")

")

National Bank of Canada’s Business

The National Bank of Canada (TSX:NA:CA) is the 6th largest bank in Canada by assets and a systemically important financial institution. Its presence is mainly in the provinces of Quebec and Ontario, while it does have expansion plans into the Western half of Canada (more on that later). It has 4 business segments: personal & commercial banking, wealth management, and U.S. Specialty Finance and International. Here’s a bit about its business segments:

Personal & Commercial – this segment has 2.7 million individuals and 147,000 businesses in Canada as clients. The bank has 368 branches and 944 ATMs serving it customers. It had $4,516 million CAD in total revenues, $2,006 million in income before provisions for credit losses and taxes, and $1,282 in net income in 2023.

Wealth Management – this segment is a leader in providing wealth management services in Quebec. It has over 800 advisors and 100 service points across Canada, providing portfolio management, financial and succession planning, and insurance services. It had total revenue of $2,521 million CAD in 2023, of which 57% was fee-based, 31% was net interest income, and 12% was transaction-based.

Financial Markets – this segment is a leader in Canada in risk management solutions, structured products, and market making in ETFs for fixed income, currencies, equities, and commodities. It also provides corporate banking, capital markets and advisory services, as well as loan origination & syndication, M&A, and corporate financing. It had total revenue of $2,656 million CAD, $1,495 million CAD in income before provisions for credit losses and income taxes, and $1,055 million CAD in net income.

US Specialty Finance & International – National Bank’s subsidiary called “Credigy” offers specialty finance in the US, and its subsidiary ABA Bank offers personal and commercial banking in Cambodia. Combined together in 2023 they had total revenues of $1,209 million CAD, income before provisions for credit losses and income taxes of $809 million CAD, and net income of $550 million CAD.

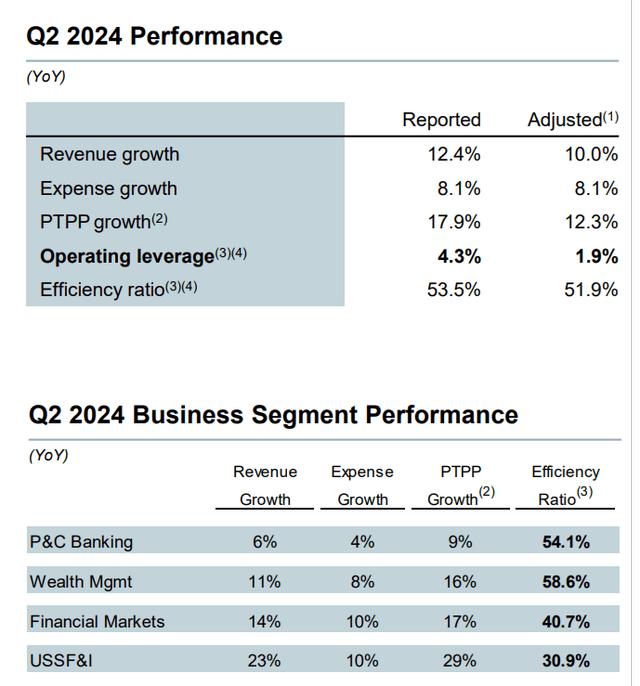

It has recently been posting strong financial results; revenues growing at a faster rate than expenses, and strong efficiency ratios. Loan growth and deposit growth have been robust too:

Q2 2024 National Bank Conference Call Presentation

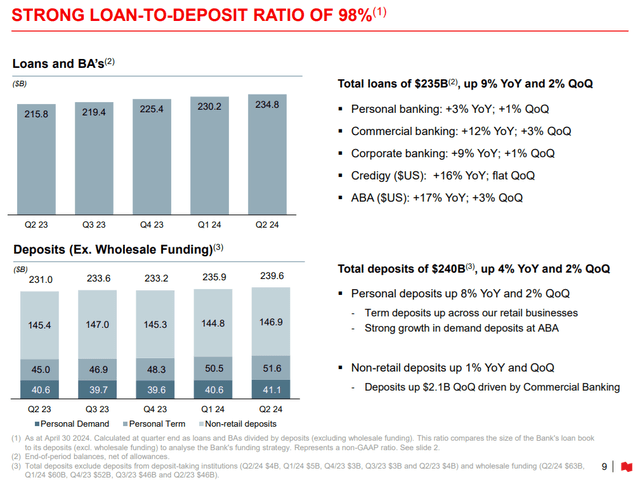

National Bank of Canada currently has a rather high loan to deposit ratio of 98%:

