")

")

The following segment was excerpted from this fund letter.

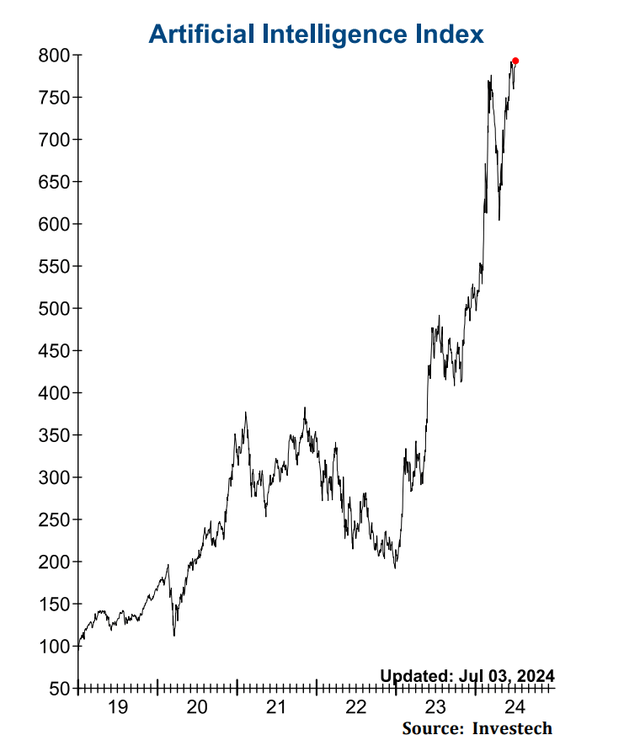

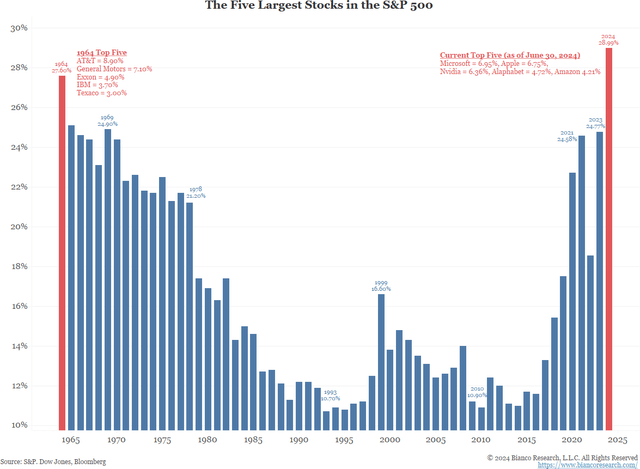

In our last letter, we chronicled the incredible performance of a select number of AI-related technology companies and its outsized impact on market indices. Well, these stocks didn’t skip a beat during the quarter. (As of this writing, the so called Magnificent Seven are up +47 year-to-date, while the rest of the S&P 500 Index is just up +7.5%.) Indeed, some of the “diversified” benchmarks stock weightings have reached absurd levels. Take the Standard & Poor’s 500 Index (SP500, SPX), by far the money management’s most common benchmark. The S&P 500 Index is currently composed of 503 constituent stocks. As of this writing, the top six stocks make up 31% of the index. If that isn’t extreme enough, consider the Russell 1000 Growth Index. This index is currently made up of 440 stocks. The same top 6 stocks make up 50% of this benchmark!

The raison d’être of our investment philosophy is that to improve the odds of outperforming any benchmark, an active equity manager must build a portfolio that looks different from its respective peers and associated benchmarks – in our case, we are quite different. That’s why we invest in only 20 or so stocks. For example, currently our top four holdings, all technology stocks (Alphabet, Meta Platforms, Taiwan Semiconductor Manufacturing and Apple), make up nearly 32% of our portfolio. We do live (and invest) in interesting times when our focused, 20-stock portfolio is arguably as diversified (if not more) than our benchmarks that carry hundreds of stocks.

