")

")

")

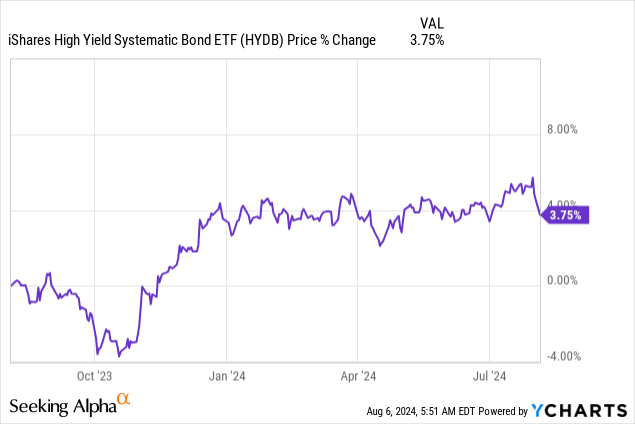

The iShares High Yield Systematic Bond ETF (BATS:HYDB) is an active strategy that pursues fixed income investments in junkier markets. We’ve long been critical of the recent high levels of demand for poor credit that has driven credit spreads to historical lows despite what we believe to be an untenable economic situation. Therefore, we have eschewed entirely and consistently any fixed income with credit premiums in the US, which we asserted was an exuberant credit market. We also have been careful, although with less conviction, about duration. On the jobs data announcement and onset of a risk-off attitudes, possibly exacerbated by the days of deleveraging we’ve had in markets, yields have gone down, which would have been good for risk-free ETFs, but credit spreads rose. With the sheer quantum of debt in corporate America, and the fact that risk-free yield would only decline if there was concern enough about the economy for credit risks to rise, we don’t see much point to high-yield credit in the current environment.

HYDB Breakdown

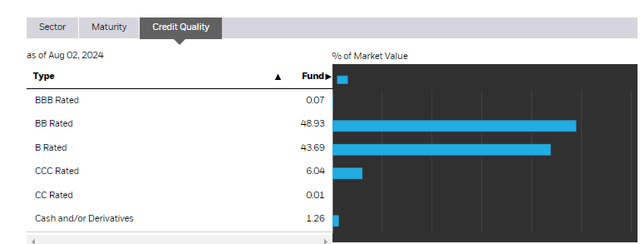

Firstly, looking at the ETF as it is today, we need to know the two key data points which are the effective duration, at 3.47 years, and the credit ratings of the portfolio which are the following.

Credit Ratings (iShares.com)

Most are BB or B rated, so below investment grade rating.

The last couple of days have been difficult for the markets. The appreciation of the Yen set the conditions for a major decline in stock markets, when some wayward US economic data and a couple of earnings misses caused some deleveraging and margin calls.

The US data has been the most relevant for fixed income. Jobs figures came out and they looked concerning. The rise in unemployment was enough to trigger Sahm’s Law, which is a technical indicator that is supposed to predict recessions. This has caused credit spreads to come from close to historical lows and rise rapidly to match early 2024 levels – from around 1.7% to 2.35% over the last few days for BB rated instruments.

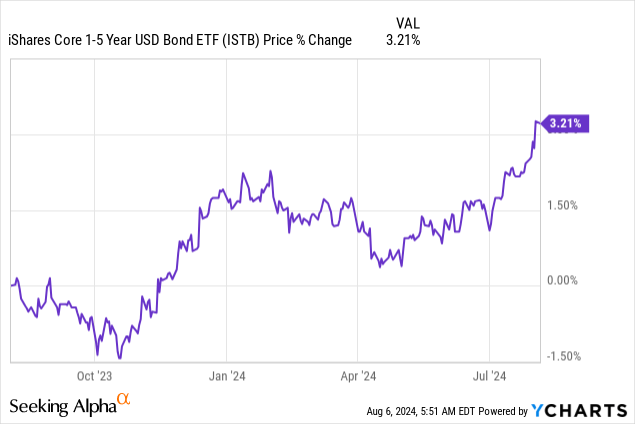

That considerable rise in credit spreads offsets the benefit from lower prevailing rates. Prevailing rates for 3-year yields fell around 0.5%, which is less than the rise in credit spreads. 5-year yields fell by around 0.3%. This caused a decline in the performance of HYBD.

This performance therefore lags risk-free instruments of late, and on a risk-adjusted basis for the last year the return of higher risk HYDB would also be lagging.

Bottom Line

Honing on the jobs data, there were pretty soft jobs addition figures. The unemployment rate also shot up to 4.3%. This was alarming at first, and technically Sahm’s Rule has been triggered, which is supposed to be a leading indicator for oncoming recessions. While this is indeed concerning, it’s useful to take into account that some of the unemployment might be exacerbated by seasonal effects around work and weather, where hurricanes and heat might have reduced demand for temporary workers. More permanent jobs were stable. It’s possible that there isn’t as much to worry about, and therefore that credit spreads might again fall, even though we are unsure why they were at those historically low levels in the first place. We think a premium from historical lows makes sense, considering that aspects of the economic environment are not tenable. Inflation is above policy levels in the world’s largest economy, after all.

On the other hand, while lower prevailing rates were a positive for this ETF, we question whether the 3.47 year duration, or any duration at all, makes sense yet. While by an older Phillips Curve logic, inflation should be lower at higher levels of unemployment, that thinking has become antiquated, and it’s more the changes in employment that matter. In this case, there was a meaningful headline rise in unemployment. With inflation expectations also firmly anchored at above policy levels, we’d probably need an unemployment-instigated recession to get inflation down. If unemployment figures end up being a blip, then there is a fair chance that the prevailing rates come up, and the hawks on the FOMC push out rate cutting timelines further as they wait for clear data on CPI pointing downwards.

In other words, HYDB and other higher-yield ETFs fail to take advantage of the situation. While at least risk-free fixed income ETFs can benefit on rate cuts and rate cut speculation, which is going to be correlated with more dialogue around recession risk since we see no other way for inflation to fall, high-yield ETFs will at best run flat since the credit and risk-free yields will likely be negatively correlated. In the case of a recession, with the sheer quantum of debt in corporate America coming due in the next year or so, it is more likely that credit spreads come to the fore and drive down prices in high yield, even if prevailing risk-free rates fall. We don’t see any major case for high-yield ETFs.

Read the full article here

")

")

")