Q2 2024 National Bank Conference Call Presentation

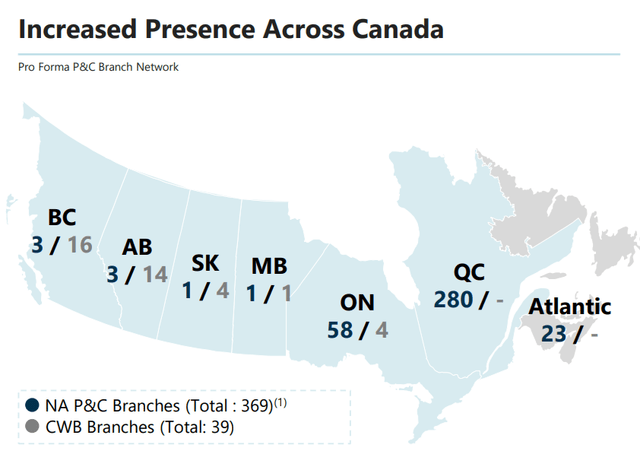

National Bank of Canada recently announced a deal to acquire Canadian Western Bank (OTCPK:CBWBF). I think the main reason for this deal was it presented a way for National Bank of Canada to quickly expand to two large Canadian provinces without having to muscle in their way by directly competing with incumbents. Indeed, Canadian Western Bank’s geographical footprint by physical branch locations is almost exactly complementary with National Bank of Canada’s footprint:

June 2024 National Bank of Canada Presentation

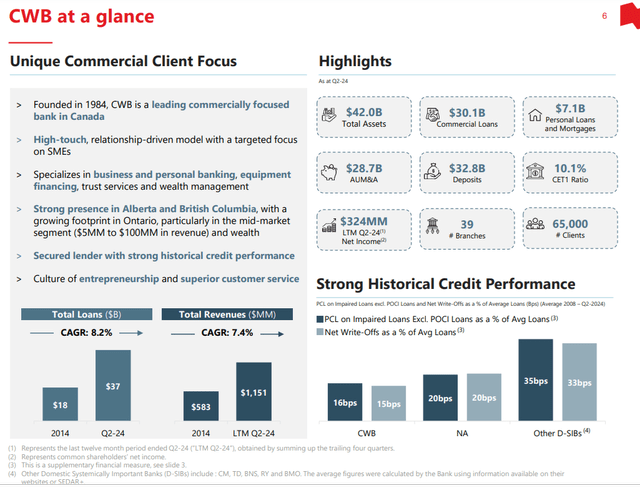

Canadian Western Bank is about 1/10th the size of National Bank of Canada by total assets, and about 1/20 the size by market capitalization just before the deal was announced. Canadian Western Bank has a very pronounced leaning towards commercial loans, and is also well capitalized with a 10.1% CET1 ratio. Prior to the acquisition deal, Canadian Western Bank was growing at a healthy clip of about 7 – 8% CAGR for the 2014 – 2024 period, and had a lower average rate of provisions for credit losses than National Bank of Canada:

National Bank of Canada June 2024 Presentation

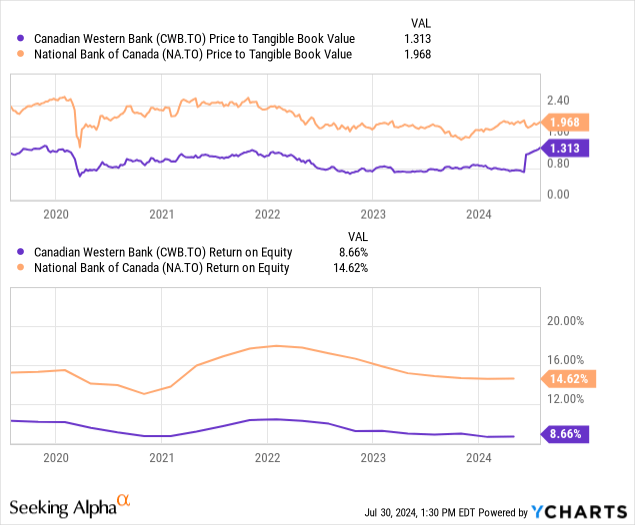

National Bank of Canada is set to pay a premium of 110% over the closing price of Canadian Western Bank just prior to the announcement of the deal. Going into the deal, Canadian Western Bank was trading at a large (~20%) discount to its tangible book value, which I believe is because it consistently earned a relatively low return on equity because of its relatively lower balance sheet leverage:

It might seem that National Bank is overpaying; however, the purchase price is actually roughly equal to Canadian Western Bank’s book value. In all, it’s a quick way for Canadian Western Bank’s shareholders to realize the book value of their shares, and a quick way to jump start National Bank’s growth. The transaction is a shares-for-shares deal, where each share of Canadian Western Bank is equal to 0.450 shares of National Bank of Canada. The deal is still pending regulatory approval, and is set to close at the end of 2025.

Compounder Over Time

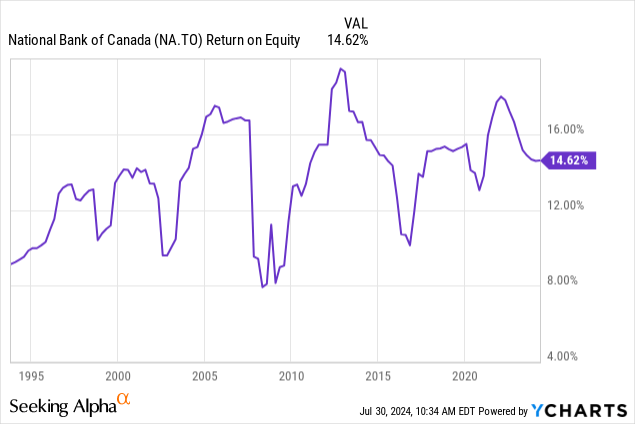

As I’ve said before elsewhere, the Canadian banking sector is an oligopoly, where National Bank of Canada is occasionally included as an oligopolist (Big 6 as opposed to the Big 5). This, as well as more stringent regulation, has meant that Canadian banks are safer and more stable than the American counterparts across the border. National Bank of Canada is no exception to this. Below is a graph of its return on equity since 1994. If we smooth out all of the short-term gyrations in this number, the long-term average return on equity at National Bank of Canada is about 14%:

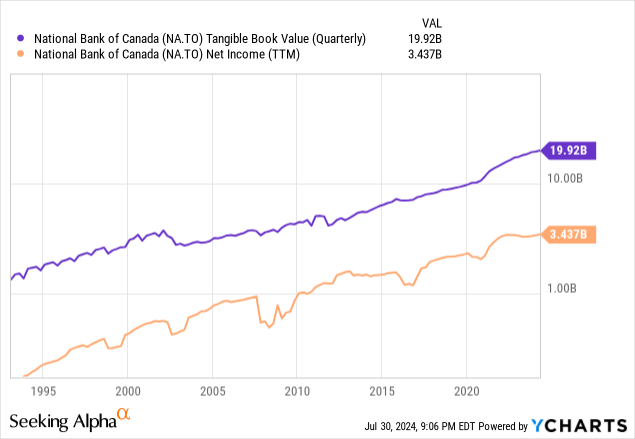

The next chart to my mind seals the deal: it plots tangible book value and net income. Notice that they are nearly straight lines on a logarithmic plot, which means that they are nearly perfect exponential growth trends. This suggests that National Bank of Canada has a long history of retaining earnings to grow its shareholder equity. If you want to get a bit more technical, the negative of the vertical gap between the two lines actually represents the return on tangible equity.

