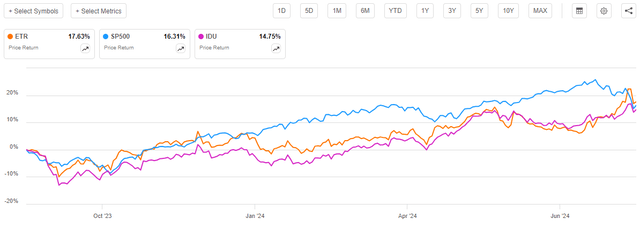

The utility sector has generally performed fairly well ever since the current bull market began in November 2023. This is a very nice change from the disappointing performance that most stocks in the sector delivered during the summer of that year. As such, we might expect Entergy Corporation’s stock price to have delivered a very acceptable performance since the date of our previous discussion.

This assumption proves to be correct, as shares of Entergy Corporation have risen by 17.63% since my previous article on this company was published. This is much better than the 14.75% gain of the U.S. Utilities Index (IDU). Perhaps surprisingly, the company’s share price has also outperformed the S&P 500 Index (SP500):

Seeking Alpha

It is very surprising to see a utility company’s share price outperform the S&P 500 Index, as that rarely happens. After all, utilities like Entergy do not deliver particularly rapid earnings growth, and so they do not usually experience the same level of gains in a bull market as most high-growth companies. High-growth technology companies have increasingly accounted for a growing proportion of the S&P 500 Index over the years, so the performance of the market is generally dictated by those companies’ stocks. In any case, every investor is almost certain to be pleased with the company’s recent performance.

One characteristic of utility companies is that they tend to deliver a significant proportion of their returns through the dividends that they pay out. Dividends represent a very real return that is not reflected in the share price performance of an investment. When we include the dividends that the company (as well as the indices) paid out, we get this alternative chart:

Seeking Alpha

This makes Entergy’s performance look even better relative to the S&P 500 Index. Indeed, the inclusion of the dividends and index distributions makes the S&P 500 Index’s performance look rather disappointing, as both Entergy and the utilities sector outperformed the broader market over the period by quite a bit. While this is not usually the case, it does stand as potential support for the belief that investors should not exclude any sector from their portfolio.

My previous article on Entergy Corporation was published on Seeking Alpha in the middle of September 2023, so roughly eleven months have passed. Naturally, this means that a great many things could have changed that may affect our thesis. In this article, we will revisit the company and our original thesis and make updates as appropriate.

About Entergy Corporation And Thesis Update

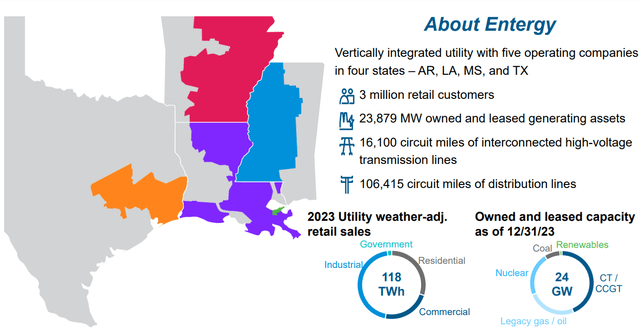

As mentioned in the introduction, Entergy Corporation is a large regulated electric utility that serves the states of Mississippi, Texas, Louisiana, and Arkansas. The company is generally considered to be one of the largest utilities in the United States, as it serves approximately three million customers and has a market capitalization of $24.84 billion. However, enterprise value is generally considered to be a better measure of a company’s size, so Entergy Corporation has an enterprise value of $52.57 billion today.

The states in which the company operates are something of a mixture in terms of culture. Mississippi and Arkansas are both generally considered to be very rural states, as neither one of them has any particularly large cities. We can see this here:

|

State |

Largest City |

Population |

|

Mississippi |

Jackson |

153,701 |

|

Arkansas |

Little Rock |

203,842 |

As such, the residents and businesses that the company serves in both of these states are pretty spread out, and so it can cover a very large geographic area without having a large number of customers. The same is true of much of Louisiana, as its largest city of New Orleans (Population: 383,997) is not especially large. However, Louisiana does have a number of medium-sized cities in close proximity to one another and Entergy serves nearly the entire state, so the company has a fairly large customer base there. In fact, Louisiana is home to the largest proportion of the company’s customers:

|

State |

Entergy Customers |

|

Arkansas |

730,000 |

|

Louisiana* |

1,313,000 |

|

Mississippi |

459,000 |

|

Texas |

512,000 |

* Total includes both New Orleans and elsewhere. Only electric customers were counted, under the assumption that anyone who receives natural gas service also receives electric service.

