Introduction

GigaCloud Technology (NASDAQ:GCT) has had an amazing run since the bottom of March last year, so I wanted to take a look at the company’s financials in more depth to see if it would be a good time to start a position. The company’s top-line growth has been phenomenal, while margins are continuing to rise. The question is if that top-line growth is sustainable, but if we take some conservative estimates, the company’s growth can slow down quite a bit to still be an attractive investment, therefore, I am initiating a buy rating, and have opened a small position.

Briefly on the Company

GCT is a global end-to-end B2B e-commerce solutions platform. The company helps connect manufacturers of big-ticket items like furniture and sports equipment primarily in Asia, with resellers of such items primarily in the US, Asia, and Europe. Being end-to-end, the company essentially does all the work associated with getting the items from A to B. For instance, the company holds the inventory of the manufacturer’s products to be shipped to the buyer, usually an online business, taking care of all the logistics. It is essentially a drop shipping business, which has many fulfillment centers that help manufacturers store their inventory for e-commerce businesses, and then from these businesses, customers get their items delivered to them.

Financials

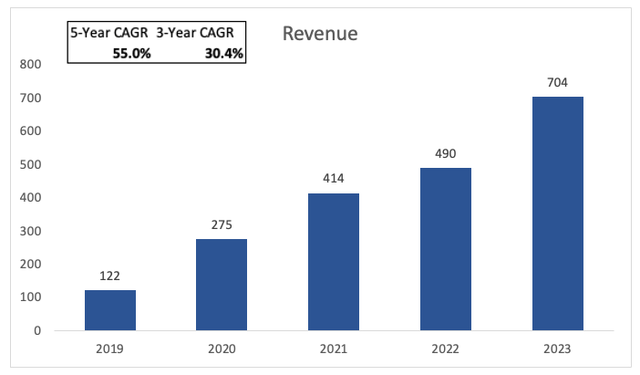

Let’s start from the top. GCT’s top-line growth has been quite impressive I would say. The company went from $122m in FY19 to $704m by the end of 2023. That is a whopping 55% CAGR since it went public. However, in the last 3 years, the growth has taken a slight hit to around 30%. Nevertheless, it is still quite impressive.

Author

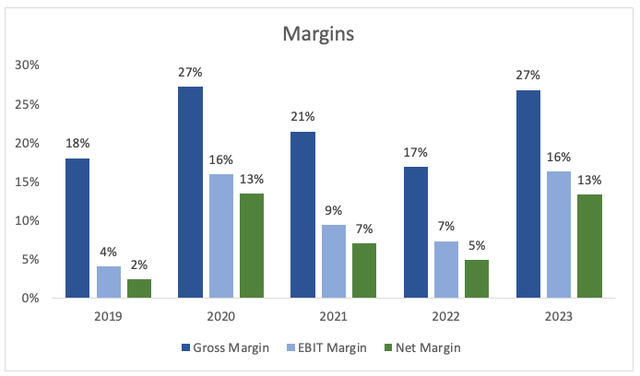

Looking at the company’s margins, we see a vast improvement from FY22 to FY23. It seems that such an improvement in margins across the board can be attributed to the company’s acquisition of Noble House, and general macroeconomic improvements, for instance, lower freight costs due to lower inflation which drove down and going forward it seems that to keep such margin profile, the company has hedged against fuel price uncertainties, as per the transcript, which is a smart decision.

Author

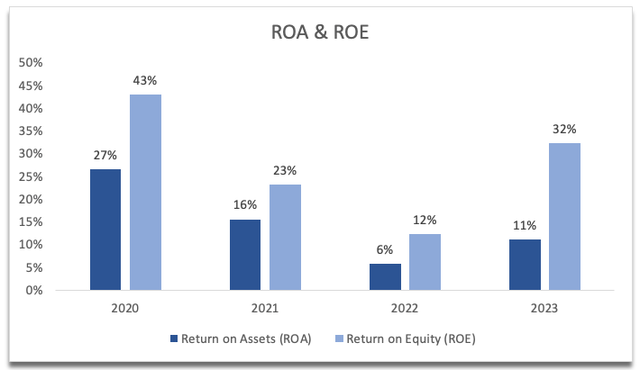

Continuing with efficiency and profitability, we can see a similar situation unfolding in the company’s return on assets and equity, ROA and ROE. FY22 seemed to be the bottom of the operations, and since then the company saw its bottom line improving tremendously, which helped ROA and ROE to almost double also. It seems that the management is very adept at utilizing the company’s assets and shareholder capital, thus creating value.

Author

The next metric I like to look at is the company’s return on total capital, which measures the company’s profitability relative to its total capital. Essentially tells us how efficiently the company uses its available capital, that is debt and equity, to generate profits. I use this metric to tell me whether the company has a competitive advantage and a moat, and usually, I would compare it to its peers, but the company doesn’t provide any peers on their 10K, and I don’t think it would be fair to compare it to the likes of Amazon, Wayfair or Ikea, mainly because the business model isn’t the same and the default peers picked by Seeking Alpha don’t look correct either. Therefore, I will just look at the company’s ROTC alone. I like to see a company at least achieving 10% ROTC to consider it a strong investment. GTC’s latest ROTC figure stood at 14%, according to SA, which is well above the minimum, and tells me that the company is using its assets very efficiently and may have strong pricing power, and efficient control over operating expenses.