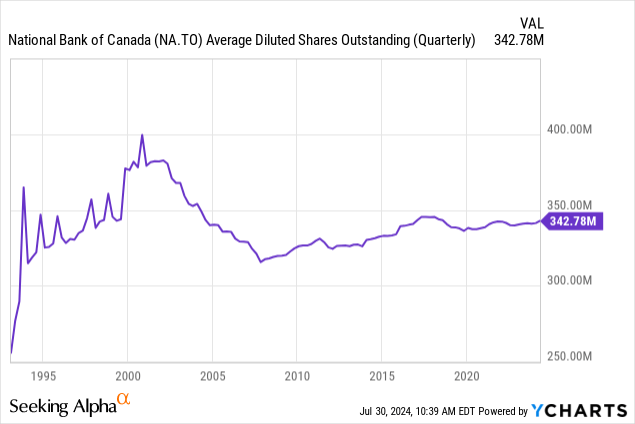

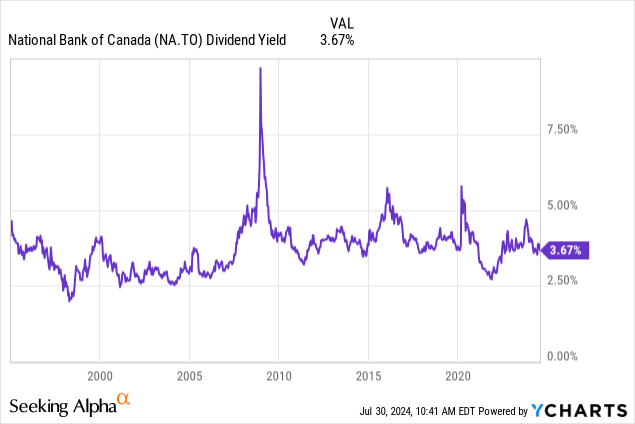

The approximate slope of the two lines above corresponds to roughly the pace of share price increase over time, which is about 10%. Adding together the rate of share price increases with the historical average dividend yield of ~3.5% approximately produces the long-term average return on equity of 14%. During this time, the share count fluctuated around a long-term average of ~350 million shares, suggesting that National Bank of Canada has tended to decrease its share count just as much as its activities increase it:

Simply put, National Bank of Canada has a historically proven high quality business model that is not intrinsically reliant on mergers & acquisitions to grow. It has a long track record of compound growth of its equity by reinvesting retained earnings, and as a result, it is very suitable for a long-term buy-and-hold investment. It has a decent dividend yield, which is a sweetener for the more income-oriented investors.

This is the past – however, what about the future? The beautiful thing about banking and capital markets businesses is that its business is timeless: technological advances may change the means by which banks do business, but the business of depositing, borrowing, and raising money is forever the same. The financial business model is simply non-disruptable. Combined with the fact that National Bank of Canada is one of the players in a highly regulated oligopoly, I have full confidence that the bank’s past will be a mirror for its future. However, it is facing some short term economic headwinds in Canada, which I will talk about next.

Short-Term Canadian Economic Headwinds

The Canadian economy is currently facing economic headwinds caused by rising interest rates and household indebtedness. In the short run this may be a source of risk to National Bank of Canada, and I want to unpack this a bit more.

The Canadian household is among the most indebted in the world, with a debt to GDP ratio of 107% as of May 2023, where about 3/4 of this debt is attributable to housing mortgages. This means that Canadian household finances are especially sensitive to interest rate movements, due to a quirk of how Canadian mortgages work. A “fixed rate” mortgage in Canada actually resets its rate every 5 years according to the prevailing market interest rates. This means that across the population of Canadian mortgagees, their rates are reset cohort by cohort.

A recent article had the following warning:

By 2026, Canadians who renew their mortgages that previously had variable-rate mortgages with fixed payments will see the largest increase compared to their previous mortgage’s origination, expected to rise 61.85%.

Payments are expected to increase by 31.88% among all types of mortgages by 2026. Those who will be hit with the softest increase are Canadians who previously held fixed-rate mortgages with a term of less than five years, who will see an increase of 19.26% by 2026.

Those who will be hit the hardest are homeowners who took out a mortgage between Apr. 1, 2020, and Mar. 1, 2022, when Canada’s prime interest rate was 2.45%. It is currently at 7.2%.

