")

Intel (NASDAQ:INTC) had one of its worst days of all-time, as the company’s almost 6% decline on last Thursday came with a more than 20% decline on last Friday. The company once again lowered its guidance as it continues to face strong pressure in the market and with customers. Despite being too optimistic before earnings, as we discussed in our pre-earnings article here, we still view the company as a strong investment.

As we’ll see throughout this article, the company’s weakness represents a cautious entry point.

Intel Cost Reduction Plan

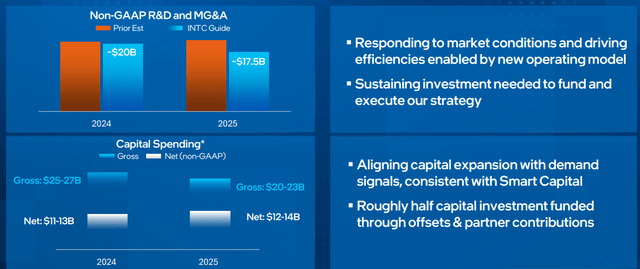

The biggest thing to come out of Intel’s earnings is the company’s announced cost reduction plan.

Intel Investor Presentation

The company is planning to cut R&D and MG&A modestly in 2024, but by more than $2 billion in 2025. The key part of the thesis here is the company’s point that in 2024 it had 10% less employees but $25 billion more revenue. The company’s response to market conditions is necessary as the company learns to manage capital spending.

However, it’s worth noting that I believe firing 15% of your workforce crushes morale and likely leaves a lot of the company not caring about its long-term success. That’s a pressure that Intel will need to face and intelligently handle in order to be able to right the ship.

Intel 5N4Y Goal

Intel is continuing to choose its lofty goal of 5 nodes in 4 years and as a part of that, the company has been betting on 18A.

Intel Investor Presentation

The company is touting strong improvement for 18A with 15% perf/watt increase versus Intel 3 and 1.3x chip density. That combines with the company’s advanced packaging and other new accomplishments. The company expects to start volume ramp early next year, and it needs to do it without the embarrassing voltage failures of the 13th and the 14th generation.

This was an ambitious project for the company, and while there’s a lot of debate over what truly constitutes a node these days, it’s an impressive accomplishment for the company. It’s worth noting that TSMC argues that the process is competitive to its 3nm, however, the results remain to be seen when the process comes out.

Intel AI PC Positioning

One sign of strength in Intel’s portfolio is the company’s positioning in the artificial intelligence industry.

Intel Investor Presentation

The company has continued to build new chips, and it is the dominant consumer partnered company here. The company has built integrated graphics tales and a lot of its top-tier chips here are also partially built on TSMC processes, which helps the company remain on the cutting edge despite foundry struggles.

Important features in AI could lead to a cycle of customers upgrading their PCs to catch up in hardware capabilities.

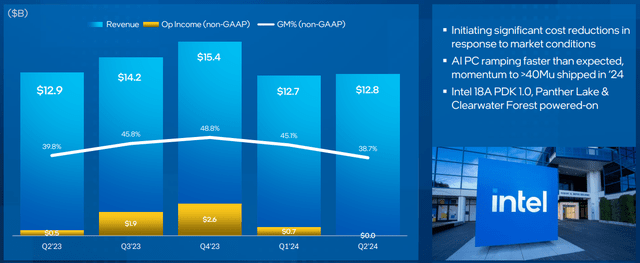

Intel Financial Results

Financially, the company’s struggles are clear as it continues to fight to go through a massive investment cycle.

Intel Investor Presentation

The company’s breaking even overall, with its 38.7% margin. That’s a relatively weak margin in the industry, as the company’s revenue has remained strong, but other segments have suffered. The company’s cost reductions and AI PC ramp-up could help enable it to be able to return to normalcy here.

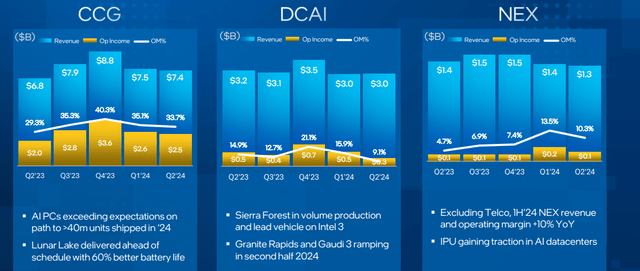

Intel Investor Presentation

The company’s CFG division continues to be its strongest, with $2.5 billion in operating income and more than half of the company’s revenue. The company is ahead of expectations here and Lunar Lake has continued to perform well taking advantage of TSMC tiles as well. The company’s DCAI and NEX businesses continue to have positive operating income ~10% range.

