")

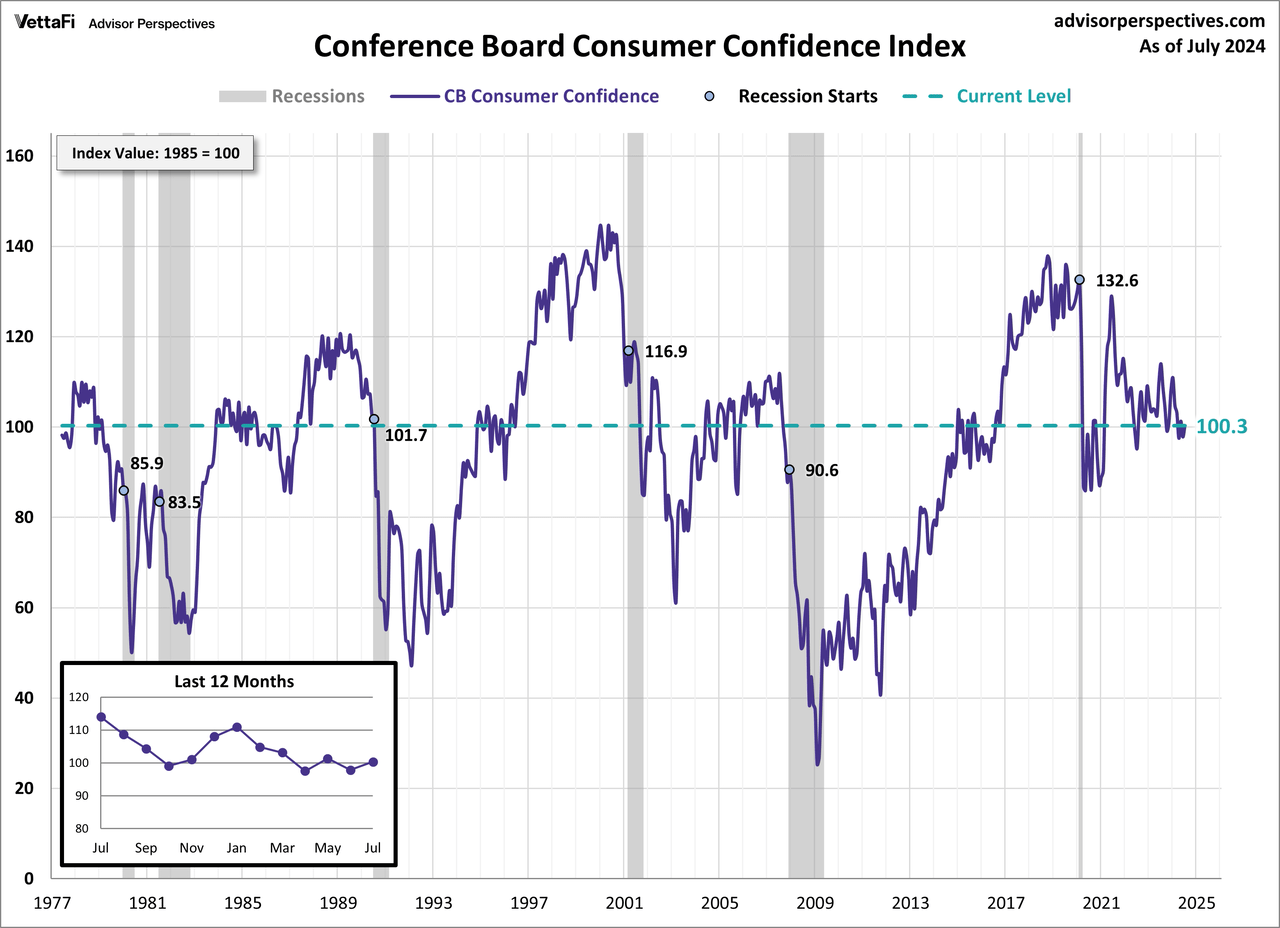

The Conference Board’s Consumer Confidence Index® ticked up in July. The index rose to 100.3 this month from June’s downwardly revised 97.8. This month’s reading was better than expected, exceeding the 99.7 forecast.