However, despite Louisiana and Arkansas being Entergy’s largest operating states in terms of the number of customers served, Entergy typically emphasizes Louisiana and Texas in its analyst presentations and earnings press releases. One reason for this is that Texas is one of the fastest-growing states in the nation, and as such, is a driver of earnings growth for Entergy. According to World Population Review, which pulls data from official sources such as the U.S. Census Bureau, the population of Texas is currently growing at a 1.55% annual rate. This is the third-fastest growth rate in the country (after South Carolina and Florida), so we can see how the company’s customer base in the state is growing. As I stated in my previous article on Entergy:

The reason that this is important for Entergy is that population growth is one of the only ways that a utility can grow, and it is completely out of the utility’s control. This is because Entergy is a monopoly that is restricted to operating in a specific region by law and it cannot expand by convincing customers outside of its service territory to switch providers. The fact, then, that Texas is one of the fastest-growing states in terms of population provides a tailwind to the company’s growth.

Texas is frequently thought of as having an oil-focused economy. After all, the hydrocarbon production growth in the Permian Basin has been one of the biggest news stories since the middle of the last decade. I certainly contributed to this surge of information on this area, as regular readers are no doubt well aware. However, Texas has also been growing as a hub for the technology sector. A few years ago, TechCrunch stated that Austin, Texas is becoming a popular place for technology start-ups:

Austin made headlines in 2021 for being “the place” for startup founders and venture capitalists alike to set up shop.

As Austin’s skyline expands, the city continues to solidify its standing as a tech hub. And the numbers are there to back it up.

VCs invested over $5.5 billion across 412 deals in 2021, more than double the amount of capital invested in 2020, according to PitchBook data. Rounds are getting larger, too, signaling a further maturing across the market: All of the top 10 deals for Austin in 2021 amounted to $100 million or more.

A local newspaper in Austin, Texas also discussed the growth in the city’s technology sector in an article from earlier this year.

The takeaway here is that Austin, Texas is starting to have some of the same panache as cities such as Palo Alto, California, that have long attracted technology talent.

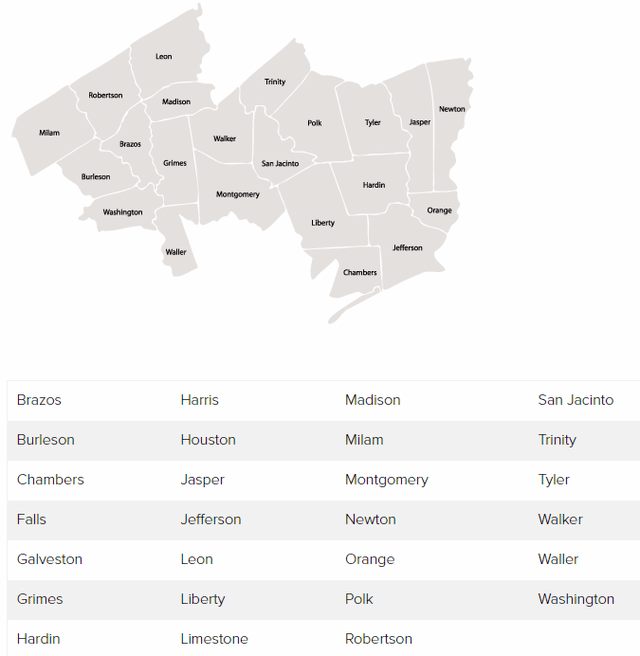

Entergy Corporation does not directly serve Austin. The company’s operations in the state are primarily centered around 27 counties in the Houston-Galveston region:

Entergy Corporation

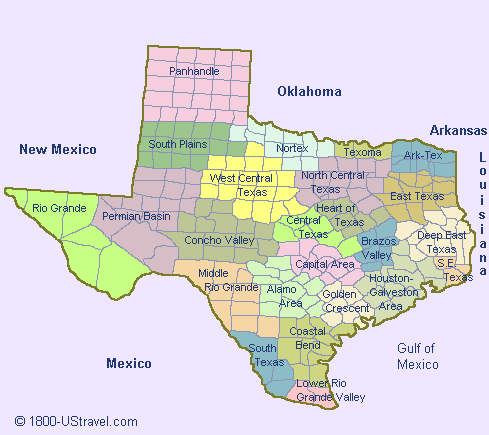

However, parts of this service territory are fairly close to the Austin metropolitan region:

