")

Investment action

I recommended a buy rating for Dun & Bradstreet Holdings (NYSE:DNB) when I wrote about it in May, as I expected the business to achieve 7% organic growth over the medium term as demand for DNB’s Master Data Management [MDM] has been great so far. Based on my current outlook and analysis, I recommend a buy rating, as I still think the organic growth story is intact. With the Fed likely to cut rates in 2H24, it should lead to a turnaround in growth for the revenue segments that are not tracking well against DNB’s medium-term target of 5 to 7% growth.

(Note: my review focuses on the fundamentals rather than the potential takeout scenario, since nothing is confirmed yet.).

Review

DNB reported 2Q24 earnings last Thursday, with revenue showing 3.9% y/y growth to $576.2 million, falling behind street’s expectation of 4.7%. On an organic basis, revenue grew 4.3% y/y, with North America revenue growing 3.4% y/y and international revenue growing 6.4%. In North America, Finance & Risk (F&R) segment organic revenue grew 2.6% y/y, driven by a net increase in revenue across third-party risk, supply chain risk management, and finance solutions, partially offset by decreased revenue from Credibility Solutions. As for the Sales & Marketing (S&M) segment, organic revenue grew 4.2% y/y, driven by MDM Solutions, partially offset by decreased revenue from digital marketing solutions. In International, F&R revenue saw 8.9% organic growth y/y, driven by high demand for risk solutions, while S&M organic revenue growth of 1.6% was driven by UK demand for data delivered through API solutions. While revenue disappointed relative to expectations, margins came in better. Adj EBITDA margin expanded by 60bps y/y to 37.8%, coming in above the street’s estimate of 37.5% as DNB saw benefits from operating leverage and cost efficiencies.

Putting aside the news of DNB exploring a sale, which drove up the stock price, the market seemed to be disappointed by DNB’s results as the share fell sharply by close to 12% (low point of August 1st). I believe the contributing factor was that organic revenue growth did not accelerate from 1Q24, which sort of put a dent in the organic growth acceleration story. Management is also guiding for FY24 organic growth to come in at the low end of its previous guidance (4.1% to 5.1%). If it comes in at 4.1%, it implies no improvement in organic growth vs. FY24, which pushes back the timeline for DNB to reach 7% organic growth (the high end of the midterm target).

In my opinion, the organic growth story still remains intact, but probably delayed by 1 year. Management guidance also seems to be conservative considering that the Feds are likely to cut rates in the coming months, which should improve over-demand sentiment, especially in the small-and-medium businesses [SMB] customer cohort.

Objectively, the majority of DNB revenue streams continue to perform well, with 90% of revenue growing by more than 6% on a last-twelve months [LTM] basis, tracking nicely against management’s 5-7% med-term goal, and retention rates are still at very healthy levels (96%), which clearly demonstrates the stickiness of DNB’s products and solutions. Importantly, DNB’s MDM continues to see strong demand, and this puts DNB in a better position to drive adoption for its GenAI analytics. On the point of GenAI products, DNB investments in new product innovations should allow it to capture demand. The uptake of new products seems to be fairly solid as well. Take the Hoovers SmartMail AI, for instance; it was launched in 2Q and is already being used by 4,000 clients. On an overall basis, the vitality index is also up 400bps from 32% in 1Q24 to 36% in 2Q24, indicating a larger portion of business is being driven by new products.

I believe the weakness in organic growth (in 2Q24 and expectations for FY24) is because of macro reasons, which pressured marketing budgets and SMBs. DNB digital marketing revenue was heavily impacted as businesses pulled back on marketing budgets due to macro challenges and fewer than expected rate cuts. The uncertainty over Google’s third-party cookie policy also remained an overhang on demand. While I am not sure of how the Google situation will play out, I think it is increasingly likely that rates are going to be cut (last Friday US job data was pretty bleak), and that should ease the cost of capital for many businesses (i.e., less budget scrutiny). Cutting rates should also ease the pressure that SMBs are feeling now, which should allow DNB to see a recovery in its credibility business (fell 7% in 2Q24).

These two revenue segments represent the last 10% that is not growing at >6% on a LTM basis. If we make the assumption that the macro situation will turn for the better in the coming quarters, I am quite confident that this 10% will flip to positive growth, and combined with the remaining 90% still growing at >6%, the organic growth story remains intact. Moreover, management is only going to raise prices by 2.5% in 2024, which is below inflation levels (wage inflation is 5.1%, for example). This leaves room for upside, in my opinion.

In addition, I should bring the reader’s attention to DNB’s FCF profile. After a year of poor FCF conversion (adj net income to FCF) in FY23, the conversion rate is expected to return to 80% in FY25 as DNB sees declining capex, the elimination of duplicative costs with the cloud transformation, and reduced back-office expenses. This should give DNB more capital to reinvest in growth.

Valuation

Author’s work

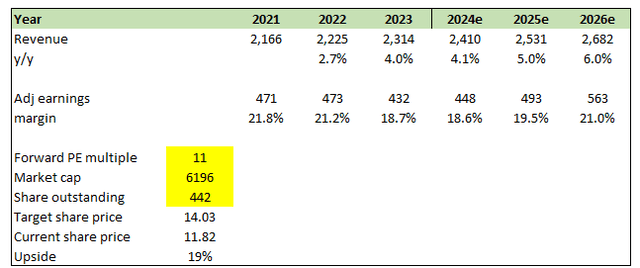

Even after the sharp increase in share price (post the potential sale news), the upside to DNB’s share remains quite attractive with non-aggressive assumptions. In my latest model, I pushed back the timing of DNB achieving 7% organic growth by 1 year to FY27, now assuming FY26 organic growth to be 6% and that FY24 will achieve 4.1% organic growth (low end of the previous guided range). I must note that these are conservative assumptions since 90% of revenue is growing >6% on a LTM basis, and the remaining 10% should see a turnaround when the macro backdrop gets better. I have also adjusted my margin assumptions downward, now assuming FY26 to achieve a 21% margin vs. the prior view of 22% as growth is slower.

A positive development on valuation multiples is that the market has “showed” us that they are willing to value DNB at a higher multiple (valuation went up from ~9.6x forward PE to 11x post-news). Assuming 11x is the “floor” that the market has set for DNB, the stock should trade at ~$14.

On a historical basis, 11x is also not demanding by any means. Over the past two years, when organic growth was at ~3%, the stock traded at 11x. With organic growth reaching back to ~6+% and the FCF conversion rate back to 80%, I don’t see any major reason why DNB should not trade at 11x.

Risk

The lack of organic growth acceleration in 2Q24 is indeed a red flag. While I am not concluding that there is a structural impairment to the organic growth story, if this persists for the next few quarters despite the macro backdrop turning better, It may suggest that DNB is facing a bigger problem than expected in terms of demand. That would force me to change my views on the stock.

Final thoughts

My recommendation is still a buy rating for DNB, as the organic growth story remains intact. While the macroeconomic environment remains uncertain, I believe this will go away as the Fed cuts rates. As economic conditions improve and interest rates decline, it bodes well for DNB, as demand sentiment should improve. DNB’s new products are also gaining momentum, as seen from the vitality index, which should position it well to capitalize on new opportunities (GenAI, in particular).

Read the full article here

")