The Present Situation Index, which is based on consumers’ assessment of current business and labor market conditions, decreased to 133.6 from 135.3 in June. Meanwhile, the Expectations Index, which is based on consumers’ short-term outlook for income, business, and labor market conditions, rose to 78.2 from 72.8 in June. Note that a level of 80 or below for the Expectations Index historically signals a recession within the next year.

“Confidence increased in July, but not enough to break free of the narrow range that has prevailed over the past two years,” said Dana M. Peterson, Chief Economist at The Conference Board. “Even though consumers remain relatively positive about the labor market, they still appear to be concerned about elevated prices and interest rates, and uncertainty about the future; things that may not improve until next year.”

“Compared to last month, consumers were somewhat less pessimistic about the future. Expectations for future income improved slightly, but consumers remained generally negative about business and employment conditions ahead. Meanwhile, consumers were a bit less positive about current labor and business conditions. Potentially, smaller monthly job additions are weighing on consumers’ assessment of current job availability: while still quite strong, consumers’ assessment of the current labor market situation declined to its lowest level since March 2021.”

“In July, confidence improved among consumers under 35 and those 55 and older; only the 35-54 age group saw a decline. On a six-month moving average basis, confidence remained the highest among consumers under 35. On a month-over-month basis, no clear pattern emerged in terms of income groups. On a six-month moving average basis, consumers making over $100K were the most confident, but the gap with other groups narrowed.”

Peterson added: “The proportion of consumers predicting a forthcoming recession ticked up in July but remains well below the 2023 peak. Consumers’ assessments of their Family’s Financial Situation-both currently and over the next six months-was less positive. Indeed, assessments of familial finances have deteriorated continuously since the beginning of 2024.” (These measures are not included in calculating the Consumer Confidence Index®.)

Read more

Background on the Consumer Confidence Index

The Conference Board Consumer Confidence Index measures the consumers’ attitudes and confidence in the economy, business conditions, and labor market, with higher readings indicating higher optimism. The general assumption is that when consumers are more optimistic, they will spend more and stimulate economic growth. However, if consumers are pessimistic, then spending will decline and the economy may slow down. The index is based on a 5-question survey, with 2 questions related to present conditions and 3 questions related to future expectations. The survey began in 1967 and was conducted every two months but changed to monthly reporting in 1977, which is where our data begins.

The next two charts are attempts to evaluate the historical context for this index as a coincident indicator of the economy. The historical range of this indicator is from 25.3 to 144.7. In this chart, I have highlighted recessions and the level the index was at the start of each recession. The average of the consumer confidence index at the start of recessions is 101.9, a level we have been below for the past 4 months. The latest index reading of 100.3 is below 3 of the 6 recessions shown.