TravelNotes.org

Austin is in the “Capital Area” shown in the map above. Entergy’s operations are mostly in the areas labeled as “Houston-Galveston Area” and “Brazos Valley” in the map above. Thus, we can see that the company might still benefit from the expansion of Austin’s technology sector as it expands outward into Entergy’s service territory. In addition, Entergy Corporation already serves Houston, which has been seeing substantial industrial expansion due to the oil production growth in the Permian Basin.

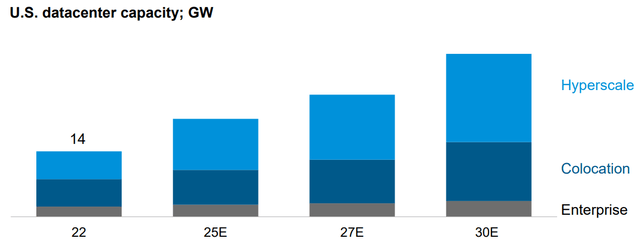

Entergy noted the technology sector expansion as a potential growth driver in its June 2024 analyst presentation. The company included a slide showing demand forecast for U.S. data centers:

Entergy Corporation/Data from Boston Consulting Group

This slide is not particularly descriptive, but it does show that the power consumption of American data centers is expected to grow at a very rapid pace over the remainder of this decade. The slide appears to refer to a study by the Boston Consulting Group that shows that the United States will face a shortfall of 80 gigawatts of electricity by 2030 due to the growing demands for power by technology companies constructing data centers. From the study:

The commercialization of artificial intelligence and associated data center expansion is bringing rapid growth to previously flat U.S. power markets. The Boston Consulting Group projects that total data center power demand will increase by 15-20% annually to reach 100-130 gigawatts by 2030. That’s the equivalent of the electricity used by about 100 million U.S. houses – about two-thirds of the total homes in the U.S.

The U.S. may face a shortfall of up to 80 gigawatts of firm power to meet this demand by 2030, though gaps will vary in size across regional markets.

Texas is on the list of states with the largest number of data centers and power consumption of data centers. Thus, the argument here is that there may be further data center construction in Texas to support the deployment of generative artificial intelligence due to the simple fact that the high level of data centers already in the state and the increasing number of technology workers means that some of the needed infrastructure to support more data centers already exists. After all, there are already workers in the region that know how to construct and maintain data center hardware. It is certainly more logical for technology companies to construct more data centers here than put them in an area like Nebraska that does not have the required employees already.

If it is true that more data centers will be constructed in Texas over the coming years, then it is quite possible that some of the electricity produced and distributed by Entergy will be needed to power the hardware in these data centers. The company’s revenues directly correlate to the amount of electricity that its customers consume. After all, electric bills increase when a household or business consumes greater amounts of electricity. The higher revenues coming into the company should allow more money to flow down to the bottom-line profits.

Financial Update

Entergy has already benefited from growing electric consumption in its service territory, as our thesis suggests should be the case. Here are the company’s reported revenues for each of the past eleven quarters:

Seeking Alpha

(all figures in millions of U.S. dollars)