In terms of the company’s financial position, as of Q1 ’24, which was filed on May 9th, GCT had $195m in cash and ST investments, against no debt on the books. That is a great position to be in, and as I always say it should help attract investors who dislike leverage. The only interest expense the company has is the finance lease for fulfillment centers in the US, which is easily covered by the company’s interest income on the cash available.

Overall, the company has been doing rather well since going public. Revenues have consistently increased throughout the years, but if we look past the top line, we can see two years of rather bad performance during FY21 and FY22, when efficiency and profitability took a decent hit. However, it seems that the company recovered in FY23 and is ready to keep on performing well in the upcoming quarters as evidenced by Q1 ’24 improvements in gross margins y/y.

Comments on the Outlook

I think the biggest uncertainty of the company’s outlook is the economic uncertainty in the US. Inflation is still very sticky, while interest rates remain elevated. The US economy has been very resilient and that wasn’t what the FED wanted when it started to raise interest rates to combat inflation. However, it seems that everything is starting to go the way the FED wanted, which is to tame inflation, and if it means rising unemployment, so be it. The most recent non-farm payroll report sent shockwaves through the markets as it came in much cooler than expected (114k added vs 180k expected), while the unemployment rate slowly but surely started to climb, and now standing at 4.3% vs 4.1% the month before.

This to me seems like the FED is about ready to cut interest rates, and there is a high probability that the first one will come in September. The markets are thinking it may be too late already and the US will see some sort of a recession with an unemployment rate likely to continue to rise. So, what does that mean for GCT? In short, fewer people are employed, more tightening of budgets, which means no buying of big-ticket items like furniture and sports equipment.

On the other hand, if we are going to see interest rate cuts starting in September, this should help with sales, and stimulate consumer confidence. Home sales may increase due to lower interest rates, which means there will be more demand for furniture. That is as long as the unemployment rate doesn’t go out of hand once again.

The company’s business model of being a fulfillment warehouse is quite attractive and given that it’s quite flexible, the buyers can browse GCT’s warehouses and choose which items to sell through Amazon, Rakuten, Walmart, Wayfair, and Home Depot, or even through their store. So, the company’s products can be sold through a variety of channels, the question is how the overall economic outlook will affect its top-line growth, which has been quite impressive so far. Can it sustain 30%-50% top-line growth going forward? How will its margins look if we are getting into a recessionary period over the next year or so? Let’s have a look at a hypothetical valuation model.

Valuation

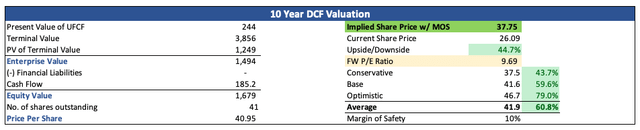

As usual, I will be approaching the valuation model with a conservative mindset. The company is not very well covered in the Street; however, I will be taking the next year of growth at face value. 56% is pretty much given, due to how well the company has performed in Q1, and the upcoming Q2 looks about the same, so around $1.1B in sales is a reasonable assumption. After that, it is hard to estimate, but it is better to be on the conservative end, so I decided to drop the growth rate to around 23% and taper off to around 2% by FY33, giving me a 17% CAGR over the next decade. This is much lower than what the company managed over the last 5 years, which only helps my conservative assumptions in the end.

Author

In terms of margins, I decided to use to lower gross margins to 20% and operating margins to 10% for FY24, which is a decrease of 700bps and 600bps, respectively. Over the next decade, I am assuming the company will return to the same margins it saw at the end of FY23, so I think this is a very conservative outcome for the company.

Author

I am also using a rather high discount rate of 12% to give myself even more room for error in the estimates above, and a 2.5% terminal growth rate because I would like the company to at least match the US long-term inflation goal. Furthermore, I am going to discount the final intrinsic value by another 10% to give myself even more room for error in the estimates. With that said, GCT’s intrinsic value is around $38 a share, which means it is trading below its (conservative) fair value.

Author

Closing Comments

As I covered in the outlook, the biggest risk is the economic uncertainty in the US. If you believe that the company will not see a major drop in its sales over the next years, the company is a buy at these levels. Also, the above valuation which is on the conservative end, gives me some hope that even if the company’s profitability dips, it is still a good deal at these levels. I think 17% CAGR is quite low for a company that has grown at a much faster pace; however, it would be great to hear what the company has to say in the upcoming few quarters. Nevertheless, I opened a small position during this broad market meltdown and will see if I want to add over the next while, especially when the company reports Q2 next week.

It seems that the company is trading at a reasonable price still, even after the run it had since the bottom in March ’23. If I see a meaningful slowdown in the upcoming quarters, I will adjust my model accordingly and decide what I want to do going forward.

Read the full article here