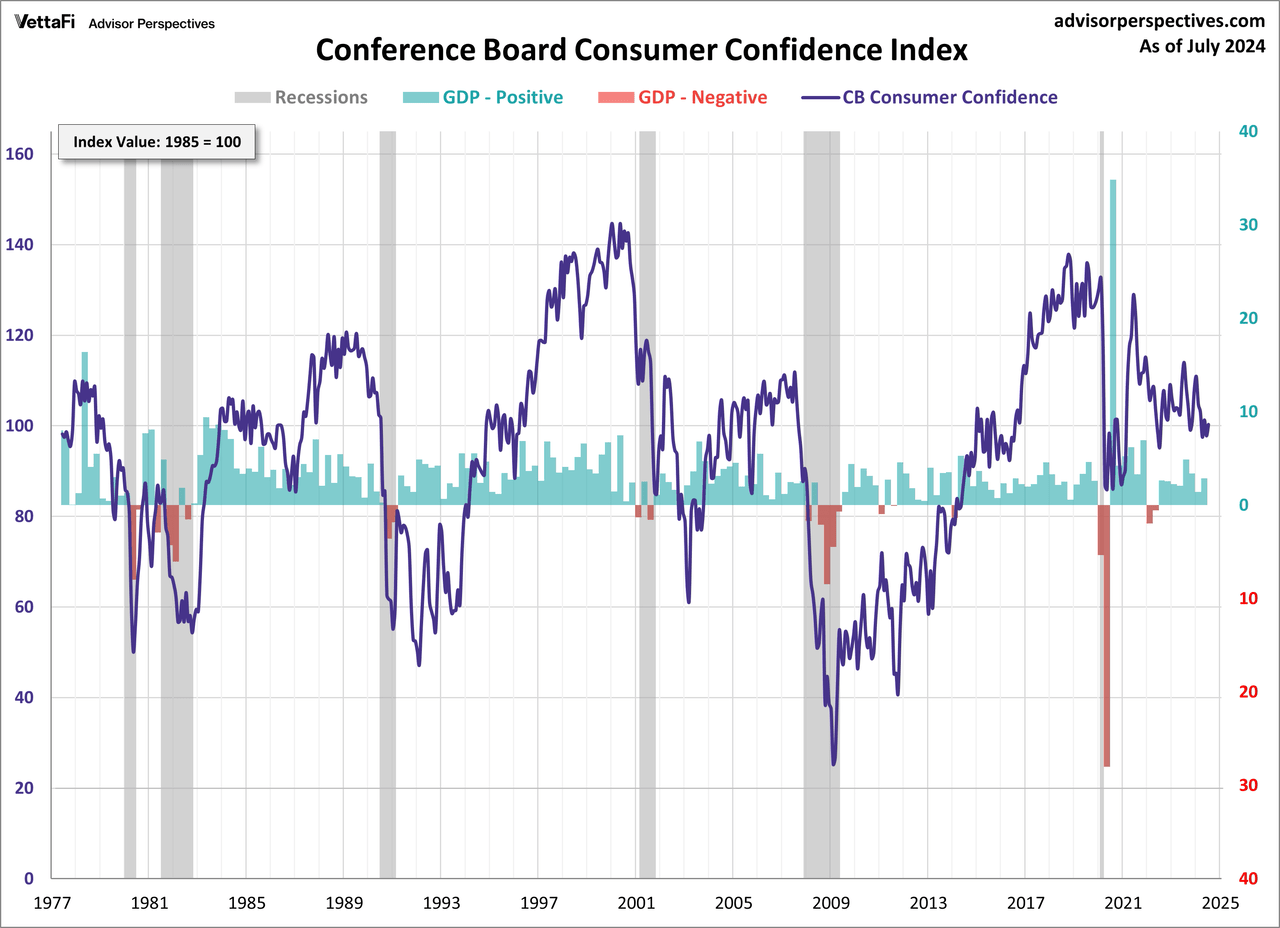

In this next chart, I have included an overlay with the GDP. It is easy to see the dips in consumer confidence when GDP is negative.