These are strong divisions with large scale customers. The company’s margins have been pushed down by competitive pressures.

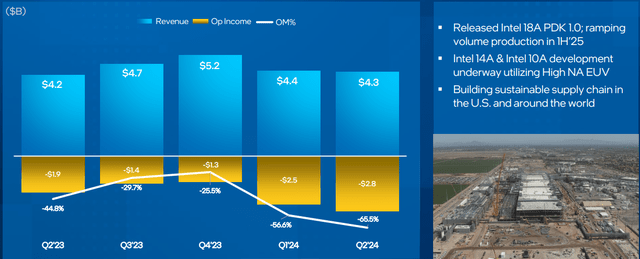

Intel Investor Presentation

The company’s continued massive source of spending continues to be its foundry division. The company has released its Intel 18A PDK and is working to achieve volume production in 1H’25. The company is also developing Intel 14A and 10A as a leader in high NA EUV machines. Intel has bought AMSL’s entire 2024 stock.

The company is in its era of massive capital spending and investment, but of course $2.8 billion in operating income losses are difficult to see with a -66% margin. Intel is targeting 2023 profitability here with massive investments and whether that succeeds remains to be seen.

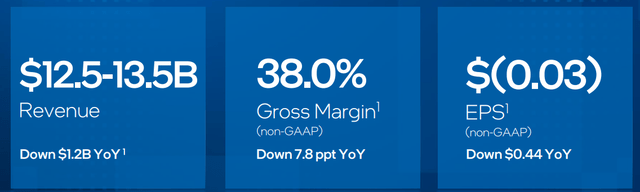

Intel Shareholder Returns

Intel’s path to shareholder returns is fighting against weak guidance, with a decrease in revenue YoY and a 38% gross margin.

Intel Investor Presentation

The company is going to be slightly negative in regards to EPS. It needs to consistently keep spending substantial amounts of capital, with the company’s foundry expenditures costing it billions of dollars. The company needs to find the cash to start driving shareholder returns at some point, but investors might need to wait until the end of the decade.

However, Intel’s management is doing everything it needs to do, the question is whether it’s doing too little too late.

- Foundry. The company is treating its foundry as an independent company, a company within the company that needs to compete with TSMC. It’s using innovations such as Power Via to attempt to compete but forcing other divisions to treat this one as a customer. The company needs to be able to succeed here.

- 18A. The company has bet its future on the foundry division and being able to compete with both Samsung and TSMC. Most people believe that Samsung is behind TSMC, but Intel needs to be competitive with both of them to get cutting edge nodes.

- ARM. x86 has a problem. The age of the instruction set means it’s less efficient than ARM, as it needs to provide backwards compatibility for software. Now, Intel is using its expertise to manufacture an ARM-based CPU, showing how it’s diversifying outside of its core business.

- TSMC. Intel at the same time is derisking its strong CPU design business from its foundry business by using TSMC tiles to great success. That protects the company and enables it to continue growing despite struggles from the foundry business.

Intel might not be able to drive strong cash flow shareholder returns today. But the company is working hard to build up a business and drive long-term shareholder returns, and it’s making the right decisions. We expect it to grow substantially to generate strong shareholder returns by the end of the decade.

Thesis Risk

The largest risk to our thesis is Intel is a company in decline surrounded by much larger peers. These companies can outcompete the company on both investment and talent. Amazon is expecting annualized capex to cross $60 billion, while Intel struggles to afford much smaller capex. Amazon is also making its own chips.

The company’s chips aren’t as fast as Intel’s on a core by core basis, but they are cheaper per unit processing power, given that the company doesn’t need to pay Intel’s margins. Amazon might not be directly competing in AI, but AWS is benefiting from AI and the company offering customers lower prices on Graviton than Intel instances will help.

That can hurt Intel’s ability to recover.

Conclusion

Intel is a company in transition. The company needs to be able to handle a market with growing competition from companies such as TSMC and Samsung. At the same time, perhaps the company’s biggest risk is growing customers that can now make their own processors. These include cloud providers like AWS and Google, along with all-in companies like Apple.

Despite that, perhaps too late, the company is making the decision to right-size its portfolio. It’s working to manage its expenses and build nodes that are once again competitive. At the same time, by being willing to build ARM processors, and use TSMC tiles, the company will be much better positioned to manage its competitiveness and shareholder returns.

As a result, we don’t see Intel as a value trap, but a unique opportunity at this time.

Read the full article here

")