According to Bloomberg, there is over $30 trillion invested in passive index related funds and ETFs – and growing by billions per day. They note that the NASDAQ 100 market valuation was just over $12 trillion as recently as the first quarter last year. Fast forward a quick 15 months and that valuation figure has surpassed $24 trillion! The wonderful feature of most indexed funds and ETFs (and most successful investors we follow) is that such vehicles “let their winners run.” Most investors, both professional and lay find this to be quite difficult. As the late, great Charlie Munger has often quipped, “The waiting is the hardest part.” That said, the downfall of indexation is the complete absence of any valuation strictures or discipline. Today, every new dollar allocated to a S&P 500 Index fund; $.31 cents goes into just 6 stocks – regardless of valuation. Passive-aggressive, indeed.

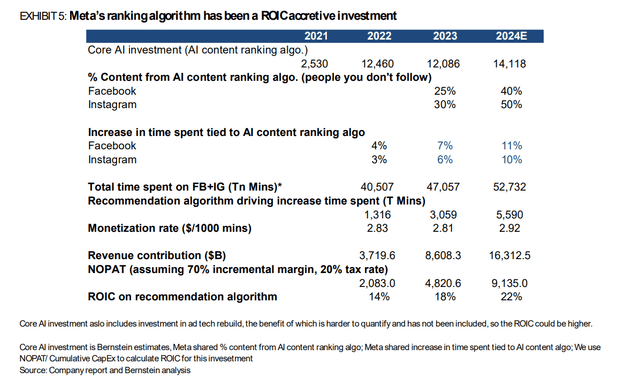

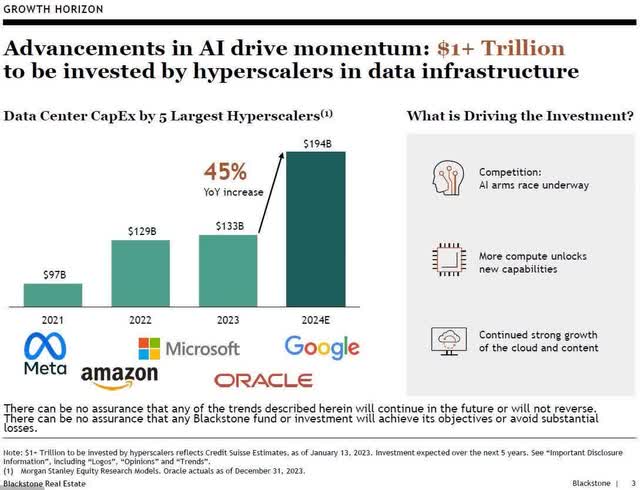

In light of the historically concentrated benchmark weightings, it is important to mention that in our technology-related holdings, we are currently only overweight in our Alphabet (GOOG,GOOGL), Meta Platform (META) and Taiwan Semiconductor Manufacturing (TSM, OTC:TSMWF) holdings. Of significant note, our +8% weighting in Taiwan Semiconductor Manufacturing is rather unique in that this +$980 billion market cap company (and arguably the most critical cog in the global technology sphere) is not represented at all in either of these two benchmarks. Thus, we are beneficiaries of huge active share in a single portfolio holding. However, each of these three holding are approaching our self-imposed maximum weight, so future likely weights will be lower, rather than higher still. Our biggest concerns with the current AI-hype, as it pertains to our few holdings that are spending billions in AI, specifically Alphabet and Meta Platforms, are the current and nearer-term returns such billions in capex are and will generate for shareholders. Bernstein Research illustrates this below on Meta Platforms.