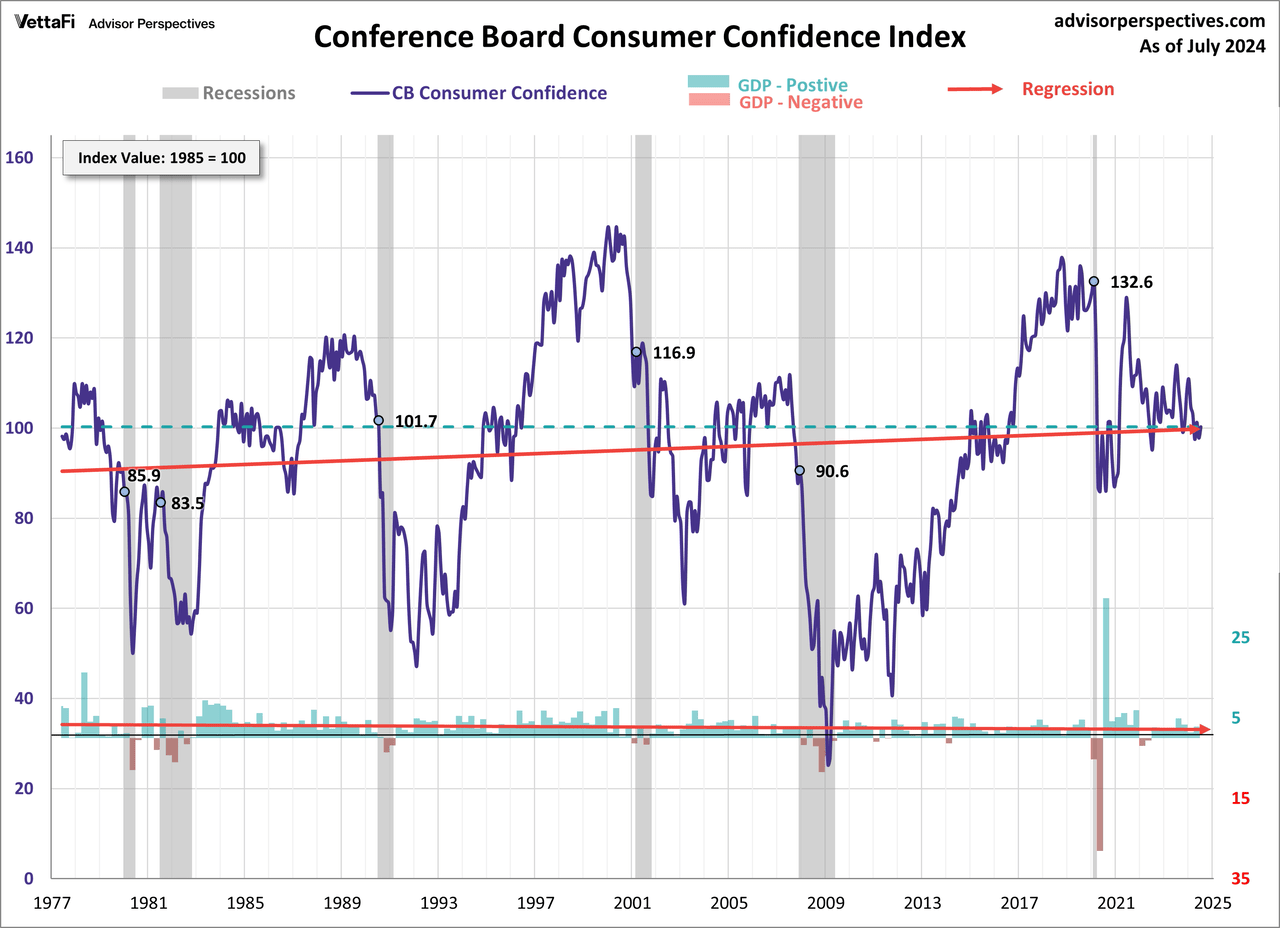

The next chart includes regression lines through the consumer confidence index and through the GDP. Interestingly, the GDP regression has a slight negative slope while consumer confidence has been increasing over the same time frame (since the late 1970s). It’s clear that consumer confidence begins falling shortly before official recession calls.

