")

")

")

Investment Thesis

On July 30, Powell Industries (NASDAQ:NASDAQ:POWL) presented Q3 2024 results, which drastically beat all expectations and caused a 24% reaction in the aftermarket.

The company has a great business model that benefits from multiple macroeconomic trends, it’s also immune to the so-called “Trump-trade”, however, the market has already efficiently priced in the results at the current price of $165, according to my valuation model, therefore I think that at this price is better to hold and look closely at a possible price correction.

Seeking Alpha Stock Price

Industrial Business, But A High-Quality One

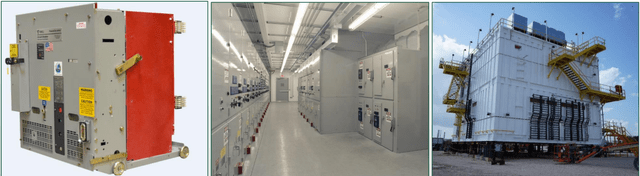

Powell Industries is dedicated to the manufacturing of electrical power distribution systems, such as circuit breakers, distribution panels and control systems. These systems are complex to implement and are sometimes custom made for the client.

Furthermore, Powell’s work doesn’t end after delivering the product, as it’s also often involved in additional services, as indicated in the annual report:

We assist customers by providing field service inspection, installation, commissioning, modification, and repair services, as well as spare parts, retrofit and retrofill components for existing systems, and replacement circuit breakers for obsolete switchgear no longer produced by the original manufacturer.

This way, long-term relationships are established, predictability is added to revenue and the company has a business vertical that typically has higher margins (services and spare parts).

Powell Industries Investor Presentation

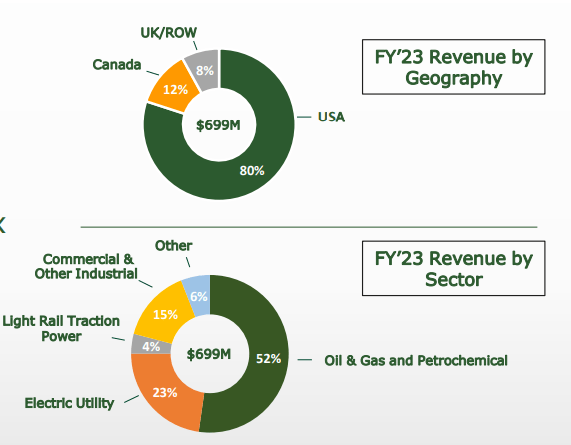

This sector has tailwinds thanks to the growing demand for renewable energy sources, such as solar and wind, which require energy distribution, control and even storage systems. It must also be considered that many electrical networks are in the process of modernization to improve their efficiency, since in the United States there’s infrastructure that is up to 50-years old.

A curious fact for the near term is that 92% of sales come from North America and practically all of them come from traditional energy industries such as Oil & Gas or Electricity. This makes the company immune to the so-called “Trump-trade” and would benefit from a more friendly policy with non-renewable energies and tariffs on Asian countries.

Powell Industries Investor Presentation

Q3 2024 Earnings Report

On July 30 at the market close, Powell presented its Q3 2024 results, which completely crushed. The expected revenue was $222 million for the quarter, while the company presented $288 million, that is, a year-over-year growth of 50% and an expectation beat of 30%.

This was already good enough, but the company also considerably improved its margins, starting with the gross margin which was 28% compared to 22% the previous year or 24% in the Q2 2024. This’s why, at the time of writing this, the stock is rising 24% in aftermarket (well deserved).

| Estimated | Reported | Beat/Miss | |

| Revenue | $222M | $288M | 30% |

| EBIT | $30.5M | $57.29M | 90% |

| EPS | $2.16 | $3.79 | 75% |

Author’s Compilation

This growth was derived from strength in the non-renewable energy industries. In the Oil & Gas sector the growth was 56% and the Petrochemical sector grew 158%, which wasn’t expected at all. While the company doesn’t give any details of what exactly this increase in demand is due to, what’s clear is that the traditional energy industry is beginning to feel comfortable enough to invest heavily, perhaps, due to what was previously mentioned about the Trump effect, but these are my speculations.

Valuation

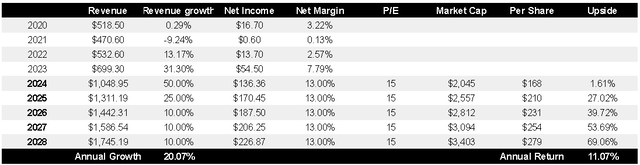

The complicated part for me comes with valuation. The outlook given by the CFO is to continue with a strong Q4 to close the year, so I’ll take this into account for my estimates.

Looking forward, we remain encouraged with where Powell is positioned as we enter the last quarter of fiscal 2024. Commercial activity remains strong, providing a tailwind as we close out the year and prepare for fiscal 2025.

-Michael Metcalf, CFO.

During the three quarters of FY2024, revenue grew on average 50% year over year, so it seems reasonable to think that in Q4 2024 growth will be around that 45-50% YoY. Following the same reasoning, the net margin could be around 13-14% for the remainder of the year.

The tricky part comes when you try to estimate beyond this fiscal year, as it’s not clear to me that growth or margins are sustainable if we take into account the last 10 years, which have been quite volatile. For my estimation, I will assume that next year is also good, thanks to the arrival of Trump, growing 25% YoY and in subsequent years the growth moderates to 10%. The profit margins would be maintained (I find it complicated) and the P/E would be 15 times.

Dividing the Market Cap by the 12.2 million shares outstanding and taking the entry price of $165 USD (current aftermarket price) any good scenario appears to be already discounted in current price.

Author’s Compilation

Risks

The main risk that I see is that in recent years the financial performance has been somewhat volatile and it isn’t clear to me if we’re facing a possible cycle peak and therefore we’re buying high. If margins return to previous levels (average 4%) it’s clear to me that this would be the case.

Furthermore, assuming that the world continues to turn towards renewable energies and stop using traditional ones, the company’s revenue would be affected in the long run because its main Oil & Gas clients would possibly stop investing in new projects.

The Bottom Line

Although the business is really good and has many tailwinds to continue growing in the future, it’s clear that no one expected that the Q3 results would continue along the same lines as Q1 and Q2, otherwise the market wouldn’t have reacted in this way.

At the price of $165, it seems to me that growth is more than discounted and the opportunity was when the stock was trading at $133. In fact, with the same estimates shown above, but with a price of $133, the potential return would be 15% per year, which would seem like a buying opportunity to me. So, that said, I think that the company is currently a hold, but if it went down to around $135 per share I would definitely buy.

Read the full article here

")

")

")