The good news for these two companies is they both have been utilizing AI for some years now with concomitant profitability. The more concerning reality is both companies, plus the entire AI space are spending at levels indicative of an “AI arms race.” At this stage of the AI boom (mania?), woe to the company that chickens-out and isn’t aggressively competing in the trillion-dollar AI spending sprint. As such, the lines between maintenance capex and growth capex have become blurred. We expect much more scrutiny from investors on this conundrum in the quarters and years ahead. This much is certain: The moment any one of the largest data center providers suggest a “pause” in its AI spending to “digest” the many billions already spent, then investors (speculators) will suddenly discover just how cyclical the AI race really is.

Yardeni Research reports the following:

-

But at some point, too much capital can end even the best of parties. There are hundreds of small companies that have raised billions of dollars from venture capitalists hoping to discover the next ChatGPT.

-

Investors have poured $330 billion into 26,000 AI startups over the past three years, which is two-thirds more than was spent funding 20,350 startups from 2018-20, according to an April 29 NYT article citing PitchBook data. Likewise, generative AI deals attracted $21.8 billion last year, up fivefold from 2022, according to CB Insights data in an April 29 WSJ article.

-

The AI kings talk big. Like every hip new tech industry, the AI world has its rockstars, including Nvidia’s (NVDA) Jensen Huang, ChatGPT’s Sam Altman, and Tesla’s (TSLA) Elon Musk. Some sound like they’ve drunk too much AI Kool-Aid.

-

Huang also noted that the company’s business was about to expand into the robotics and the sovereign AI businesses. “The next wave of AI is set to automate the $50 trillion in heavy industries” with robotics factories that “will orchestrate robots that build robots that build products that are robotic.”

-

Not to be outdone, ChatGPT CEO Sam Altman at the Aspen Institute Ideas Festival compared the rise of AI to the discovery of agriculture and the invention of industrial-era machines. He claimed that AI will dramatically increase productivity and help global GDP grow 7% annually to double within 10 years. While we concur with Altman that AI will enhance productivity and boost economic growth, doubling the size of the world economy in a decade is quite a claim.

The following is a sober reflection of the AI boom circa-2024 from Sequoia Capital (July 2024):

“What has changed since September 2023?”

- The supply shortage has subsided: Late 2023 was the peak of the GPU supply shortage. Startups were calling VCs, calling anyone that would talk to them, asking for help getting access to GPUs. Today, that concern has been almost entirely eliminated. For most people I speak with, it’s relatively easy to get GPUs now with reasonable lead times.

- GPU stockpiles are growing: NVIDIA reported in Q4 that about half of its data center revenue came from the large cloud providers. Microsoft alone likely represented approximately 22% of NVIDIA’s Q4 revenue. Hyperscale CapEx is reaching historic levels. These investments were a major theme of Big Tech Q1 ’24 earnings, with CEOs effectively telling the market: “We’re going to invest in GPUs whether you like it or not.” Stockpiling hardware is not a new phenomenon, and the catalyst for a reset will be once the stockpiles are large enough that demand decreases.

- OpenAI still has the lion’s share of AI revenue: The Information recently reported that OpenAI’s revenue is now $3.4 billion, up from $1.6 billion in late 2023. While we’ve seen a handful of startups scale revenues into the <$100M range, the gap between OpenAI and everyone else continues to loom large. Outside of ChatGPT, how many AI products are consumers really using today? Consider how much value you get from Netflix for $15.49/month or Spotify for $11.99. Long term, AI companies will need to deliver significant value for consumers to continue opening their wallets.

- The $125B hole is now a $500B hole: In the last analysis, I generously assumed that each of Google, Microsoft, Apple and Meta will be able to generate $10 billion annually from new AI-related revenue. I also assumed $5 billion in new AI revenue for each of Oracle, ByteDance, Alibaba, Tencent, X and Tesla. Even if this remains true and we add a few more companies to the list, the $125 billion hole is now going to become a $500 billion hole.