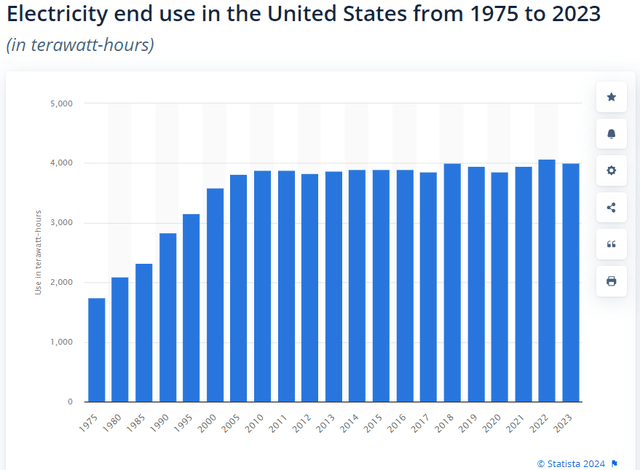

We do see some seasonal fluctuations here, which are mostly driven by air conditioner usage. Most of the states in which Entergy Corporation operates are very hot during the summer, so its customers run air conditioners in an attempt to cool down. Thus, we should expect the company’s revenues to spike in the second and third quarters of the year because that is when air conditioning use will peak. We do certainly see that here, and we also see that the company’s revenues in a given quarter were usually higher than they were in the same quarter of the previous year. For example, in the recently reported second quarter of 2024, Entergy had a total revenue of $2.9536 billion compared to $2.846 billion in the second quarter of 2023. This is a 3.78% increase year-over-year. That certainly seems small, but it is not really ridiculously low for an electric utility, as these companies grow at a very low rate and electric consumption in the United States has been fairly flat over the past several years. This chart shows the total amount of electricity consumed annually in the United States since 1975:

Statista

As we can see, electric consumption in the United States has been relatively stable since 2010. This might seem to disprove our growth thesis that was described earlier, but it is important to keep in mind that this chart shows the numbers for the country as a whole. There can still be an area in which electricity consumption increases that is offset by a decrease elsewhere. Overall, this fits with the Boston Consulting Group’s statement that the demand for electricity has been stagnant.

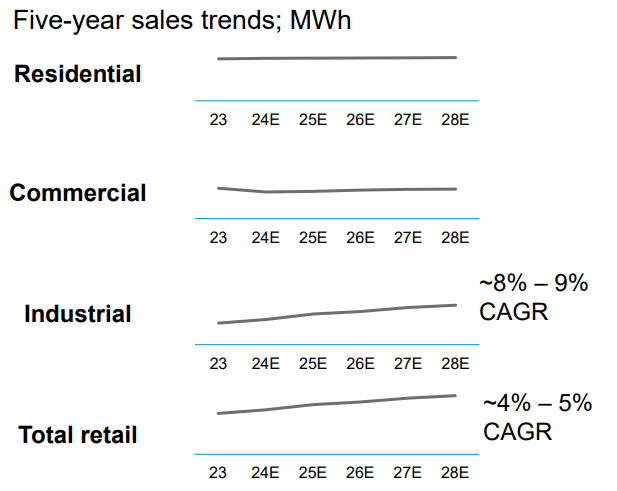

Entergy Corporation recognizes this as well. Its own projections call for flat consumption from its residential customers through 2028, although industrial use is expected to increase dramatically over that period:

Entergy Corporation

This fits with our statements earlier in this article and in previous ones. Ultimately, it will be the case that growing consumption by industrial companies (data centers are considered industrial users) will drive the company’s load growth over the next five years or so. We can see too that this growth rate should be fairly substantial, with industrial consumption growth rising at an 8% to 9% compound annual growth rate through 2028.

As we discussed in the previous article, Entergy is working on upgrading its infrastructure to accommodate this projected growth. This will grow the company’s rate base over the period. I explained the concept of rate base previously:

The rate base is the value of the company’s assets upon which regulators allow the company to earn a specified rate of return. As this rate of return is a percentage, any increase in the rate base allows Entergy to adjust the prices that it charges its customers in order to earn more money.

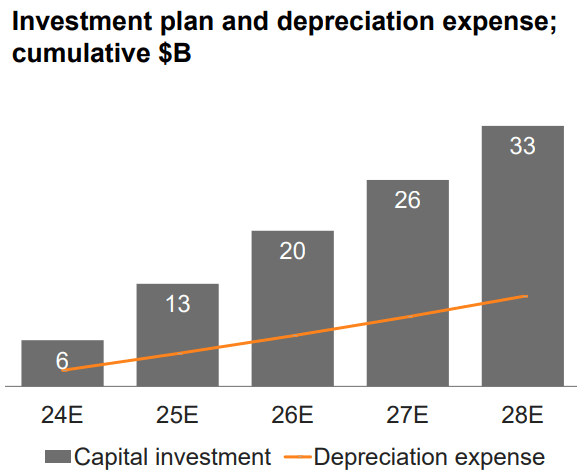

The usual way in which a utility company increases its rate base is by spending money to upgrade its infrastructure. Entergy Corporation is planning to do that as it recently unveiled a plan to invest approximately $33 billion over the 2024 to 2028 period into its distribution network:

Entergy Corporation

This is a substantial increase over the $16 billion that the company was planning to invest the last time that we discussed it. The massive increase in the company’s planned capital expenditure cannot be explained simply by inflation. It seems obvious that the growth in industrial consumption within its service territory is driving the company’s management to realize that it needs a much more robust and capable infrastructure than was originally expected. This provides further validation that the thesis that we have been promoting for Entergy Corporation is correct.

