")

")

")

Dear readers/followers,

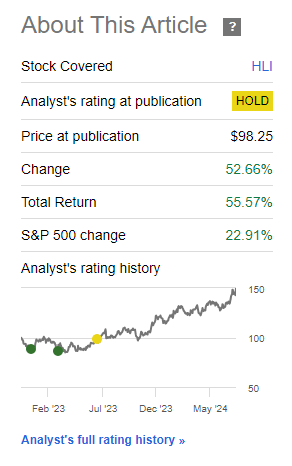

This article is going to be an update on the investment bank Houlihan Lokey (NYSE:HLI). Thankfully, I still own some shares (a small position, I rotated some of it) that I bought all the way back in early 2023. I did, however, go “Hold” on the company’s prospects for 2023-2024 only a few months after that, back in the summer of 2023. You can find that particular article here, and see that the bank has actually outperformed the S&P 500 2x since then.

Seeking Alpha Houlihan Lokey RoR (Seeking Alpha Houlihan Lokey RoR)

I wish I could take credit for the bullish recommendations, but the fact is because I went “hold”, there’s no credit here to take. I can also be honest and say, clearly, that I did not expect HLI to outperform in this manner. This is despite its strong market position with an M&A expertise/restructuring and other upsides.

So, in this article, I mean to look at what could cause further outperformance for the business, and if the company, despite the returns for the last 12 months, could be considered to be anything close to a “buy” here.

There are risks to this company – but what upside remains at this time?

Let’s take a look.

Houlihan Lokey – Revisiting a bit of a “failure”

I call my thesis for Houlihan Lokey, despite being up 50%, a failure. This is because I changed my thesis too early, resulting in perhaps some investors and readers not “getting” the upside here, and I do seek to be specific and find the valuation “sweet spot” for all of my investments. With HLI, this has failed until now.

Most coverage for the company has been positive lately, with SA analysts having only positive stances since January of this year. I will tell you in advance that I do not view Houlihan Lokey to be a “buy” here, so I’m sticking to my “hold” rating at a price of almost $150/share at the time of writing this piece.

This is despite some truly excellent fundamentals, including very conservative leverage.

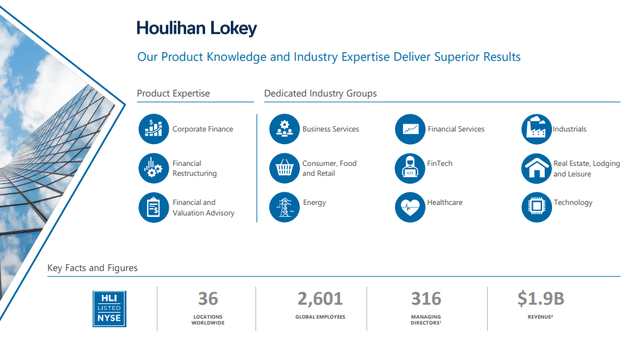

To understand my stance, you need to understand Houlihan Lokey and how I view the company’s potential for business outperformance. As an investment bank with a multinational profile, but with a specialty attention towards very specific “service” segments, it’s fair to say that Houlihan Lokey operates in a bit of a niche position on the market.

All of these services that the company offers are, without a doubt, crucial. This includes things like M&A’ing and restructuring which, while cyclical, has seen a lot of interest due to the state of the previous overall macro/current economy, where businesses are more likely than before to be in need of such services (bankruptcy and the like).

HLI IR (HLI IR)

So, a market leader or above-market leader who manages such services with an impressive profit margin (15% on average, or thereabout) is something to be interested in. Houlihan Lokey also has very impressive trends when it comes to the stability of its earnings and profit, in that it hasn’t gone negative or “bad” for a long time (5+ years).

It did, however, experience a non-trivial decline during 2023 (last year), when earnings moved from ZIRP. ZIRP had seen the company’s earnings spike due to significant interest in its services, seeing it peak at around $7.1 in adjusted EPS in 2022, only to crater to roughly $4.5 in 2023, and expected to stay at a similar or lower level (2024 is done).

And, let me make it clear that the company is not currently expected to materially improve from that until at the very earliest -26 or -27 (Source: Paywalled F.A.S.T graphs link).

On paper, we can say that the company seems like a very attractive business. With its worldwide coverage and over 2,600+ employees generating upwards of $2B in annual revenues, it’s in a very attractive position on the market, because it earns both during up and down cycles, even if cycles like this one would be more impaired in terms of M&A. This is reflected in the financial performance, where 2024 (the fiscal of 2024 is closed for HLI, it’s already in Fiscal -25), generated $440M of Pre-tax income, comparable to the YoY figure.

Where I’m having trouble reconciling the premium that’s being demanded is that HLI margins are actually down. Pre-tax earnings are showing EBIT margins of 23%, down from 23.7% last year, almost 30% during -22, and 24.5% back before COVID. This is not a positive evolution of this KPI.

If you’re an HLI bull, you should focus on where the company is “amazing”, and there are many ways in which the company fulfills this. This includes being a market leader in restructuring, M&A, and Global Fairness Opinion. Quite literally, no other company manages to beat HLI here. The closest would be Rothschild & Co in M&A, which is only 3 below in terms of a number of M&A deals.

HLI also has a very diverse mix of clients and industries. You can’t claim that HLI is geographically diverse (70%+ Americans) or Segment diverse (58% corporate finance, 27% financial restructuring), but it does have several strings to its “lute”.