- It’s not over-the B100 is coming: Earlier this year, NVIDIA announced their B100 chip, which will have 2.5X better performance for only 25% more cost. I expect this will lead to a final surge in demand for NVDA chips. The B100 represents a dramatic cost vs. performance improvement over the H100, and there will likely be yet another supply shortage as everyone tries to get their hands on B100s later this year.

“One of the major rebuttals to my last piece was that “GPU CapEx is like building railroads” and eventually the trains will come, as will the destinations – the new agriculture exports, amusement parks, malls, etc. I actually agree with this, but I think it misses a few points:”

- Lack of pricing power: In the case of physical infrastructure build outs, there is some intrinsic value associated with the infrastructure you are building. If you own the tracks between San Francisco and Los Angeles, you likely have some kind of monopolistic pricing power, because there can only be so many tracks laid between place A and place B. In the case of GPU data centers, there is much less pricing power. GPU computing is increasingly turning into a commodity, metered per hour. Unlike the CPU cloud, which became an oligopoly, new entrants building dedicated AI clouds continue to flood the market. Without a monopoly or oligopoly, high fixed cost + low marginal cost businesses almost always see prices competed down to marginal cost (e.g., airlines).

- Investment incineration: Even in the case of railroads – and in the case of many new technologies – speculative investment frenzies often lead to high rates of capital incineration. The Engines that Move Markets is one of the best textbooks on technology investing, and the major takeaway – indeed, focused on railroads – is that a lot of people lose a lot of money during speculative technology waves. It’s hard to pick winners, but much easier to pick losers (canals, in the case of railroads).

- Depreciation: We know from the history of technology that semiconductors tend to get better and better. NVIDIA is going to keep producing better next-generation chips like the B100. This will lead to more rapid depreciation of the last-gen chips. Because the market under-appreciates the B100 and the rate at which next-gen chips will improve, it overestimates the extent to which H100s purchased today will hold their value in 3-4 years. Again, this parallel doesn’t exist for physical infrastructure, which does not follow any “Moore’s Law” type curve, such that cost vs. performance continuously improves.

- Winners vs. losers: I think we need to look carefully at winners and losers – there are always winners during periods of excess infrastructure building. AI is likely to be the next transformative technology wave, and as I mentioned in the last piece, declining prices for GPU computing is actually good for long-term innovation and good for startups. If my forecast comes to bear, it will cause harm primarily to investors. Founders and company builders will continue to build in AI – and they will be more likely to succeed, because they will benefit both from lower costs and from learnings accrued during this period of experimentation.

“A huge amount of economic value is going to be created by AI. Company builders focused on delivering value to end users will be rewarded handsomely. We are living through what has the potential to be a generation-defining technology wave. Companies like NVIDIA deserve enormous credit for the role they’ve played in enabling this transition and are likely to play a critical role in the ecosystem for a long time to come. Speculative frenzies are part of technology, and so they are not something to be afraid of. Those who remain level-headed through this moment have the chance to build extremely important companies. But we need to make sure not to believe in the delusion that has now spread from Silicon Valley to the rest of the country, and indeed the world. That delusion says that we’re all going to get rich quick, because AGI is coming tomorrow, and we all need to stockpile the only valuable resource, which is GPUs. In reality, the road ahead is going to be a long one. It will have ups and downs. But almost certainly it will be worthwhile.”

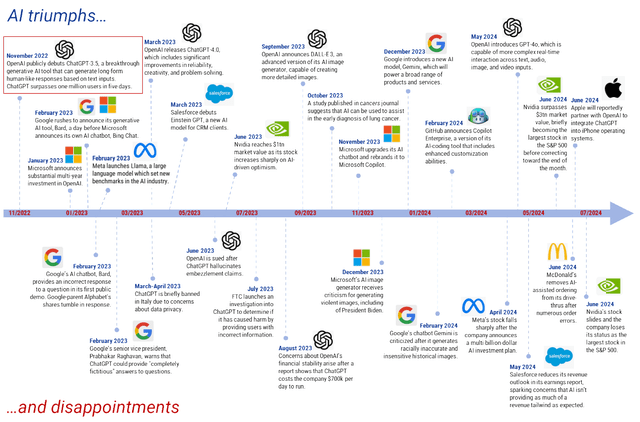

A short history of AI developments

Goldman Sachs Global Investment Research (Source: BBC, cancers, OpenAI, Tech.co | Technology News, Reviews and Advice Guides, Google, various news sources, compiled by Goldman Sachs GIR)