Another recent article displayed various opinion polls showing that Canadians are under financial stress due to the higher interest rates:

65% of Canadians said high interest rates have negatively impacted their household finances…

… almost half of those polled, 47%, said that even if interest rates declined, they’d still be concerned with their ability to repay their debts, 34% said they are so indebted that lower interest rates would offer little relief…

… 32% said they would incur further debt to cover living expenses in the next year. An almost equal 31% regret the amount of debt they’ve taken on in life…

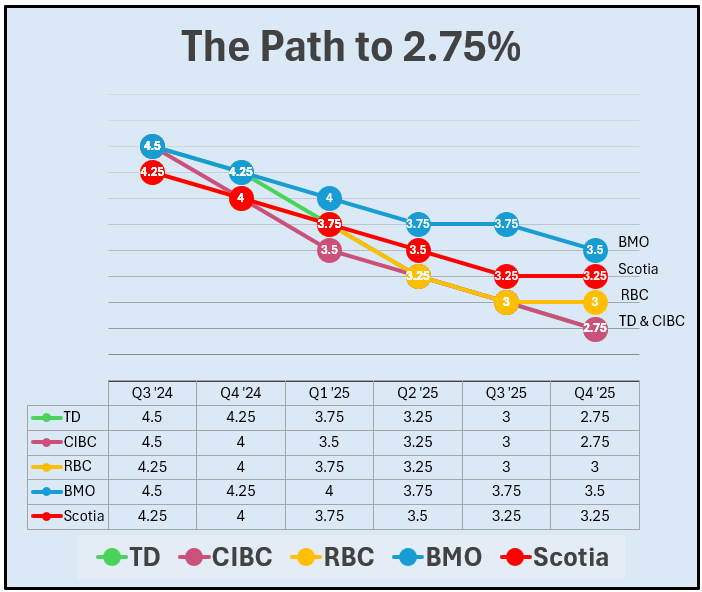

Thankfully, rate cuts are coming. There was one on June 5, 2024, and another 25 bp cut on July 24, 2024. Additionally, inflation pressures in Canada are weakening where inflation in June 2024 cooled to 2.7%, and the labour market in Canada is also weakening, where the unemployment rate rose to 6.4% in June 2024. This puts pressure on the Bank of Canada to continue cutting interest rates. The Big 5 banks in Canada have their own interest rate expectations for the near future, and they are all downward trending:

CanadianMortgageTrends.com

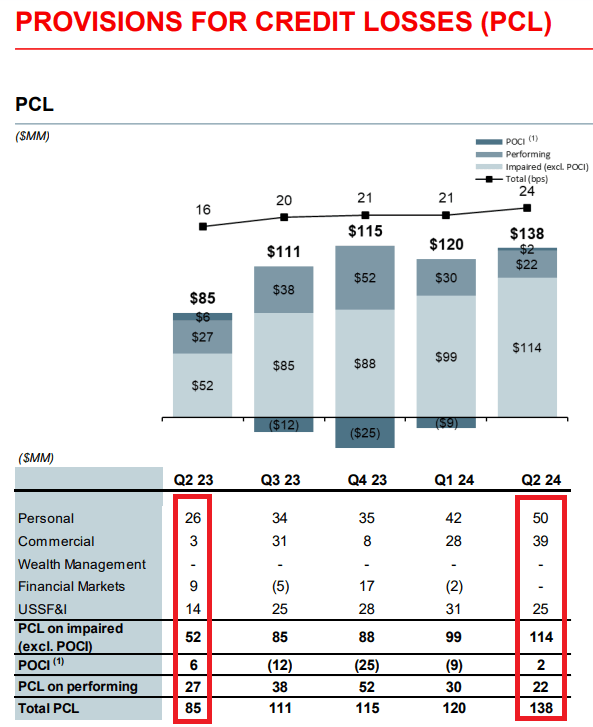

Zooming back into National Bank of Canada’s credit, we have this graphic from the Q2 2024 conference call that details the growth of allowances for credit losses over the last 4 quarters. Because there is still a cohort of mortgages whose rates will reset higher in 2025 and 2026 (they were originated in 2020 and 2021), my expectation is that PCL at National Bank of Canada will continue to inch higher over the next two years.