Other Sentiment Indicators

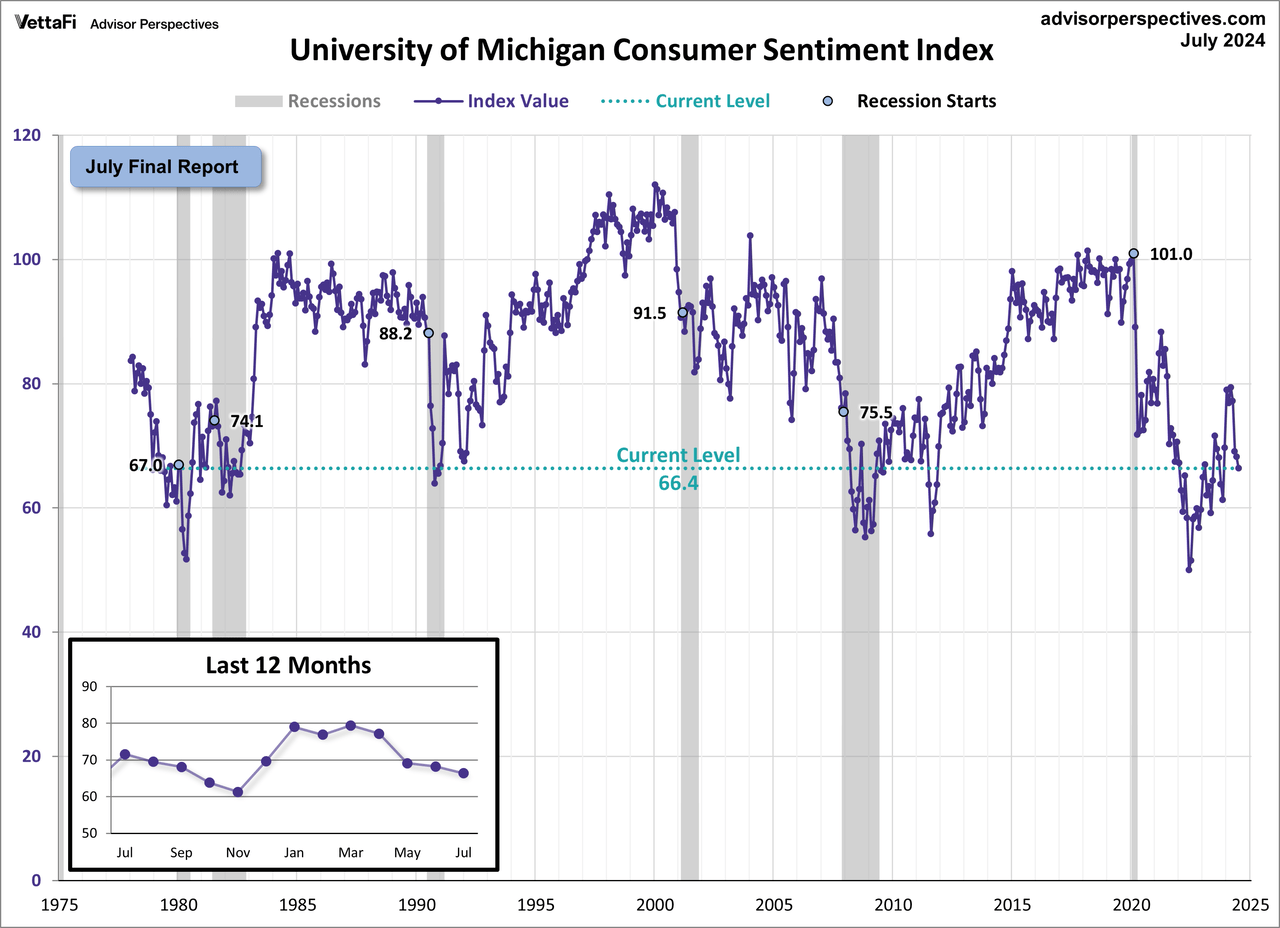

For an additional perspective on consumer attitudes, see the most recent University of Michigan Consumer Sentiment Index. Both indexes gauge consumer attitudes toward the current and future strength of the economy. However, the Consumer Confidence Index is more influenced by employment and labor market conditions, while the Michigan Sentiment Index is more focused on household finances and the impact of inflation.

The Conference Board index is the more volatile of the two, but the broad pattern and general trends have been remarkably similar to the Michigan index.

