(NASDAQ:AAPL)")

Apple (NASDAQ:AAPL) submitted a solid earnings sheet for the third fiscal quarter, that resulted, despite weak growth in the company’s largest hardware category iPhones, in a sizable top line and bottom line beat. Services revenues also reached a new all-time high, indicating that the company’s transition away from hardware-related revenues is continuing. Additionally, Warren Buffett, a major investor in Apple, drastically cut back its investment in the iPhone maker in the second-quarter, creating selling pressure for the technology company. Since shares have reached my fair value estimate and I expect sentiment headwinds related to Buffett’s stock sales, I believe the risk profile has deteriorated here.

Previous rating

I rated shares of Apple a strong buy in early May, in the mid-$180 price range, due to what I saw was a scenario of potentially accelerating capital returns. The technology company saw strong product uptake in the Services business in the last quarter, leading to a record 28% revenue share in this category. However, Apple is seeing no growth in the largest revenue category and shares are now the most expensive in the Big-5 tech industry group while offering the lowest expected EPS growth. With Buffett’s drastic reduction in its Apple investment in the second-quarter also creating uncertainty, I am changing my rating to hold.

Apple beat earnings estimates

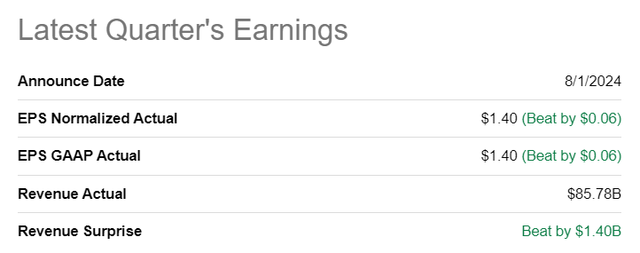

Apple beat average Wall Street estimates for Q3 revenues and earnings by decent margins. The technology company reported adjusted earnings of $1.40 per-share, which beat the consensus estimate by $0.06 per-share. Revenue came in at $85.8B, a June-quarter record, and beat the average prediction by a significant $1.4B, chiefly due to strength in Services.

Seeking Alpha

Apple’s top line picture growth remains weak, but Services remain a bright spot

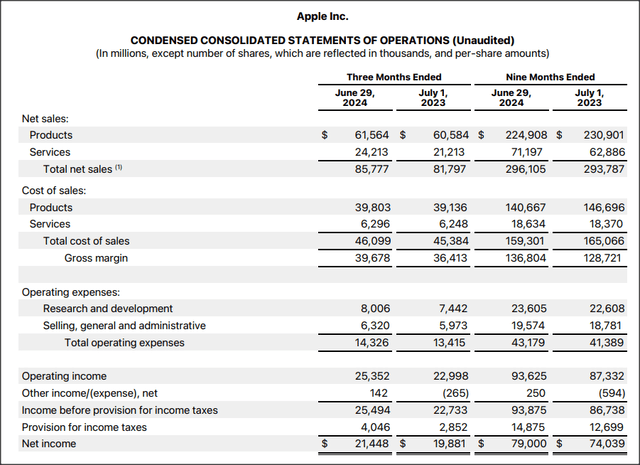

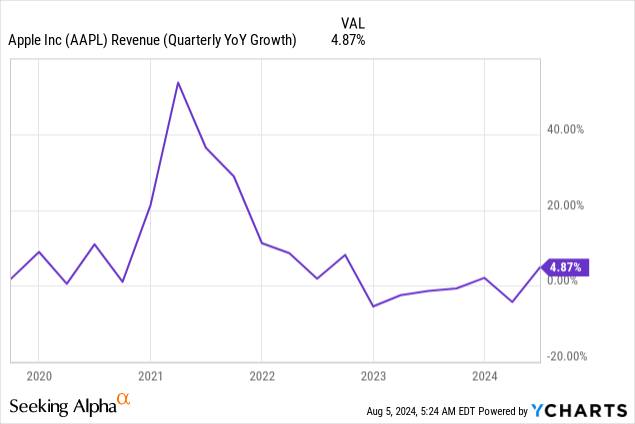

In the third-quarter, Apple’s returned to positive top line growth as its revenues reached $85.8B, showing 5% year over year growth. In the previous quarter, weak iPhone sales actually caused Apple’s consolidated revenues to fall 4% year over year.

