")

")

Shares of the Everest Group (NYSE:EG) are up moderately over the past year, though they have largely been rangebound between $360 and $400, even as the company has benefitted from a quiet catastrophe environment. I last covered Everest Group in May, rating shares a hold, as I needed to see more evidence of underwriting progress. Since that article, the stock is up 4%, lagging the market’s 7% gain. In a benign hurricane season, I saw upside to $400, which we are now approaching as we enter the heart of hurricane season. I remain cautious on shares.

Seeking Alpha

Q2 earnings were seasonally strong

In the company’s second quarter, Everest earned $16.85, beating consensus by $0.21. It grew gross premiums by 13% to $4.7 billion, with a skew towards reinsurance. Last year, the company issued equity to facilitate its growth, which remains a capital allocation decision that I am not enthusiastic about. In particular, we are still not, in my view, seeing Everest deliver on the underwriting results it is aiming for.

Now, when looking at results, it is also important to note that EG has seasonality in its earnings because it faces hurricane risk. These catastrophe losses are focused largely in Q3 and can carry into Q4. There is limited risk here in H1. As such, we should see the company generate more earnings in H1 than H2, which is something to be mindful of. Over an entire year, Everest targets an 89-91% combined ratio with 6% catastrophe losses.

In the company’s second quarter, Everest had a 90.3% overall combined ratio, resulting in $358 million in underwriting profits. Now, this was in line with the midpoint of its targeted range. However, as noted, cat losses are lighter in H1. During Q2, EG had $135 million of pre-tax catastrophe losses. This was up from the incredibly light $27 million last year, but it still resulted in a cat load of 3.3%.

Essentially, EG was able to meet its target only because cat losses were half of its anticipated full-year level. At a normal cat ratio, its combined ratio would be closer to 93%. Now, of course, for the full year, cat losses may come in below 6% and boost profits. At this point, it is difficult to know because it depends on what happens with hurricane season.

I do not view Q2 cat results as being inconsistent with a 6% full-year result, given how most of the losses occur during a 3-month span. Now, management also focuses on its “attritional combined ratio,” which was 86.6%. It defines attritional as excluding catastrophes, one-time items, and prior year developments. Again, with an average cat load of 6%, we need to see this running closer to 84% for EG to hit its target.

Reinsurance Delivered Solid Results

Drilling deeper into results, we are seeing a bifurcation in results by division. Its reinsurance unit is performing better. Everest is growing this unit more quickly as gross premiums rose 16.5% to $3.2 billion. While this unit does drive greater profitability, it does have more catastrophe risk, which can be more volatile and receive a lower earnings multiple by investors as a result.

This unit earned a $303 million underwriting profit, accounting for about 85% of total underwriting profits. It had an 88.9% actual combined ratio and an “attritional” combined ratio of 84.4%, 30bps better than last year. Again, this unit’s performance ultimately comes down to how it performs during hurricane season, but Q2 results were solid.

Insurance underperformance continues

On the other hand, its insurance unit continues to deliver subpar results. In insurance, gross premiums rose by 6% to $1.5 billion, and it delivered just a $54 million underwriting profit. Management said it is seeing pricing exceed losses, but its combined ratio remains high at 94.4%. In Q2, it had a 92.8% attritional combined ratio. This remains well above target.

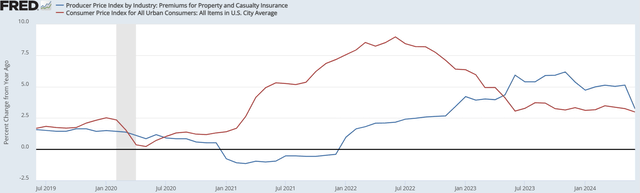

Disappointingly, it was also 0.2% higher than a year ago. That is a surprising performance, given it remains a very healthy environment for underwriting, which is why we are seeing other insurers like Arch Capital (ACGL) and Chubb (CB) report strong results. In 2021/2022, insurer profits were squeezed by inflation rising faster than premiums. Given insurance contracts are 6-12 months, it takes time for them to adjust for higher inflation.

St. Louis Federal Reserve

As insurers have raised prices over the past year, it has been a prime opportunity for them to recapture lost margin during the pandemic, an opportunity that Everest has largely missed based on Q2’s results. Additionally, the gap between premiums and inflation has narrowed since we passed the June 2023 repricing. While there remains a modest gap, I view this as more likely to allow the industry to retain current margins rather than materially exceed them. Ultimately, this leaves me skeptical Everest can generate sufficient underwriting gains to meet its profitability targets in an average catastrophe environment.

Higher rates are benefiting investment income

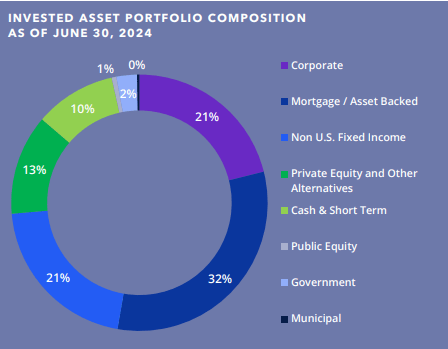

While its underwriting results lag, its investment portfolio has picked up the slack, as Everest is a prime beneficiary of higher rates. Its $528 million of Q2 investment income was a record and up from $357 million last year. It has a $39.1 billion portfolio. It is diversified across sectors and had an AA- average quality, which should minimize potential credit losses.

Everest Group

This portfolio has a 3.4-year average duration, meaning it takes some time for the portfolio to roll over and for changes in interest rates to shift investment income. Even if the Federal Reserve begins cutting rates in September as I expect, it will likely see maturing bonds have lower yields than market levels for at least another 12 months. As such, I expect net investment income to continue to grow, albeit at a declining pace.

Potential Upside Catalysts are unclear

Back in May, I was looking for $53-56 in 2024 earnings, though I viewed the run-rate as closer to $51-53. So far, the company has generated $33 in H1 earnings, which should be about ~60% of a normal year’s earnings for about $55 in 2024 earnings. Now at a normal cat load, EG would have to face another ~$2.40 in losses, which is why I would not annualize Q2 EPS. After these results, I still see the company generating about $55 in 2024 EPS, assuming a normal catastrophe environment.

From a purely tactical perspective, investors also need to consider whether now is a good time to buy a cat-exposed reinsurer. Over the next two months, the magnitude of the US hurricane season is likely to be the primary driver of share price performance. Weather is inherently unpredictable, and it is impossible to know where and when storms will land. In my view, shares are already discounting a quieter season, and so I see greater downside risk from a more damaging storm than upside risk from a quiet season.

Shares may stay “cheap”

At ~7.2x earnings, EG is not an expensive stock, but with so much of its earnings tied to Q3 storms and underlying insurance results continuing to disappoint, I struggle to see the case for much multiple expansion. Indeed, with growth faster in reinsurance, the business is becoming less diversified and potentially more cat-exposed. I continue to view its $349 book value, excluding unrealized gains and losses, as a reasonable floor, but absent a very mild hurricane season, I do not see a catalyst for further appreciation, especially as we move further into a rate cutting cycle.

While not as cheap, ACGL and CB trade below 12x with much superior underwriting momentum and less volatile earnings. Sometimes, it can be better to invest in a less-cheap stock of a better performing company than in the most-cheap stock in a sector. I continue to view that as the case here. For long-term investors, I do not see a need to sell at this multiple, but with hurricane risk and weak insurance underwriting, I do see a case to tactically sell and revisit after the summer. I would want shares to trade closer to book value before being a buyer.

Read the full article here

")

")