")

Introduction

I “discovered” Globant (NYSE:GLOB) at an investor conference when the stock was in the 50´s. At the time I had difficulty understanding what they did, I asked what digitally native meant and how it generates revenue, whether it is a software company or IT services. Slowly I began to comprehend and then greatly appreciate the company’s market potential and the value it created for clients and investors. Today the financial markets are questioning if Globant and other IT consultants/engineers will be made obsolete by AI or become an integral part of its implementation.

Performance

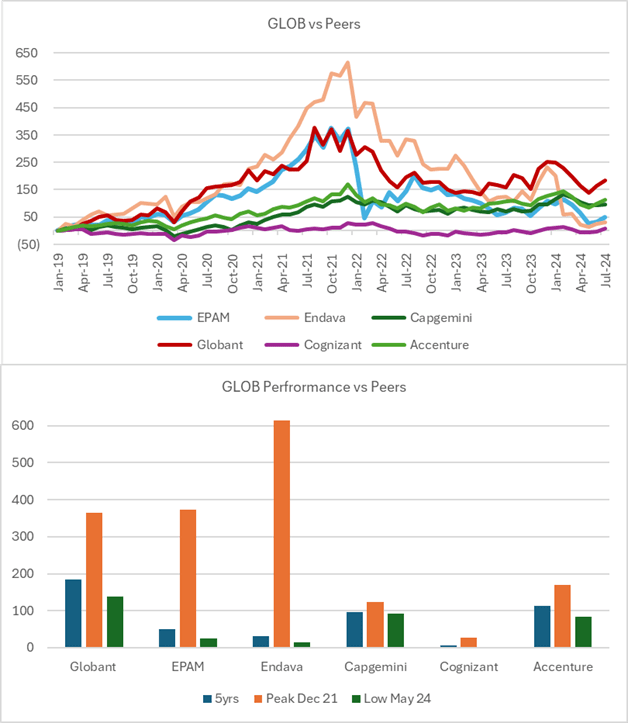

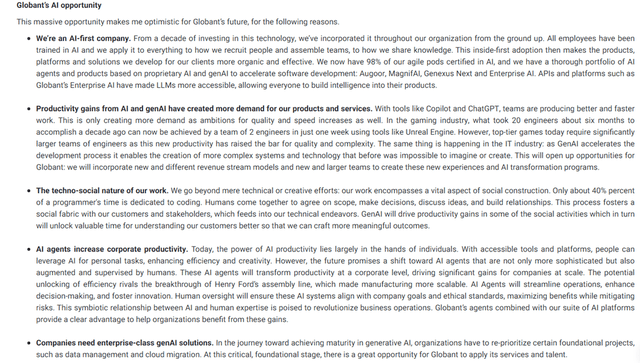

Globant, based out of Argentina, went public in 2014 and has returned over 18x as it grew at over 25% annually through 2019. In the last 5 years, the stock has been very volatile, peaking at US$350 before the start of the rate hike cycle and giving back half those gains on lower valuations and decreased growth. It has performed better than its peers and competitors such as EPAM Systems (EPAM) and Endava (DAVA) which have had revenue and earnings declines.

Created by author with data from Capital IQ

Is AI a Friend or Foe

Since the launch of ChatGPT and the generative AI “revolution” the software and related consultants/IT engineering companies have seen a decline in new business. Across different verticals, companies cited that customers are reassessing their IT strategy, initiatives, and budgets to identify and implement AI across the business (sales and operations). Globant has stated that AI has dramatically improved coding, and software engineering productivity that can reduce costs and increase delivery. However, the fear is that AI may make Globant and companies like it obsolete. The decline in revenue, and new contracts have spoked the market and led to a stock sell-off that may be premature. According to Globant, they see AI as a powerful revenue generator as companies need help and assistance in its implementation.

