")

Krystal Biotech’s Vyjuvek: A Topical Triumph Driving Gains

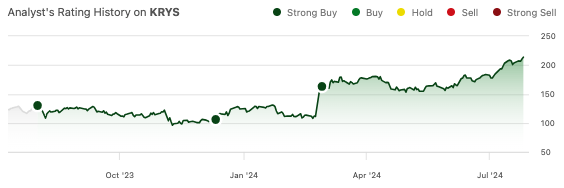

Krystal Biotech’s (NASDAQ:KRYS) stock has risen another 25.6% since my previous “strong buy” recommendation in February.

Seeking Alpha

Back then, I wrote about their Q4 earnings report, which showed strong sales and high patient compliance for Vyjuvek, Krystal Biotech’s dystrophic epidermolysis bullosa (DEB) topical therapy. Furthermore, the company was already reporting net income, which surprised me given that Vyjuvek had only recently entered the market and the company has a very active and diverse pipeline. Revenue increased slightly in the first quarter, from $42.1 million in the fourth quarter to $45.2 million. Krystal reported a marginal net income of $932,000 in the first quarter, which was impacted by a $12.5 million litigation settlement expense. The complaint, filed by “Periphagen,” alleged that Krystal breached a contract and misappropriated trade secrets. The settlement includes a series of $12.5 million payments from KRYS to Periphagen. KRYS owes $75 million, of which $37.5 million has already been paid.

Back to Q1 earnings: KRYS reported that weekly patient adherence remained high, at 91%, but this is down from 96% in Q4. So, the launch is going well. Analysts expect $65.49 million in Q2 when KRYS reports on August 5.

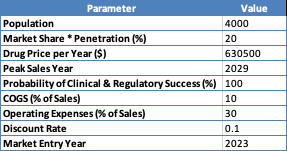

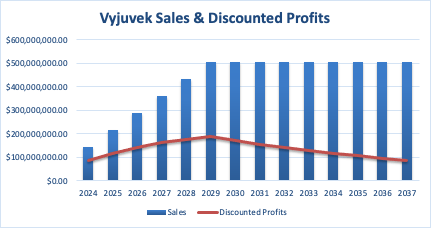

In terms of discounted cash flow analysis, my population estimate is 4,000 EU and US patients. This is consistent with KRYS’ own estimates and historical prevalence rates, which, generally, range between 3 and 10 affected persons per million. Vyjuvek costs about $630,500 per year. Because Vyjuvek is the only “novel topical wound therapy” approved in the US for DEB, I assigned it a market share of 80%. However, the penetration rate presents a challenge due to variances in severity and product availability (e.g., affordability), so I sided with a conservative figure (25%).

Author

The final calculation assumes linear growth in market share until the peak sales year, consistent drug pricing, fixed COGS and operating expense percentages, and a defined discount rate to calculate the present value of future cash flows. The final risk-adjusted net present value ($1.877 billion) is the sum of all discounted profits from the market entry year until 2037.

Author

Krystal’s Speculative Clinical Pursuits in Rare Respiratory Conditions and Oncology

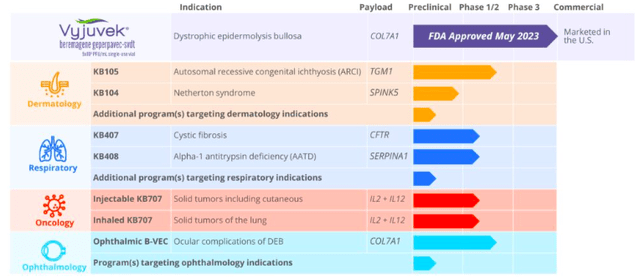

KRYS is progressing with its gene therapy targeting cystic fibrosis. KB407 is currently undergoing a Phase 1 dose-escalation clinical trial in patients with CF. 407 utilizes an HSV-1-based gene therapy vector theorized to transduce “full-length human CFTR” and deliver it to airway epithelial cell populations. This approach is a bit unconventional, as adeno-associated viruses (AAV) naturally target these cells and have established safety (e.g., Luxturna and Zolgensma), although initial efforts in CF fell short. In fact, KRYS’ Vyjuvek was the first gene therapy to be approved utilizing HSV-1 vectors.