And for clients in Europe, it does offer comprehensive coverage, should they want to take advantage of this.

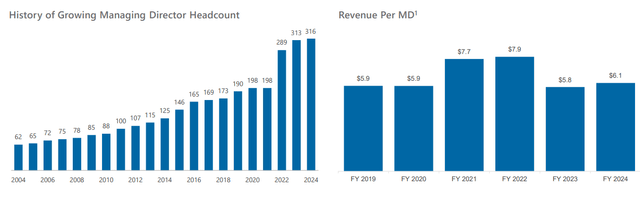

Another metric I’d keep a close eye on is the number of Managing Directors, or MDs, and the revenue they generate – because this is a key indicator for how well the company is doing as well.

HLI isn’t doing bad at all – it’s just “back down” from ZIRP, and normalization is not a “bad” thing.

HLI IR (HLI IR)

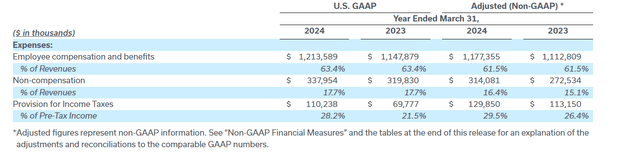

4Q24, or fiscal 2024 came to an end with the report in May. Revenues were up, and net income was up for the year but down for the quarter YoY. However, we are still managing one of the best revenues ever. The company uses the same expression that many businesses seem to use these days; “good performance in a challenging market”, and for HLI this is true. The M&A environment is described as being somewhat “sluggish” here but with signs of improvement.

Where I see impressive trends is the expense side of things. In particular, the company managed to keep things stable here – that is no small feat. While it is a percentage of a higher amount, it hasn’t changed as a percentage, which was something I actually forecasted the company as seeing.

HLI 4Q24 Results (HLI 4Q24 Results)

And if we look at the quarterly results, the company actually managed to reduce it to 63.3% for the employee comp.

So I would characterize the results presented as positive. I would also say that there’s upside potential here, but due to the macro, I would say that there is likely to be some time before some of that upside potential becomes relevant.

Let’s look at where this puts the company valuation.

Houlihan Lokey Valuation – The company is not attractive here

As I see it, it doesn’t matter how you view the company’s future prospects here, because the company’s valuation has ballooned to extreme levels. What do I mean by extreme?

I mean that HLI is now trading at 31x P/E, compared to a historical 5-year average of 16.5x. That approaches the double average here. There is, as I see it, no excuse or justification for this. Even if the company were to, as expected currently, move up towards a $7 EPS normalized in the next few years, that would be no higher than during ZIRP. While this implies impressive double-digit growth, at 16.5x P/E, that double-digit growth at today’s valuation implies a negative annualized rate of return of almost 8% per year, or 20% until the end of fiscal 2027. And this, by the way, is with the current dividend expectations, with a dividend yield that’s no higher than 1.52%

What would you have to expect in order to get double-digit positive RoR here? You’d have to forecast it at least 27x P/E. There is no long-term historical valuation precedence for that sort of long-term level of valuation. Even if you say, that HLI is worth 25x (which I don’t believe, but still), that’s only 6.7% per year – there are certain IG-rated prefs and bond-type investments that yield similar levels to this and at less risk.

I see the overhang of a valuation decline or normalization here as significant. While I did indeed fail in forecasting just how high the company could climb, I believe the degree of valuation inflation here is so significant that Houlihan Lokey should be avoided.

My last price target for this company was something around $80/share, which by the way is still 16-17x P/E normalized for the 2024 fiscal. I’m willing to increase this to $95/share here, allowing for the 13-14% annualized rate of earnings growth that I view as quite realistic. But the price at which the company trades for that today is not something I view as realistic.

For that reason, I see the following risks.

Risks to a (positive) Houlihan Lokey Thesis

The risk here is obvious to me. If you invest in Houlihan Lokey at a 30x P/E, you’re expecting the company (provided you want double-digit positive returns) to maintain this, or a level of valuation close to this – something like a 27-31x P/E. I do not believe this as a sustainable expectation given both the yield, the operational specifics, and the historical valuation levels, which are around 50-60% of this level.

Recent trends and moves have put this company at a price where I don’t believe it makes sense. Yes, it’s a market leader in a hard-to-lead market segment/s – but that still doesn’t justify this.

Investment banks such as HLI are also exposed to cyclical developments, and while HLI due to its segment and operational specifics are less exposed than some, I would still not say that it’s immune.

Based on these risks to the company, I say that the thesis for HLI is as follows here, and I remain at a “hold”.

Thesis

- Houlihan Lokey is a market-leading expert in a field that demands the highest sort of financial expertise. The company has every hallmark of a qualitative, well-run, and sound business, making it a highly investable prospect at the right price – but the company has recently reached well beyond that price.

- For me, that right price currently comes at a PT of $95 given the current share price and forecast trends, but also where the company is going from here.

- Based on these targets, I give HLI a “hold” here, and I say the company is dangerously overvalued here.

Remember, I’m all about:

1. Buying undervalued – even if that undervaluation is slight, and not mind-numbingly massive – companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

2. If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

3. If the company doesn’t go into overvaluation, but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

4. I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them (italicized).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion.

I won’t call it cheap, and it no longer has a good enough realistic upside for me to invest in. This is a “hold” for me now.

Read the full article here

")

")

")

Business Update Conference Call Transcript")