Globant

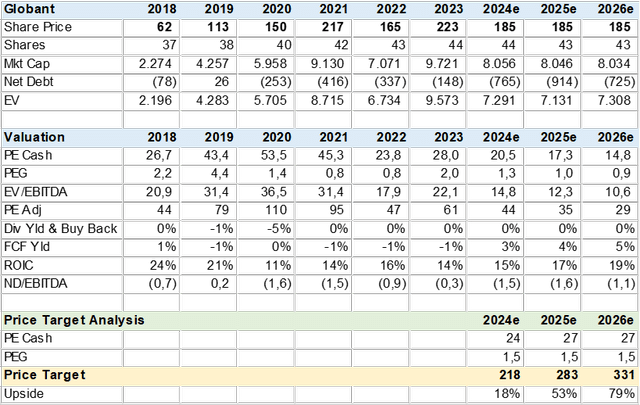

Financial Estimates

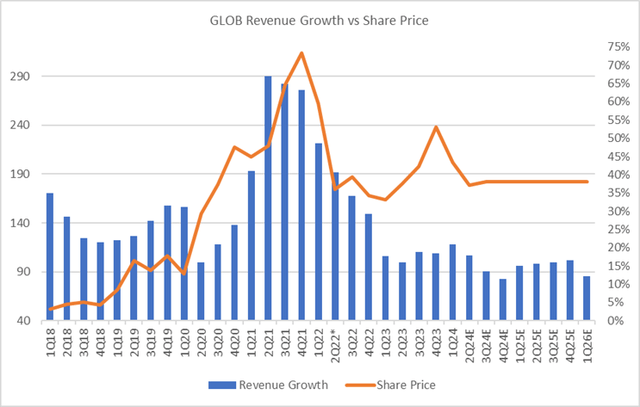

I gathered consensus estimates from 22 analysts to measure the company’s growth and profitability. The market estimates that revenue can grow at over 16% with cash margins of 16% that provide Globant with over US$300m in FCF (free cash flow) in 2025. The company does conduct M&A to boost growth and add new services, in the last 6 years it has spent almost US$1bn without requiring debt, i.e. it has reinvested its FCF. The YE24-26 estimates do not assume M&A and FCF is accumulated in cash or net debt.

The quarter consensus estimates point to a dip in revenue growth from 21% in 1Q24 to 11% by 4Q24e before picking up to a 16% run rate in 2025. If Globant closes new business in the next few quarters that drives revenue higher the market may reprice the AI risk from negative to positive.

Consensus Estimates (Created by author with data from Capital IQ) Consensus Estimates (Created by author with data from Capital IQ)

Valuation

The consensus price target of US$218 backs into an implied P/CE of 24x or a PEG of 1.7x. Note that I use cash earnings to value companies with significant stock-based compensation. Cash earnings = net income depreciation + stock-based compensation. I calculated a year-end 2025 price target of US$283 +53% by using a PEG of 1.5x to the cash earnings growth in the YE25-26 period.

Consensus Valuation (Created by author with data from Capital IQ)

