")

Ambac (NYSE:AMBC) recently sold its Financial Guarantee (aka legacy) business to funds managed by Oaktree in a deal that sent the stock price down more than 20%. The transaction clearly left investors disappointed, as they were expecting a much more attractive valuation. Additionally, the company invested a significant amount of these proceeds into a new business instead of making special distributions.

We will unbundle what happened over the past few months and provide an outlook on the future of this business, which recently changed shape. However, there still is some upside, although more limited.

After 15 years of run-off, the Financial Guarantees business is sold at a disappointing valuation

The company reported as soon as 2023 that they engaged the investment bank Moelis to conduct a strategic review of the business, including a potential sale of the FG division. Investors piled into the stock, which saw its highest valuation in years, fueled by expectations that the legacy business that was in run-off since 2009 could attract generous suitors.

However, the company announced a sale for only $420 million in cash to funds managed by Oaktree, the famed private equity and debt investor. This was clearly below expectations, as the stock tanked as much as 19% in one single day.

But let’s dive into the valuation and compare it to our previous SOTP analysis we presented earlier this year before the transaction was announced.

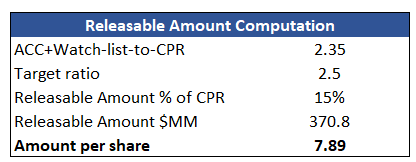

CPR Calculation (Author’s Analysis)

Our estimate of Claims-Paying-Resources (CPR), an indicator of how many resources the business had to pay its obligations, showed around $370 million of releasable amount. This figure was computed by looking at its closest competitor, MBIA, and assuming a target ratio of CPR-to-obligations. This estimate was actually very close to the actual sale figure of $420 million. However, our SOTP analysis showed a significant upside potential that was primarily driven by the other divisions of Ambac. We estimated that the total fair value for the company was around $800 million, which today would translate into $850 million given the $50 million extra realized on the legacy business, or $19 per share. We are not alone in this upside potential assumption, as Oaktree itself will also receive 10% of Ambac’s share capital through warrants with a $18.50 strike price. Do we still believe in so much potential? Well, let’s dive into what happens next.

The new acquisition: $280 million for another insurance company?

What we think caused the bulk of the stock move wasn’t actually the sale price. We think that how the company decided to invest the proceeds played actually a larger role in the reaction. Ambac acquired a 60% majority stake in Beat Capital Partners, a London-based insurance underwriting platform, for a consideration of $280 million. This values the target at around $460 million, or 17x 2024 EBITDA ($27 million). This is a very generous valuation, and it is probably the reason behind the negative stock price reaction. As a comparison, we used a 6.5x multiple for Cirrata, Ambac’s own insurance broker. This kind of M&A is known for putting at risk shareholder value, and several investors were not expecting it.

Company Forecasts (Latest Presentation)

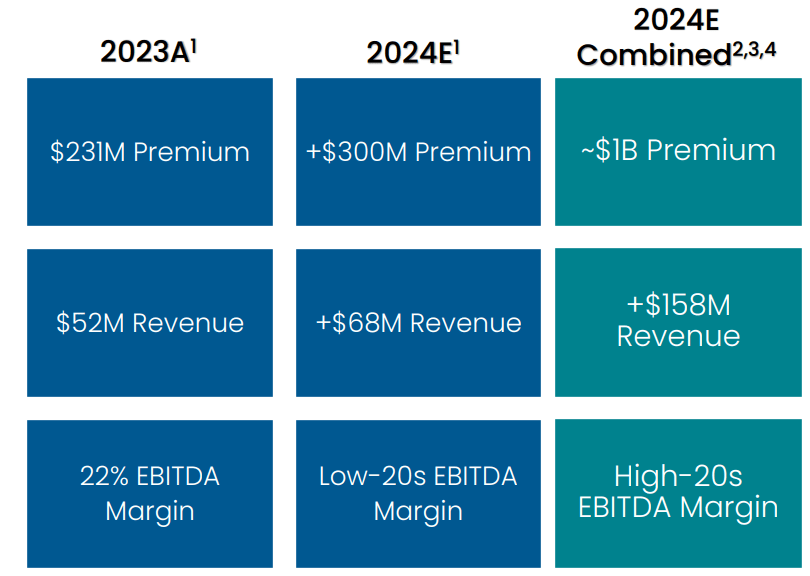

This is how management is trying to justify the transaction. Their goal is to accelerate the path towards $100 million of EBITDA within 3 years, which would imply a multiple of around 4.5x-5.5x depending on the unclear Pro Forma cash. They are also expecting margin improvements, primarily from synergies between the two businesses and their distribution. They also stated that the transaction will help diversify Cirrata’s current risk base, primarily concentrated into medical and employee benefits (around 50% of total risk).

Bottom Line: A New Valuation Framework

We are not enthusiastic about this recent acquisition, but we want to make the effort of doing the math and putting numbers in perspective. We will use the same SOTP analysis which now has a certain figure around the legacy business, and also to evaluate the new Cirrata+BMO division.

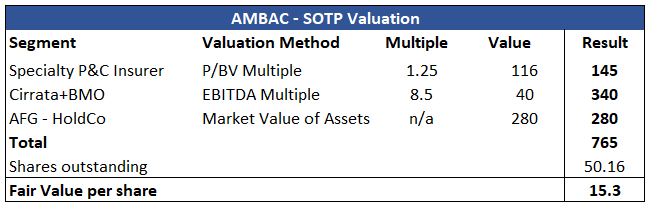

SOTP Analysis (Author’s Analysis)

We have computed the cash at the HoldCo level using the Q1 figures and adding what’s left after the acquisition from the legacy sale. We also used a conservative 8.5x multiple for the new Cirrata+BMO, significantly below the amount paid (17x). After adjusting the share count to reflect the potentially dilutive effect of Oaktree’s warrants, we highlight a fair value per share of around $15, or around 20% higher than today’s levels.

Conclusion

Ambac recently completed a significant reshaping of the entire company, with two major transactions announced. We think that while the sale happened at terms in line with our expectations, the acquisition of BMO was generous in its multiple. However, the business still looks sound and the overall upside potential is around 20%.

Read the full article here