")

")

Investment Thesis

AppLovin Corp. (NASDAQ:APP) will be reporting its Q2 FY24 earnings this week on Wednesday, August 7th, after markets close for business.

The Palo Alto, CA-based ad-tech platform company has had a remarkable turnaround since 2022, as I have detailed in both my previous coverages on AppLovin, showcasing the fundamental strength of its underlying app monetization and ad distribution technology. AI has been the cornerstone in the company’s turnaround, allowing AppLovin to post strong growth but, more importantly, for GAAP operating income to grow six-fold over the past four quarters on a TTM basis.

In my previous coverage, I expressed optimism about AppLovin’s earnings growth rates, where I mentioned that “I believe AppLovin is positioned to grow its margins even more, assuming the company is able to maintain current growth rates.”

At the same time, the ad spend landscape looks to be mixed. While major Big Tech ad platforms have posted respectable growth in their ad products, research indicates some weaknesses that could be forming in pockets of the digital ad landscape.

However, I still believe AppLovin is well-positioned to grow its digital ad business over the next few quarters, despite the mixed ad outlook. Further, the strong growth the company has demonstrated in its earnings should outweigh any debt concerns.

I continue to recommend a Buy on AppLovin.

Recapping the Mixed Ad Landscape

With the Q2 earnings season well under way, I believe insights from earnings calls and reports from major Big Tech ad platforms will provide strong indications of what to expect from AppLovin.

Alphabet’s Google (GOOG) began the earnings season posting strong search & advertising revenues of 14% growth in Q2, mirroring the growth seen in the previous quarter. YouTube demonstrated a similar growth in ad revenue, growing 13% due to strong momentum in CTV (Connected TV) and brand advertising.

Meta Platforms (META) reported strong Q2 ad revenue growth and went on to further add that the total number of ad impressions & the average price per ad “both increased 10%.” Simultaneously, Amazon (AMZN) is now clocking a $50 billion revenue run rate in their ad business on a TTM basis and has incrementally added an additional $2 billion in ad sales in Q2 alone.

All three ad platforms sounded quite optimistic about continued ad growth moving forward, with Meta Platforms sounding the most optimistic of the lot due to the robust ad spending they were seeing in their ex-U.S. regions, such as APAC, which is growing its ad revenue by nearly 30% y/y. Plus, all three ad platforms talked about how AI was helping each of their platforms’ advertisers see a better lift on their ads and achieve higher ad monetization rates.

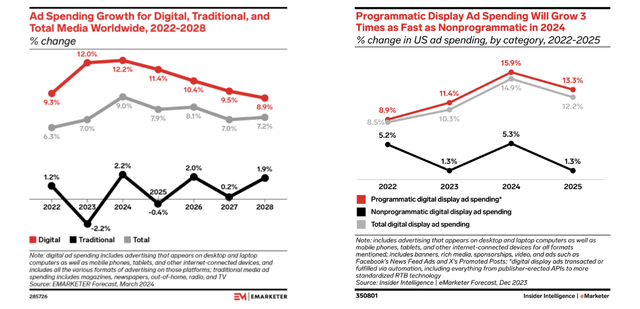

At the same time, research indicates that digital ad spend will grow 11-12% in FY24 and FY25, down from the 11-13% growth that was initially expected.

Exhibit A: Programmatic Ad spend is expected to outgrow the overall Digital Ad spend (eMarketer)

However, programmatic display ads are still expected to outgrow the digital ad spend growth rates, as I have illustrated in Exhibit A above.

This mixed outlook is still quite positive for AppLovin’s Software Platform which drives the majority of the company’s high-growth, high-margin products, such as AppDiscovery & Max in my opinion.

Implications for AppLovin Heading Into Q2

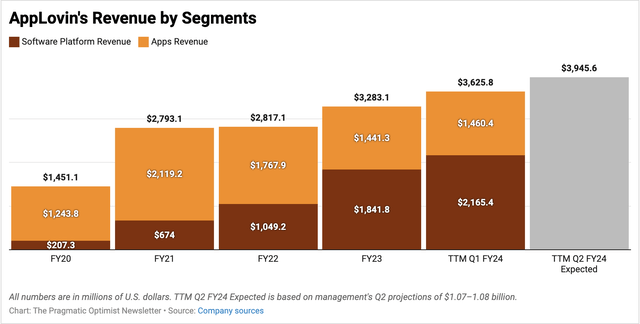

The strength of AppLovin’s Software Platform was on full display in the Q1 quarter, as the company reported a 91% growth in Q1 segment sales to $678 million and pulled the total Q1 revenue growth rate of the company to 48% y/y to $1058 million.

In my previous coverage, I made the following observation about a product on AppLovin’s AppDiscovery platform:

While cross-checking this data in their quarterly filing related to this earnings report, I found that while revenue per installation increased by 5%, the volume of installations skyrocketed by 87%, which I take as a sign of increased ad efficiency.

These results were a reflection of the robust investments management had made, such as the rapid deployment of their entire AI stack on Google’s GCP platform.

Through Q2 FY24, I noticed that AppLovin has continued adding features and enhancements to their Max product that focus on brand safety, monetization, and inventory supply. Max is AppLovin’s in-house bidding algorithm provided for free to ad publishers, and AppLovin earns a ~5% take rate from advertisers who bid through Max.

I believe AppLovin should be well on track to achieve their Q2 revenue targets of $1.07-1.08 billion, putting them on the path of achieving strong double-digit growth rates this year. The addition of AppLovin’s product features combined with the outlook on programmatic ads that I noted in the previous section implies a >20% top-line growth rate through FY25, in my opinion.