While iPhone revenues continued to decline in Q3’24 (they were down 1% year over year to $39.7B), Apple has again offset weakness in its biggest hardware category with growth in Services. In fact, Services reached a new all-time revenue high of $24.2B in the third-quarter, resulting in a segment top line growth rate of +14% Y/Y. Services include AppleCare, Apple One, Apple TV+, iCloud, Apple Music, Apple Pay and other non-hardware related revenue streams and have been a bright spot for Apple. With growing product uptake in Services, the segment represented a revenue share of 28% in Q3’24 compared against a revenue percentage of 26% in the year-earlier period. Only iPads had a faster revenue growth rate from a category standpoint than Services (+24% Y/Y) in the third-quarter.

Not only does Services see the second-fastest category revenue growth within Apple’s portfolio, but Services is also becoming more important as a revenue contributor on a consolidated basis. In the longer term, I see Apple’s Services contribute at least one-third of total revenues.

Apple

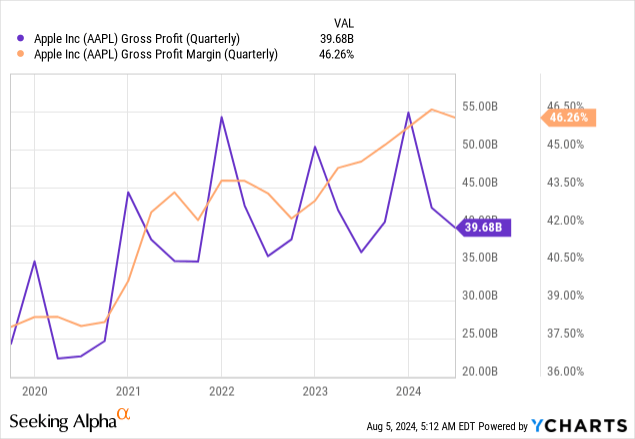

Apple did remain widely profitable, however, as was expected. The high-margin Services business has driven an expansion in Apple’s gross margin in the last several years: in Q3’24, Apple’s gross margin reached 46.3%, showing a solid 1.7 PP margin gain year over year. While the Services business stole the show once again in Apple’s Q3 earnings release, it was also just reported that Warren Buffett drastically cut its stake in the technology company, possibly because of Apple’s weak top line growth prospects.

Implications of Buffett’s Q2 Apple sale

Warren Buffett’s Berkshire Hathaway just disclosed in a regulatory filing that it cut its investment in Apple by about half in the second-quarter. Berkshire Hathaway sold 390 million shares of Apple in Q2, following a sale of 115 million shares in the previous quarter. Berkshire Hathaway still owned shares valued at $84.2B at the end of the second-quarter, however. Apple has been the single largest stock position in Berkshire Hathaway’s portfolio in 2016.

Warren Buffett’s Q2 Apple sale is set to add some pressure on the technology company’s stock, in my opinion, and it raises questions as to why the famed investor sold. One reason may be Apple’s lack of material hardware-related growth, indicating that the investor doesn’t expect a reinvigoration of the company’s top line given the absence of any major new product launches. Apple has not produced any significant growth in its top line for years as iPhone sales started to taper off after the pandemic.

Another reason may be Apple’s now stretched valuation. Since Berkshire Hathaway started to buy into Apple in 2016, at a much lower price, the investment company booked serious capital gains from its recent sales. In the short term, I expect Apple to suffer from negative sentiment hang, and I would not be surprised to see Apple stock sales in the Berkshire Hathaway portfolio in Q3.

The lesson here is that Buffett likely expects a recession, or at least a major correction in the stock market… which, given yesterday’s market slump, is a concern many investors may now share as well. Since technology companies have done extremely well in the last two years, especially Apple, the tech segment may be especially vulnerable to a valuation draw-down. With Buffett scaling back its tech exposure, investors may want to evaluate whether they are also overweight high-priced, low-growth investments like Apple that are vulnerable to profit-taking.

