")

Q2 2025 Earnings Call Transcript")

A strong case for an eventual rate reduction was developing ahead of the Federal Reserve’s (“Fed”) July Federal Open Market Committee (“FOMC”) meeting. According to CME’s FedWatch Tool, the likelihood of a rate cut this September prior to today’s meeting was approximately 90%, driven by declining inflation and a softening labor market.

Accordingly, the primary question was not whether the Fed would signal a rate cut at today’s meeting, but how explicitly they would communicate this expectation. And on this, the policy statement from the meeting is supportive of a lower rate environment in the months ahead. Here’s what else you need to know about the July Fed meeting.

What Did The Fed’s July Policy Statement Say?

In the policy statement from the rate-setting committee, Fed officials decided to keep the benchmark lending rate at its current mark of between 5.25% and 5.50%. This was widely expected prior to the release. Of more important note were the details within the policy statement.

In their June statement, the FOMC noted that “job gains have remained strong and the unemployment rate has remained low.” In their current statement, the committee acknowledged the more moderated market, saying “Job gains have moderated, and the unemployment rate has moved up but remains low.”

With regards to inflation, the wording in the statement was more subtle. Though the committee still sees inflation as an issue, they see it only as “somewhat elevated” compared to “elevated” in their last policy release.

Likewise, the committee used less emphasis in their statement with regards to risk factors relating to inflation. For example, instead of saying that they remain “highly attentive to inflation risks,” the committee stated that they are “attentive to the risks to both sides of its dual mandate.” In my view, the “both sides of its dual mandate,” comment is noteworthy, as it may indicate policymakers are becoming more concerned about the labor market, given the rising joblessness in recent months.

What may come off as a disappointment to those seeking clearer direction is the lack of change in the second half of the statement. The release still noted that the committee “does not expect it will be appropriate to reduce the target range until it has gained greater confidence that inflation is moving sustainably toward 2 percent.” This is unchanged from their last remarks. While this is worth noting, I don’t believe it offsets the more notable updates made to the first half of the statement.

Market Reaction To July Fed Meeting

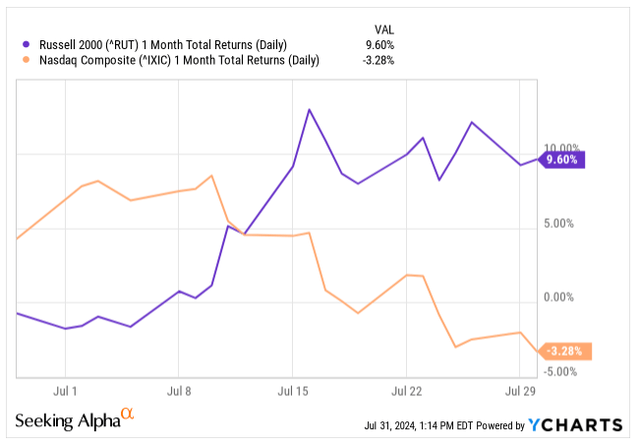

Heading into the release, equity markets were in the midst of a significant rotation away from the tech stocks that have powered indexes to multiple record highs throughout the year. This has been fueled in part by rising sentiment in the Russell 2000 index (IWM), an index of smaller companies that likely would benefit from a lower rate environment.

YCharts – 1MTH Returns Of Russell 2000 Index Compared To Nasdaq Composite

On Tuesday, the Nasdaq Composite (NDX) and the S&P 500 (SPX) both ended the day lower on continued weakness in shares of Nvidia (NVDA). This compares to the Dow Jones Industrial Average (DJIA), which rose 200 points on the day.

Ahead of the rate decision and commentary, however, markets rallied higher, with the DJIA up nearly 230 points before the release and the NDX up over 400 points, reversing losses from the day prior. The momentum carried into the afternoon session following the announcement. In the bond markets, the yield on 10-year U.S. Treasuries further slipped to 4.113% after ending the day at 4.143% on Tuesday.

In my view, markets are likely to be buoyed higher on continued optimism over a looser policy environment in the months ahead. Additionally, I expect shares of smaller companies in the Russell 2000 index to continue benefitting at the expense of their larger-sized tech peers.

Why Does The July Fed Meeting Matter?

Though observers did not expect the Fed to change its benchmark rate today, the decision and subsequent commentary were crucial in gauging the Fed’s readiness and willingness to cut interest rates in the near future.

Recent data showing cooling inflation and a softening labor market have strengthened the case for a rate reduction. Today’s meeting likely clarified the Fed’s approach to balancing the risks of cutting rates too soon versus waiting too long.

