")

A lot of stocks are trading at very high premiums right now. The economy is doing great, the stock market is doing great. Finding straightforward value stocks isn’t so easy right now, and we have to look for companies that are in a good position to return value to shareholders, even at higher prices.

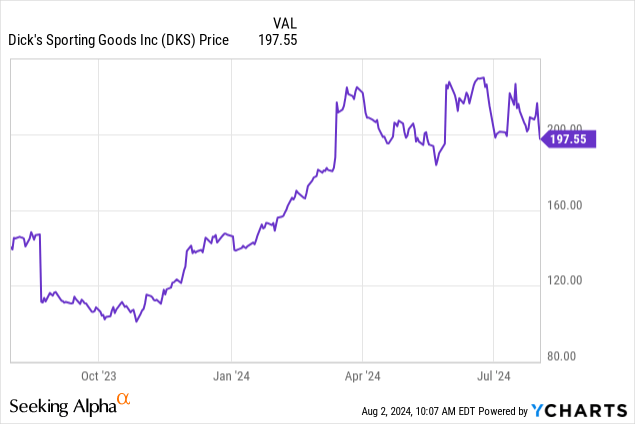

Today we’ll be looking at DICK’S Sporting Goods (NYSE:DKS), a company that is trading well on the north-end of the 52-week range. We’ll be looking at them from a perspective of dividend growth, stock buybacks, and whether the potential return to investors from their strong cash balance is worth paying the high prices the stock is available at right now.

Understanding DICK’S

DICK’S Sporting Goods is a Pennsylvania-based chain of retail sporting goods stores that includes Golf Galaxy and other specialty concept stores. They have around 900 stores overall nationwide.

10-K from SEC

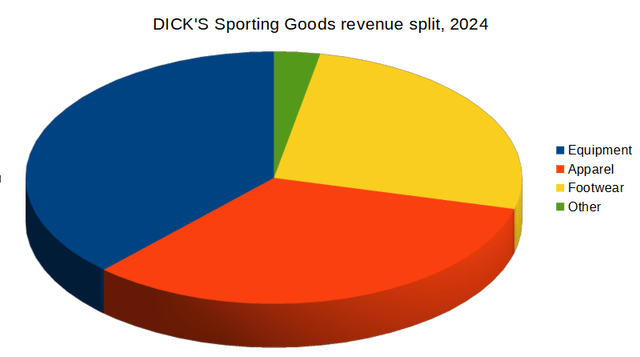

The company sells sports equipment, apparel, footwear and accessories. They sell a lot of brand names, and have their own house brands for various products. The company sells at fairly solid margins which have remained more or less consistent in recent years.

In addition to the ubiquitous DICK’S Sporting Goods stores around the country, the company is pushing some bigger stores called DICK’S House of Sport. There are only a handful of such stores right now, but the company says they intend to grow the number substantially in the next few years.

Balance Sheet

|

Cash and Equivalents |

$1.65 billion |

|

Total Current Assets |

$5.16 billion |

|

Total Assets |

$9.7 billion |

|

Total Current Liabilities |

$3.02 billion |

|

Total Long-Term Liabilities |

$3.99 billion |

|

Total Shareholders’ Equity |

$2.69 billion |

(source: most recent 10-Q from SEC)

DICK’S Sporting Goods has a pretty solid balance sheet, and an appealing amount of cash on hand. After surging prices in recent months, the company is trading at a fairly substantial premium to book value, with a price/book about 6.20. They’re going to have to show a lot of potential for growth and earnings to justify such a premium.

The thing that’s most appealing to me about the balance sheet is the amount of free cash on hand. That’s important for returning value to shareholders, in the form both of a growing dividend yield and potential share buyback programs, which we will cover later.

The Risks

Everything is coming up roses for DICK’S Sporting Goods, but there are still some concerns to look out for going forward.

Sporting goods are an intensely competitive business, and DICK’S has to compete not just with other sporting goods outlets but also regular retailers, online sellers, and potentially most difficultly, vendors who are starting to sell direct to customers, cutting retailers out of the picture entirely.

The inflationary environment is also a difficulty, making product costs unpredictable. Increases in costs could force manufacturers to pass the costs on to retailers, and consumers, which could affect demand.

And that could be very difficult for DICK’S, as changes in demand and shopping patterns are hard to predict, especially when the company has been trying to predict what customers are going to want to buy to stock in nearly 900 stores around the country. That’s always going to be a problem, but so far, DICK’S has been able to handle it.

Statements of Operations – Growing the Business

|

2022 |

2023 |

2024 |

2025 (Q1) |

|

|

Net Sales |

$12.3 billion |

$12.4 billion |

$13.0 billion |

$3.0 billion |

|

Gross Profit |

$4.7 billion |

$4.3 billion |

$4.5 billion |

$1.1 billion |

|

Net Income |

$1.52 billion |

$1.04 billion |

$1.05 billion |

$275 million |

|

Diluted EPS |

$13.87 |

$10.78 |

$12.18 |

$3.30 |

(source: most recent 10-K and 10-Q from SEC)

As you can see, DICK’S Sporting Goods has seen its net sales increase generally in recent years, and estimates are that this is going to continue, with $13.24 billion expected in the current fiscal year, $13.8 billion in 2026, and $14.5 billion in 2027. That is a strong level of growth for a company that is already the biggest sporting goods chain in the United States.

Profits will be growing too, per estimates, with EPS at $13.73, $14.72 and $15.80, respectively. This puts the P/E ratio of the current company at around 14.42. That’s not a bad ratio when one considers the stock is trading at such a premium to its book value.

Later this month, DICK’S will announce its second quarter earnings release, which is estimated at $3.42 billion and an earnings per share of $3.78. The company has been pretty spot on in making good on these estimates, though the earnings surprises have been positive in recent quarters, so there is room for them to beat this time.

Returning Value to Shareholders

In the calendar year 2023, DICK’S Sporting Goods repurchased 5.4 million shares at a cost of $648.6 million. That’s $120 a share, quite a premium to pay for the company, though quite a bit cheaper than where it trades now. That shows some strong confidence in the company going forward. There is a remaining authorization of $779.6 million, though it is doubtful any repurchases will take place while the stock is trading in its current range.

The once place where DICK’s could really improve return is dividends. They currently pay $1.10 per quarter, which is a yield of about 2.2%. That is an increase from $1.00 per quarter the prior year. With $1.65 billion in the bank and earnings growing like they have been, they can certainly afford to increase the payout going forward, which makes this a potential dividend growth pick.

Conclusion

I really like DICK’S Sporting Goods, they have become an impressive market leader in the sporting goods market and are strongly profitable. The company has a good cash position and is able to start growing dividends at a consistent rate if they so choose.

The one downside to the stock that I see is that it is trading so far above its 52-week lows. They have pulled back a bit off their highs, but the stock is still trading at a rich premium, which I see as the difference between a buy and a hold. Right now, I’m looking at hold.

But like I say, I really like DICK’S, and I’ll be keeping a close eye on the stock with a hope that it will fall into a more friendly buyer’s range. Below $150 per share, I will start to be very interested.

Read the full article here

")

")