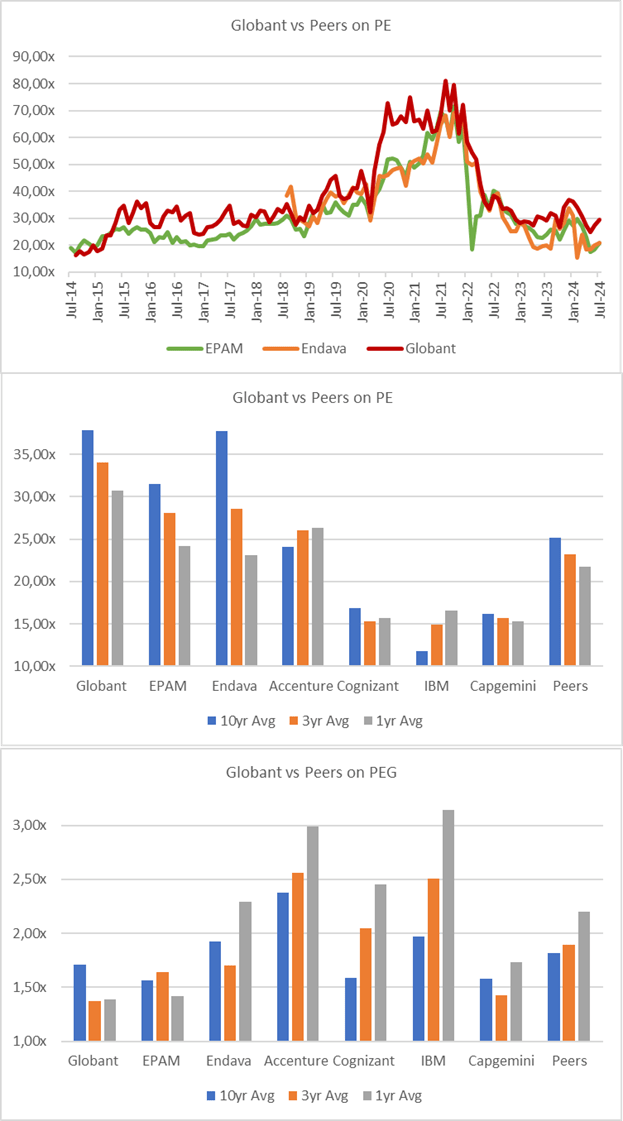

To get a better sense of valuation, I compared Globant’s historical PE vs peers and competitors. As can be seen in the charts below, there was a valuation spike post-pandemic and now the stock is at a back-to-trend. What is interesting is the overvaluation of the larger cap peers such as Accenture (ACN) and International Business Machines (IBM) on a PEG basis. Those companies have significantly lower growth rates, and the market is rewarding them with expensive multiples on the expectations of AI spurred growth.

Historical Valuation (Created by author with data from Capital IQ)

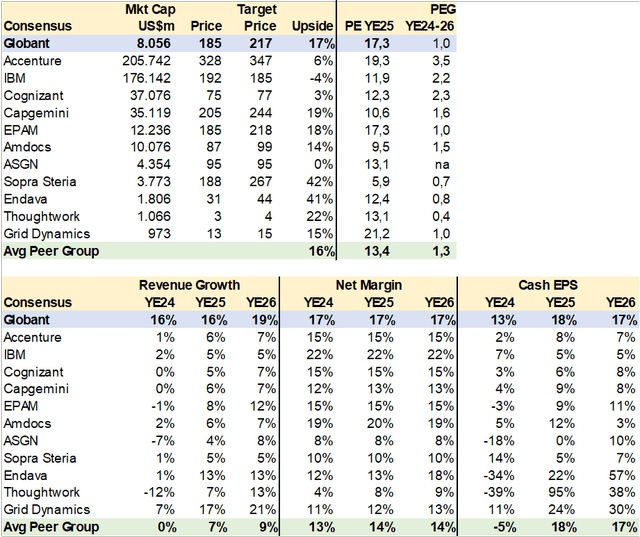

Peer Comps

I compared Globant to its key peers and competitors on consensus valuation and growth metrics. The results, as mentioned earlier, implies that the market “believes” that large-cap IT consultants can accelerate growth driven by AI implementation. However, analyst operating estimates continue to favor Globant as the higher-growth company.

Peer Comps (Created by author with data from Capital IQ)

Risk

The main risk to the Globant investment case is if the customer base can implement and utilize AI without the help of an IT consultant and its army of software engineers. In this scenario, not only does the sector lose out on a new growth market but may become obsolete. A middle ground is that margins get squeezed on added competition, with AI enabling more start-ups to be competitive.

Conclusion

I rate Globant a buy. The company’s track record and vocal AI strategy lead me to believe that it may be able to deliver if not surprise the market on growth and profitability that can spur stock price gains without multiple expansion. Globant can be part of an extended second stage of AI as it helps companies formulate and implement artificial intelligence into company operations.

Read the full article here