")

")

")

")

Investment Thesis

Meta Platforms’ (NASDAQ:META) stock rallied over 6% in aftermarket as the company topped both revenue and GAAP EPS estimates, but subsequently reversed course due to an ongoing market pullback. We know that Google’s (GOOG) (GOOGL) advertising revenue, particularly YouTube ads, came in light in its 2Q earnings release. META also experienced some softness in its advertising revenue. However, investors are focused on META’s capex outlook. The company has increased its capex outlook for FY2024 to continue focusing on AI innovations, which is a positive signal especially compared to Google’s muted capex expansion.

In my previous coverage, I rated META as a “buy” and continue to believe that the stock has strong upside potential due to its elevated capex on GenAI. META is currently developing Llama 4, a faster open-source large language AI model expected to have nearly ten times the training capability of its previous version. Despite the resiliency of its stock amid the current market selloff, the stock is trading at a non-GAAP P/E fwd of 17.4x, which remains appealing. Therefore, I reiterate my “buy” rating, as META’s strong track record in monetization and increased capex on GenAI should support its growth trajectory

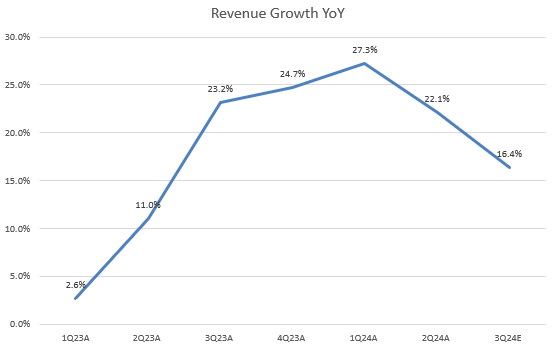

Revenue Growth Shows Softness

The company model

Despite META’s revenue beating market consensus in Q2 FY2024, we can see that its top-line growth momentum has significantly decelerated. While management expects the midpoint of its revenue guidance for Q3 FY2024 to be $39.75 billion, above the consensus, this outlook implies a further growth slowdown to 16.4% YoY. Similarly, we also notice that Google’s YouTube ads growth significantly decelerated to 13% YoY in Q2 FY2024, down from 20.9% YoY in the previous quarter.

Here is a question: why did GOOGL trigger a 5% selloff while META rallied 6% on the next day following their earnings results? I believe investors care more about a company’s long-term growth trajectory rather than a cyclical slowdown. We should know that both companies significantly grew their revenue in Q3 FY2023, which might result in a YoY slowdown due to a higher basis. To remain competitive and maintain growth in the current GenAI race, companies must increase capital investments. Clearly, META has done a better job compared to Google.

GenAI Will Create a Massive Monetization Opportunities

During the Q2 earnings call, the CEO Mark Zuckerberg highlighted numerous opportunities for GenAI monetization. GenAI can enhance the core ads business by boosting user engagement on Family of Apps. For example, Threads is about to hit 200 million monthly active users, and Meta AI has already handled billions of queries. With increased capex on AI infrastructure, META continues to scale GenAI training capacity to advance its foundation models. Meta AI is currently supported by Llama 3.1, released last quarter, which includes the first frontier-level open-source model. As mentioned earlier, the company is now working on Llama 4, expected to be released next year.

META’s GenAI technology also extends to other fields, such as Ray-Ban Meta Glasses, which are showing early success as demand is significantly outpacing supply. Therefore, I believe the company is on the right track to maintain its growing capex, driving strong growth through significant GenAI monetization opportunities from future AR glasses to Metaverse.