KRYS is also in Phase 1 development, targeting another rare respiratory genetic disorder, alpha-1 antitrypsin deficiency (AATD), with KB408, another HSV-1-derived vector to deliver copies of the SERPINA1 gene.

Both CF and AATD are heavily contested fields, with several players in Phase 1/2 testing gene therapies (e.g., with AAV vectors developed to overcome past challenges in CF), siRNA, and small molecules.

KRYS is also testing KB707, both as an inhalation and injection, in patients with solid tumors of the lung and injectable solid tumors, respectively. 707 is, again, an HSV-1 vector. It intends to deliver genes encoding both IL-12 and IL-2, which are key markers in the tumor microenvironment.

Q1 Earnings

KRYS reported $45.25 million in product revenue in Q1. COGS was just $2.419 million. R&D and SG&A expenses totaled $10.957 million and $26.058 million, respectively. After accounting for the $12.5 million “litigation settlement,” loss from operations was $6.684 million. Net income was $932,000 after “interest and other income” of $7.616 million. EPS (basic and diluted) was $0.03.

Financial Health

As of March 31, KRYS had $359 million in cash and cash equivalents and $179.253 million in short-term investments. Total current assets were $853.269 million, while total current liabilities were just $47.589 million.

KRYS added $15.888 million in cash via operating activities in Q1. Since they are profitable, although only marginally, I will not estimate the cash runway. It is worth mentioning that any changes in revenue could substantially alter their financial outlook, and the company remains heavily dependent on Vyjuvek.

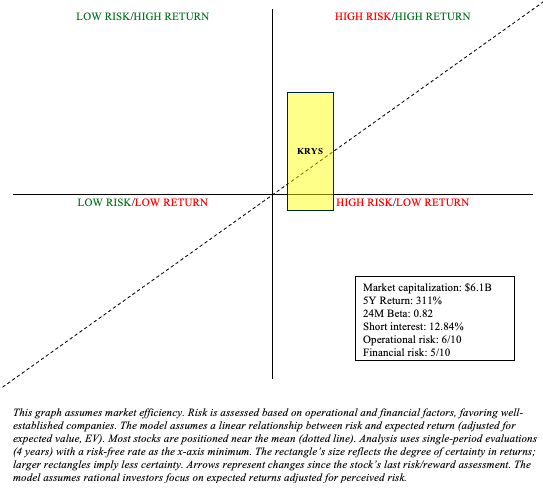

Risk/Reward Analysis and Investment Recommendation

Vyjuvek continues to impress early on in its commercialization and should continue to provide KRYS with considerable income to fund their other clinical pursuits. However, KRYS’ pipeline, beyond Vyjuvek, is pretty speculative and pursuing highly contested indications.

Krystal Biotech

So, while Vyjuvek provides a nice floor for KRYS, it’s challenging to see how else the company will justify its valuation in the future. So, there remains a lot of uncertainty with KRYS. Subsequently, I think it’s prudent to downgrade to “hold” based on the company’s high valuation, bearing in mind that this is a stock that’s appreciated ~90% since my December “strong buy” recommendation.

Author

To be clear, I believe KRYS is still worth holding, particularly within a barbell portfolio. It’s just that I wouldn’t add at these prices. I do appreciate their efforts in other rare, genetically driven dermatological conditions like KB105 for TGM1-ARCI, providing optionality beyond DEB, where they have an edge. Furthermore, I think their efforts in aesthetics, via its wholly owned subsidiary, Jeune, though speculative, are interesting.

Read the full article here

")