Exhibit B: AppLovin’s Revenue Trends on an annual and TTM basis. (Company filings & reports)

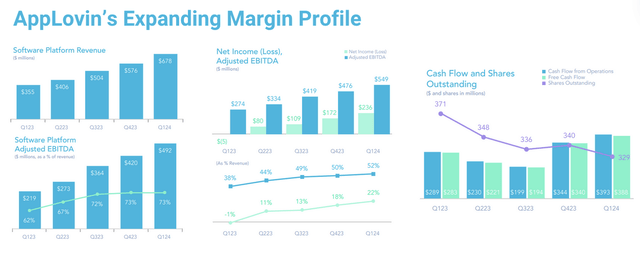

Plus, the strong growth in AppLovin’s high-margin, high-growth Software Platform business should continue to keep margin expansion buoyant. As noted in Exhibit C, AppLovin’s adjusted EBITDA margins are robustly expanding, now at ~49% on a TTM basis after accounting for their Q1 performance.

Exhibit C: AppLovin’s Revenue Trends on an annual and TTM basis. (Q1 Investor Presentation, AppLovin)

If I factor in management’s adjusted EBITDA Q2 targets of $550-570 million, I estimate AppLovin’s adjusted EBITDA TTM margins to expand by 1.7% sequentially to 50.7% in Q2. This is very impressive, in my opinion, and I will be curious to see what management has in store for their Q3 targets.

Markets can be skeptical of these growth rates given the company’s high debt load. Per their Q1 filings, AppLovin holds ~$3.5 billion in LT debt, while cash & equivalents total ~$436 million. In terms of leverage, I estimate the company will maintain a 1.6-1.8x leverage ratio, which is extremely manageable due to the 50% adjusted EBITDA margins.

Agreed, that the interest expense of ~$270 million the company incurs will depress its valuation potential, but my valuation indicates that the company is positioned to benefit from strong growth despite its debt load.

Valuation points to upside for AppLovin

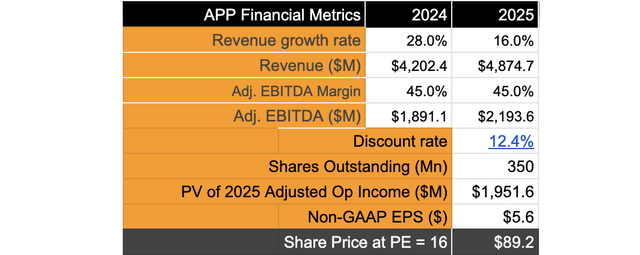

As I noted in previous sections, I believe the company is still well positioned to maintain top-line growth rates of at least 20% through FY25 with the strong line-up of enhancements and features that the company is continuing to add. I am being conservative here, since I had previously expected at least 25% in H2 of this year.

On the adjusted EBITDA margin front, I have been conservative again and assumed the company will grow its adjusted EBITDA in line with its top-line revenue despite the strong +50% adjusted EBITDA margin pace the company is currently demonstrating. The high-margin, high-growth Software Platform segment should drive margin expansion for AppLovin. My model assumes a 12.4% discount rate.

Exhibit D: AppLovin is well positioned for upside heading into Q2 (Author)

The +20% CAGR growth in adjusted earnings should warrant a valuation multiple in the range of 38-40x. However, with interest expenses of ~$270 million per year due to its long-term debt, I believe a valuation multiple of ~16x may be applied to AppLovin. This implies an upside of ~31% from AppLovin’s current levels.

Risks & Other Factors to Look For in AppLovin’s Q2 Report

- Q2 Expectations: Markets expect AppLovin to report Q2 FY24 earnings of 72 cents per share, more than four times the 22 cents that were reported in Q2 of last year, while Q2 FY24 revenues are expected to be worth $1.08 billion, growing 44% y/y. This is at the high end of AppLovin’s own revenue target range of $1.07-1.08 billion.

- Forward Expectations: For Q3, markets expect AppLovin’s management to guide to $1.1 billion in sales, up ~28% y/y while full-year FY24 revenues are expected to grow 33% y/y to $4.38 billion. Management has refrained from providing full-year outlooks, citing macroeconomic uncertainties, but with two quarters of data in after their Q2 earnings, there may be a chance for investors to hear about AppLovin’s full-year outlook.

- Digital Ad Landscape Commentary: I will personally be interested in understanding how management thinks about the landscape and the road so far. Any updates from their Wurl CTV business should be well received if provided. Moreover, in addition to the broader landscape and ad monetization efficiencies of their products, I will also be interested in learning about Google’s withdrawal of the cookie deprecation. So far, Sandbox testing data shows the impact of cookie deprecation was less than expected. But with Google sunsetting its cookie deprecation project, it should provide an additional boost to AppLovin’s outlook.

- Macroeconomic outlook: The last two weeks of economic data have cast a shadow on the overall positive outlook for the economy. Ad spending is one of the first areas where slowdowns are usually seen, especially in brand advertising. So far, companies have not reported anything out-of-the-ordinary, and I will be looking to see if AppLovin’s management sees any anomalies here.

-

Peer events: The Trade Desk (TTD), a large indirect peer to AppLovin, will be reporting its own Q2 earnings the following day, on August 8th, after markets close. Any deviation in TTD’s earnings versus AppLovin’s earnings will impact the latter.

Takeaway

So far, AppLovin has been enjoying the wild ride in its stock, supported by robust top-line and bottom-line growth. The strength of AppLovin’s fast-growing Software Platforms segment overshadows any valuation concerns arising from its sizable debt load. I expect management to report another solid performance in Q2 and am positive about their expectations for continued momentum in Q3 and beyond.

I continue to recommend my Buy rating on AppLovin.

Read the full article here

")

")