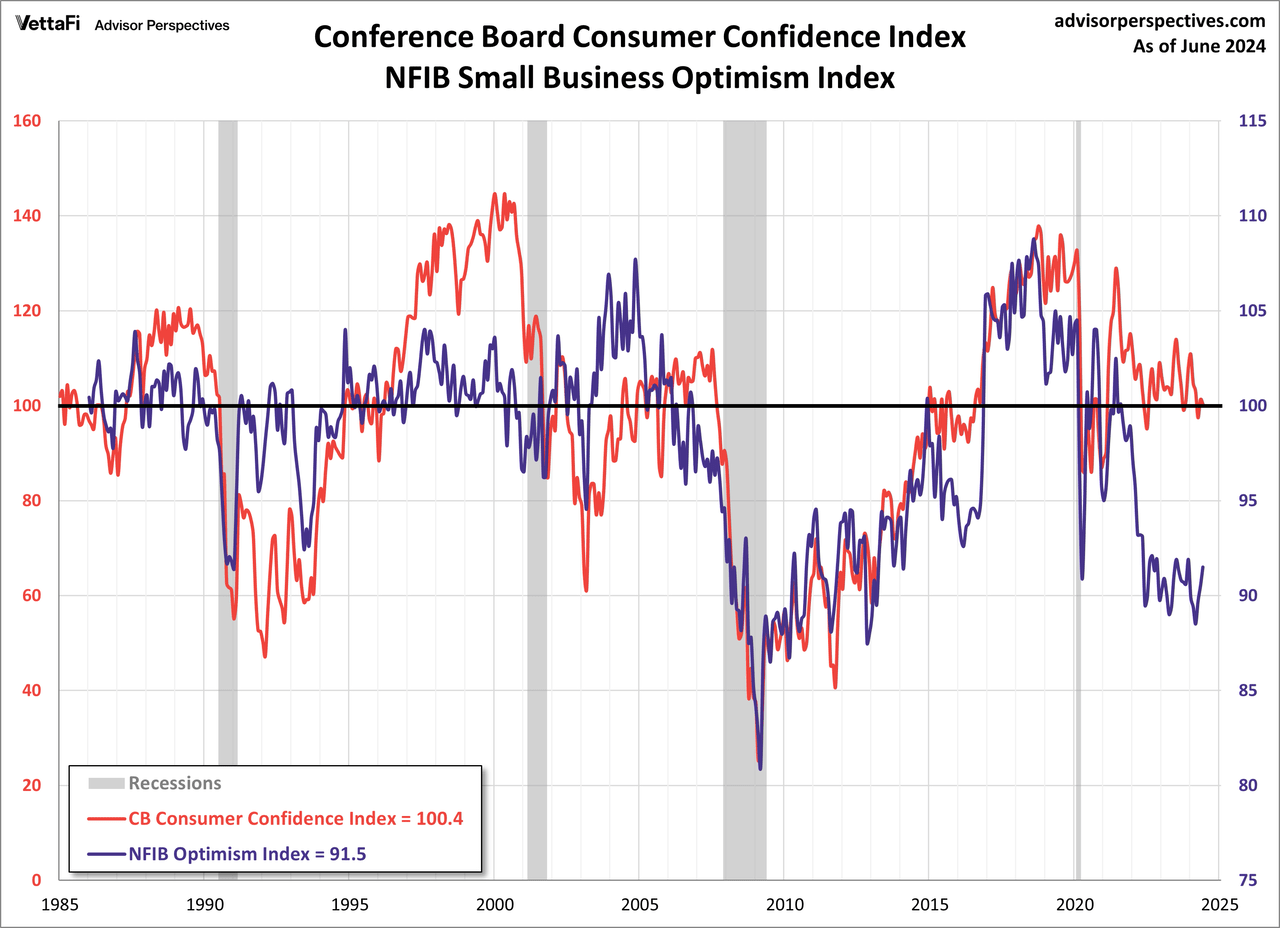

And finally, let’s take a look at the correlation between consumer confidence and small business sentiment, the latter by way of the NFIB Small Business Optimism Index. The consumer measure is the more volatile of the two, so it is plotted on a separate axis to give a better comparison of the two series from the common baseline of 100. As the chart illustrates, the two have tracked one another fairly closely since the onset of the financial crisis. The two have diverged at brief periods and been highly correlated at others.

ETFs associated with sentiment include: Consumer Discretionary Select Sector SPDR Fund (XLY).

Original Post

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.

Read the full article here

")