Blackstone: On AI

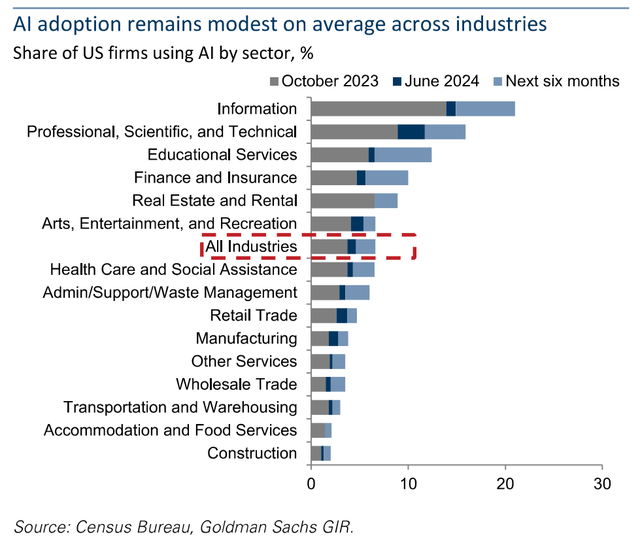

Indeed, the road ahead, circa-2024, looks quite long as industry adoption of AI thus far doesn’t match much of the Wall Street hype.