Q2 2024 National Bank of Canada Conference Call Presentation

To be clear, this is a short-term bump in the road, not a crisis. As I detailed out in my previous article about Royal Bank of Canada’s credit quality, Canada has many regulations on originating mortgages, including minimum down payments, maximum amortization periods, debt service ratios, interest rate stress tests, and minimum credit scores. These are guarantees that mortgages in Canada pass a minimum standard of quality in terms of the fundamentals of the borrower.

My bottom line is that it is very unlikely that a subprime mortgage crisis type of credit event will happen in Canada, but I would expect a further inch up in provisions for credit losses for personal & commercial banking at National Bank of Canada over the next 2 years. However, I don’t think that this should deter a long-term minded investor, because, like all acute economic events, this period of financial stress too will pass.

Valuation & Comparison With The Big 6

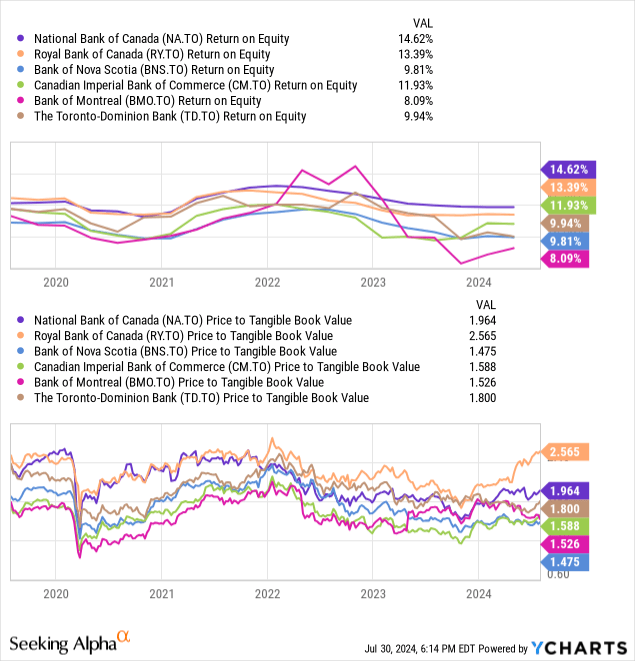

Except for a short blip in 2022 – 2023, National Bank of Canada had the highest return on equity over the last 5 years. There is a weak trend where the approximate order of a bank’s return on equity correlates to its order of ranking in its valuation as measured by price to tangible book value multiple.

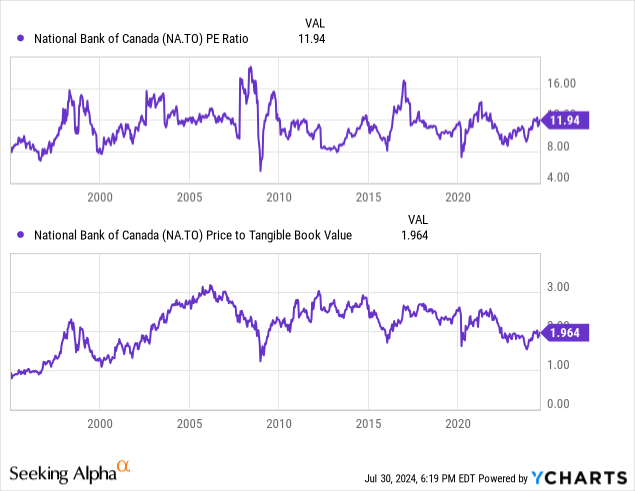

As measured by this multiple, National Bank of Canada is the second most expensive bank of the Big 6 in Canada, trading at 1.964x tangible book value. Let’s focus in on National Bank itself:

As measured by P/E ratio, National Bank of Canada has historically traded between 8x and 16x earnings, where 12x is roughly the historical average; currently National Bank’s valuation is at the historical average by this measure. As measured by price to tangible book value ratio, National Bank of Canada has historically traded between 1.5x – 3x, and currently sits in the middle of this range too. This indicates that now would be a very average time to be buying shares – National Bank of Canada is not “on sale” at the moment. The valuation reflects the fact that National Bank is a mature company, and the market seems to price it by asking “show us your profit figures”. I think the best way to build a position in National Bank of Canada is to dollar cost average over a period of time.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here

")

")