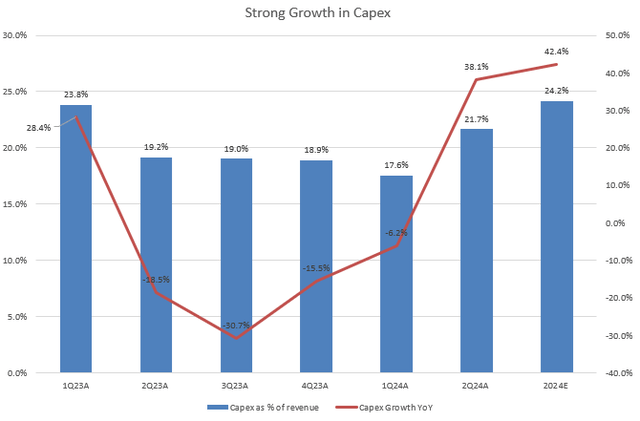

Significant Capex Boost Drives Long-Term Revenue Growth

The company model

As mentioned, META is entering another capex cycle in FY2024 after a decline in FY2023. Following a growth slowdown in FY2022, which saw a 1% revenue decline, the company’s revenue showed a significant rebound in FY2023, driven by a strong ROI from a 68% YoY increase in capex in FY2022. Similarly, in Q2 FY2024, META’s capex grew by 38.1% YoY, compared to a -6.2% YoY growth in Q1 FY2024, which may coincide with some growth softness.

Additionally, we can see in the chart that its capex as a percentage of revenue increased for the first time after seven quarters of decline, reaching 21.7%, a substantial boost from 17.6% in Q1 FY2024. Most importantly, the company raised its FY2024 capex guidance to a range of $37 billion to $40 billion, up from the previous range of $35 billion to $40 billion. Based on the company’s FY2024 revenue outlook, this translates into a 42.4% YoY growth in capex and 24.2% capex as a percentage of revenue in FY2024. These numbers imply that the capex growth is expected to be stronger in 2H FY2024.

Furthermore, during the earnings call, CFO Susan Li mentioned, “We currently expect significant CapEx growth in 2025 as we invest to support our AI research and our product development efforts.” This indicates that capex will not show any softness but even stronger in FY2025, which excites investors. Therefore, based on META’s previous success in AI monetization, I believe the company’s growth momentum will reaccelerate (assuming no incoming recession). However, there is a catch: META’s FCF profile will be under pressure while significant increase in capex. I believe FCF may experience YoY decline in 2H FY2024.

Valuation

Seeking Alpha

META’s valuation multiples are still relatively cheap among the “Magnificent 7” group, considering its strong growth potential with the increased capex outlook. Despite a tremendous growth opportunity under the GenAI roadmap, its GAAP P/E TTM sits at 25x, nearly in line with its 5-year average. Furthermore, if we exclude the company’s stock-based compensation, its non-GAAP P/E TTM drops to roughly 20x. Factoring in META’s earnings growth consensus, its non-GAAP forward P/E would be 17.4x, significantly lower than the S&P 500 index’s forward P/E of 22x. This is largely due to its attractive non-GAAP forward PEG ratio of 1.25x, which is 17% below its 5-year average and 9% below its sector average, according to Seeking Alpha. The ratio is also lower than GOOGL’s 1.28x. Therefore, I believe META’s stock remains attractive despite the broad-based market selloff over the past two weeks.

Conclusion

In conclusion, while META’s advertising revenue may slow down in the near term, its earnings growth remains resilient. Based on the company’s previous capex cycle, I’m confident that META can navigate near-term growth softness and reaccelerate growth over the long term. Particularly under the current AI boom, META’s continued upgrades in its GenAI model, supported by significant increases in capital spending, make the company more competitive compared to peers like Google, which has shown relatively weaker capex momentum. Moreover, the stock’s current valuation is still attractive, with its P/E multiple closer to its 5-year history. Combined with META’s track record to monetize its AI investments, this suggests potential for multiple expansion in valuation. The stock’s near-term momentum is largely impacted by the recent market pullback due to potential economic slowdown, creating a buying opportunity during any stock pullback. Therefore, I still maintain a “buy” rating for META.

Read the full article here

")

")

")

: Back To Its Margin Expansion And Hyper Growth Path")