Apple’s valuation

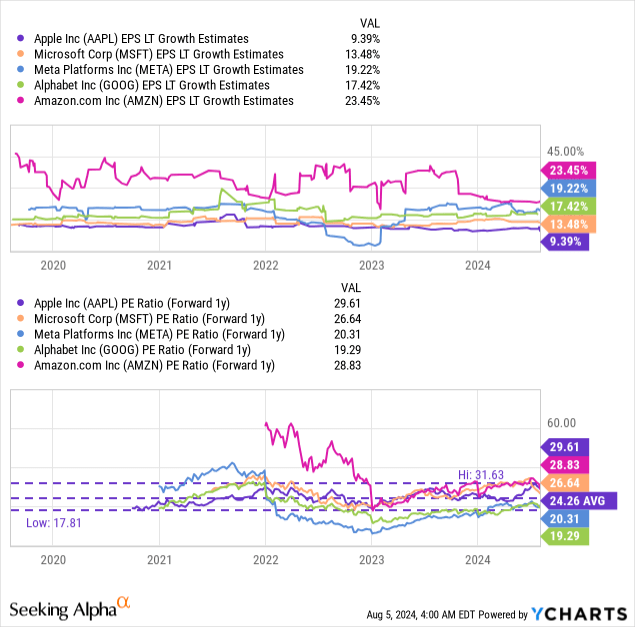

Apple’s shares are priced at a P/E ratio of 29.6X which makes the company the most expensive technology investment in the top-5 large-cap tech industry group. The average P/E ratio in the industry group is 24.9X while Apple’s long term P/E ratio is 24.3X (implying a 22% premium). Amazon (AMZN) is trading at a 21% discount to its 3-year average P/E ratio, Microsoft (MSFT) at a 6% discount, Alphabet (GOOG) at a 7% discount and Meta Platforms (META) at a 14% premium.

It is also noteworthy that due to headwinds in the iPhone category, Apple is expected to see the weakest long-term earnings per-share growth of only 9.4%. In other words, Apple is the most expensive tech company in the industry group here while offering investors the slowest EPS growth. In my opinion, Alphabet offers investors the best bang for their bucks right now, while Meta Platforms is also a buy, based off of valuation and free cash flow.

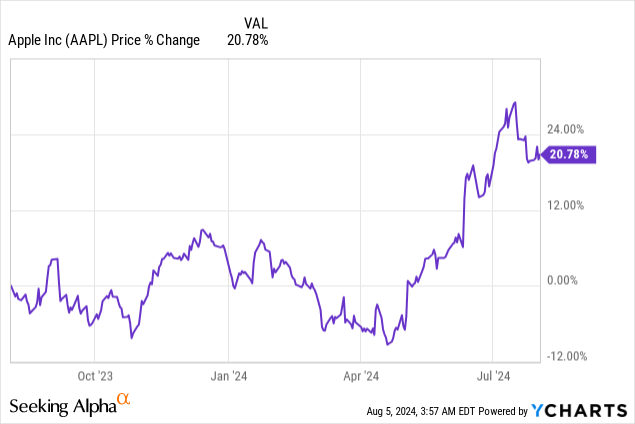

In my last work on Apple in May I argued that I saw a fair value for Apple’s shares of $215 (which implied a 30X forward P/E ratio). This fair value was based off of growing Services revenue share and potential for stock buybacks as a means for the company to return a large portion of its operating profits and free cash flow to shareholders. Since Apple has reached my stock price target — shares are currently trading at $220 — I am changing my rating to hold. What adds to my hold rating is the fact that Berkshire Hathaway has drastically reduced its stake in the technology company, which could be seen as a loss of confidence in Apple’s growth prospects.

Apple’s risks

Apple is still overly concentrated in hardware-related revenue streams, which together represented 72% of the firm’s consolidated top line in the third-quarter. What further adds to the company’s risks, in my opinion, is that Apple is focused chiefly on the consumer electronics market which tends to be cyclical and which therefore creates earnings and free cash flow headwinds for Apple during a downturn. Within the hardware category, Apple is seeing slowing growth for the company’s flagship product iPhones which Apple has not yet been able to replace with another hardware product.

Closing thoughts

Apple is a well-run technology company with considerable momentum in Services which has resulted in strong gross margin gains in the last few years. Services now represent 28% of consolidated revenues. However, the hardware category, especially iPhones, is becoming a drag on Apple’s growth. I believe the risks inherent in the hardware category are counterbalanced by continual momentum in Services, but Apple’s shares have now reached my fair value target, triggering a change in rating to hold. I also believe that Buffett’s sale of Apple in Q2 will have deep implications for investors from a sentiment point of view and may limit any further upside, especially given that Apple is now trading at a high 30X P/E ratio. With shares reaching my stock price target and Buffett’s actions potentially creating negative sentiment overhang, I am down-grading Apple to hold.

Read the full article here

")