The company’s new capital spending plan should be sufficient to drive its earnings per share upwards at a 6% to 8% compound annual growth rate over the 2024 to 2028 period. When combined with the current 3.89% dividend yield, we are looking at a 10% to 12% total return over the period, assuming that the company’s price-to-earnings ratio remains relatively stable. That is a very reasonable total return for a utility company.

Financial Considerations

As I stated in my previous article on Entergy Corporation:

It is always important that we investigate the way that a company is financing its operations before we make an investment in it. This is because debt is a riskier way to finance a company than equity because debt must be repaid at maturity. That is typically accomplished by issuing new debt and using the proceeds to repay the existing debt since very few companies have sufficient cash on hand to completely pay off their debt as it matures. As new debt is issued with an interest rate that corresponds to the market rate at the time of issuance, this can cause a company’s interest expenses to go up following the rollover.

The usual way that we analyze a utility company’s financial structure is by looking at its net debt-to-equity ratio. As of June 30, 2024, Entergy Corporation had a net debt of $27.3954 billion compared to $14.9011 billion in shareholders’ equity. This gives the company a net debt-to-equity ratio of 1.84 today. This is an improvement over the 1.92 ratio that the company had the last time that we discussed it, which is very nice to see. After all, the reduction in this ratio means that the company is less dependent on debt to finance itself than it was eleven months ago, which risk-averse investors should appreciate in today’s high-interest rate environment.

However, as I have pointed out in a few previous articles, Entergy Corporation is somewhat more leveraged than its peers. This is still the case today, which we can clearly see here:

|

Company |

Net Debt-to-Equity Ratio |

|

Entergy Corporation |

1.84 |

|

DTE Energy (DTE) |

1.99 |

|

Eversource Energy (ES) |

1.93 |

|

CMS Energy (CMS) |

1.76 |

|

Exelon Corporation (EXC) |

1.73 |

(all figures are calculated from the most recently released financial report for each company)

We can immediately see that Entergy Corporation is the median company in terms of leverage here. This is a bit different from the scenario that we have seen in the past, which generally showed Entergy Corporation being much more leveraged than its peers. It is worth noting that DTE Energy and especially Eversource Energy have been rapidly increasing their leverage, though, so that is at least partially responsible for the improvement that we see in the chart above.

While the improvement here is certainly a very good thing, we can still see that Entergy Corporation’s leverage remains fairly high, and it is still substantially more levered than either CMS Energy or Exelon Corporation. As such, we should certainly not celebrate the improvement here. Rather, we should continue to watch the company’s leverage in order to ensure that it remains on its current course of strengthening its balance sheet.

Valuation

According to Zacks Investment Research, Entergy Corporation will grow its earnings per share at a 7.33% rate over the next three to five years. This gives the company a price-to-earnings growth ratio of 2.20 at the current stock price.

Here is how Entergy’s current valuation compares with its peers:

|

Company |

PEG Ratio |

|

Entergy Corporation |

2.20 |

|

DTE Energy |

2.19 |

|

Eversource Energy |

2.51 |

|

CMS Energy |

2.58 |

|

Exelon Corporation |

2.73 |

(all figures from Zacks Investment Research)

This looks pretty good for Entergy Corporation. As we can clearly see, the company’s current price-to-earnings growth ratio is fairly low compared to most of its peers. Thus, the current entry price appears to be pretty reasonable.

Conclusion

In conclusion, Entergy Corporation is fairly well-positioned to grow going forward. The company has a significant presence in Texas, which is one of the most rapidly growing states in the country. This applies to both the population and businesses, and it is the latter that will likely be the driver of forward electric consumption growth. The state may also be home to data centers supporting artificial intelligence and other high-consumption activities due to its high-tech base in a few nearby cities. That will obviously help Entergy Corporation, and the company is making the investments necessary to grow its infrastructure in support of this thesis. Entergy Corporation has also been strengthening its balance sheet and trades at a fairly attractive discount to its peers.

Read the full article here

")

")

")

")