Source: ZeroHedge

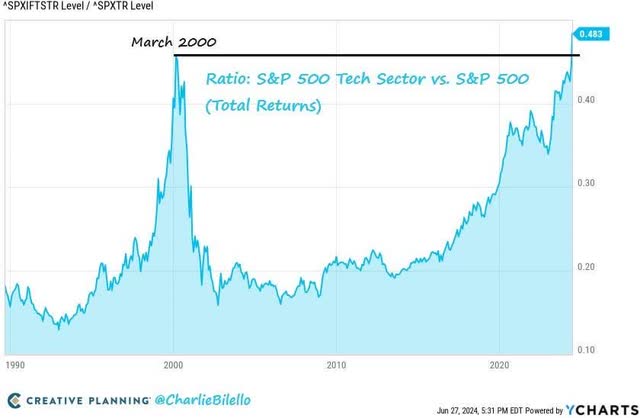

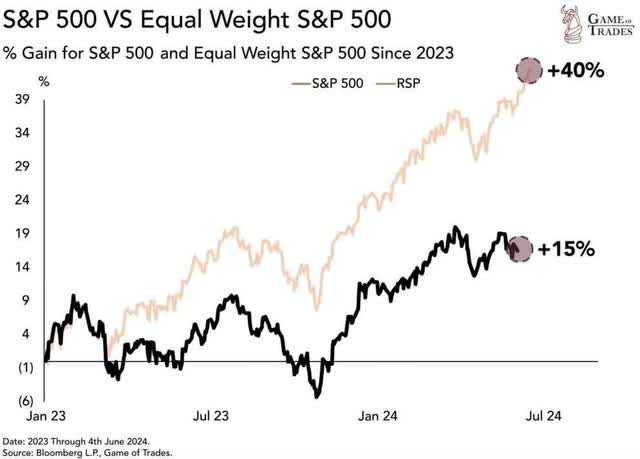

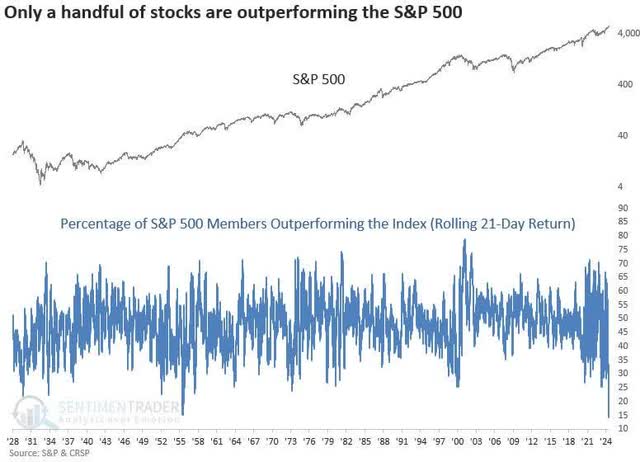

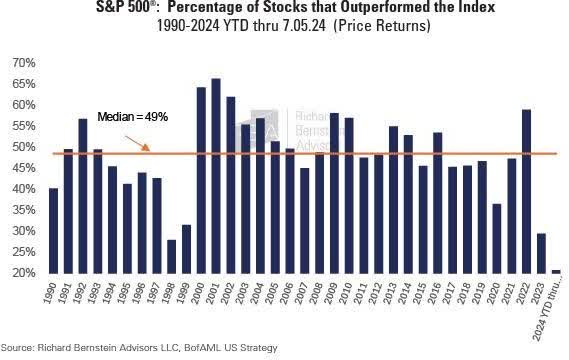

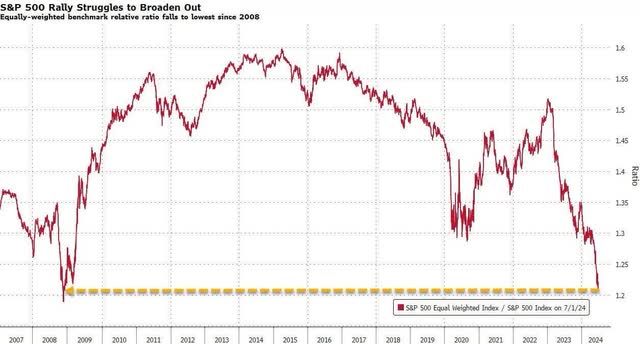

The above charts illuminate the continuing, extraordinary dominance of technology stocks. Please note the last two charts. It goes without saying that our new idea buy list is dominated these days by non-tech stocks.

|

The information and statistical data contained herein have been obtained from sources, which we believe to be reliable, but in no way are warranted by us to accuracy or completeness. We do not undertake to advise you as to any change in figures or our views. This is not a solicitation of any order to buy or sell. We, our affiliates and any officer, director or stockholder or any member of their families, may have a position in and may from time to time purchase or sell any of the above-mentioned or related securities. Past results are no guarantee of future results. This report includes candid statements and observations regarding investment strategies, individual securities, and economic and market conditions; however, there is no guarantee that these statements, opinions or forecasts will prove to be correct. These comments may also include the expression of opinions that are speculative in nature and should not be relied on as statements of fact. Wedgewood Partners is committed to communicating with our investment partners as candidly as possible because we believe our investors benefit from understanding our investment philosophy, investment process, stock selection methodology and investor temperament. Our views and opinions include “forward-looking statements” which may or may not be accurate over the long term. Forward-looking statements can be identified by words like “believe,” “think,” “expect,” “anticipate,” or similar expressions. You should not place undue reliance on forward-looking statements, which are current as of the date of this report. We disclaim any obligation to update or alter any forward-looking statements, whether as a result of new information, future events or otherwise. While we believe we have a reasonable basis for our appraisals and we have confidence in our opinions, actual results may differ materially from those we anticipate. The information provided in this material should not be considered a recommendation to buy, sell or hold any particular security. |

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here

")

")

")

Business Update Conference Call Transcript")