In my view, the two-day meeting conveyed a positive tact among policymakers to lean towards cutting rates sooner than later, aiming to achieve the elusive soft landing that officials have sought since the start of their rate hike campaign

Will The Fed Reduce Interest Rates This Year?

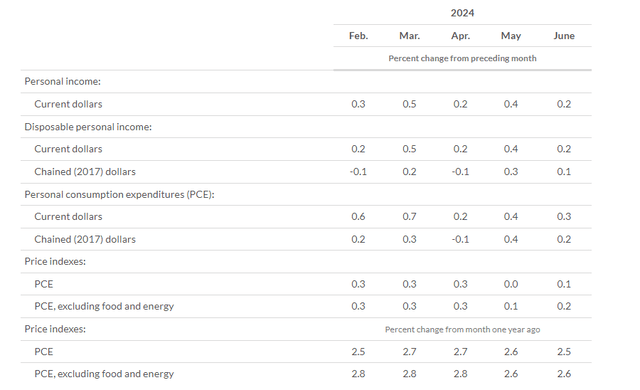

Recent data on inflation and the labor market could support the Fed’s readiness to lower rates in the coming months. In June, the Fed’s preferred inflation gauge, the Personal Consumption Expenditures (“PCE”) index, rose 2.5%, a continuation of the cooling trend from the previous month’s 2.5% reading.

BLS – PCE Summary For June 2024

In recognition of the positive trend seen in the PCE, Chicago Fed President Austan Goolsbee noted in early July that the current benchmark range was set when inflation readings were over 4%, suggesting that rates should remain restrictive only as long as necessary.

With inflation now in the 2.5% range, Goolsbee likely believes rates are sufficiently tightened. Although he is not a voting member of the committee this year, his views could influence more hawkish officials.

For example, San Francisco Fed President Mary Daly, a voting member, recently acknowledged the positive inflation trend but emphasized that price stability has not yet been achieved, and more confidence is needed to ensure a sustainable path forward.

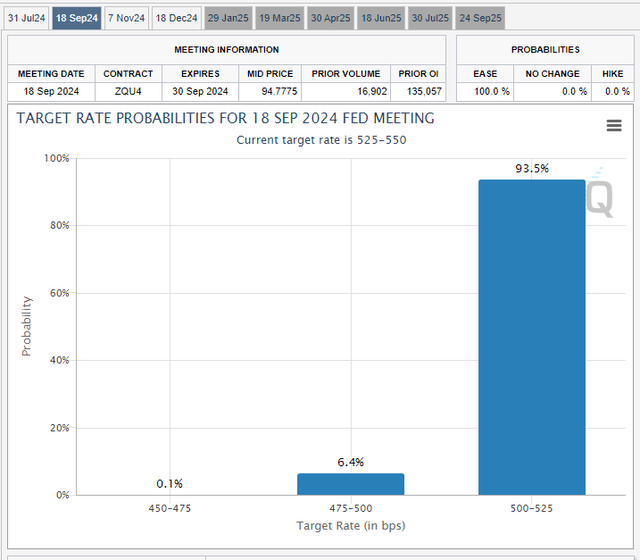

The two officials likely have more refined perspectives today. The policy statement and the initial commentary from Chairman Powell indicate greater likelihood of lower rates in the coming months. This aligns with the views of interest rate observers, who now see an over 90% chance of a rate reduction in September, according to the CME FedWatch Tool.

CMEFedWatch Tool – Target Rate Probabilities For September FOMC Meeting

The Bottom Line

There were two near certainties heading into the two-day July FOMC meeting. First, it was widely expected that the policy statement would show no change in benchmark rates, and today’s meeting confirmed this expectation. Second, though rates were expected to remain steady in July, observers have assessed an over 90% chance of a rate reduction in September. The FOMC meeting today was anticipated to reinforce these expectations.

The policy statement and subsequent commentary appeared to make good on expectations heading into the decision. This potential shift is supported by recent trends in inflation and the labor market, which suggest that the economy may be cooling sufficiently to warrant easing monetary policy.

Today’s policy statement also seemed to reflect growing awareness of the slowing conditions in the labor market. This shift was evident in the change from the June policy statement, where the committee emphasized being “highly attentive to inflation risks,” to the current language, which states that they are “attentive to the risks to both sides of its dual mandate.” This revised phrasing suggests a broader focus that now includes considerations beyond just inflation, possibly in response to recent labor market developments.

Given these developments, it seems likely that the FOMC will move towards a rate reduction in September, aligning with market expectations.

Read the full article here

")

Q2 2025 Earnings Call Transcript")

")

")