")

British luxury fashion company Burberry Group plc (OTCPK:BURBY) starts off its first quarter (Q1 FY25, quarter ending June 29, 2024) trading update, released in mid-July, with a quote from Gerry Murphy, Chair of Burberry. He says “Our Q1 FY25 performance is disappointing.”

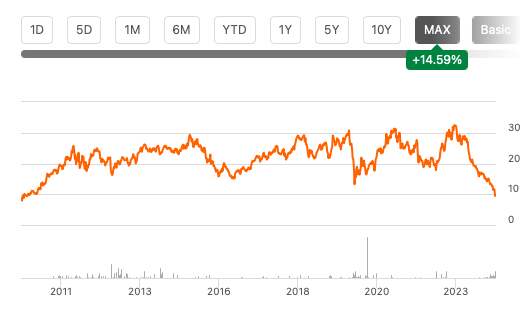

In fact, the performance was so disappointing for investors, that BURBY dropped by 16% in a single day following the update and is now trading near all-time lows (see chart below). It’s down by 42% in the past five months alone, since I last wrote about it in March.

Price Chart (Source: Seeking Alpha)

Awful as the situation is, it’s not a shock. The luxury market has been winding down since last year and has pretty much slowed to a crawl, if that, in 2024 so far. Yet, it’s hard to overlook the fact that over the same time, the S&P Global Luxury Index has declined by a far smaller 11.3%.

This begs the question, why has Burberry seen such a deep decline then?

Exceptionally Weak Q1 FY25 Update

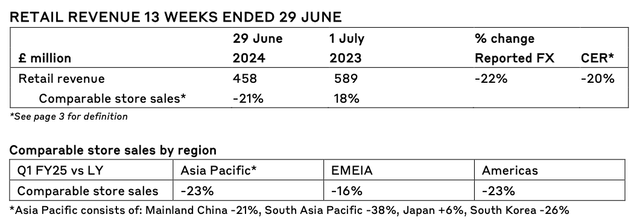

The answer can be found in the Q1 FY25 update, which saw a severe performance downturn. The company reported a huge 20% year-on-year (YoY) decline in retail revenue at constant exchange rates [CER] compared to the slow but still positive 1% YoY growth in the full year FY24 (see table on ‘Revenue by Channel’ on Pg 5 of the link for details). The latest drop in retail revenue in terms of reported exchange rates was even bigger (see table below).

Source: Burberry

A look at the regional distribution of sales, reveals that weakness in Asia Pacific revenues, in particular, was the big reason for the overall decline (see table on ‘Comparable store sales by region’ above). This is in sharp contrast with an above-average growth of 3% in comparable store sales seen for the region in FY24, compared to a 1% fall for the group as a whole. The region is most significant for Burberry as its biggest market, bringing in 44% of the company’s retail revenues in FY24.

Within the Asia Pacific region, a deterioration in China’s appetite for luxury is visible across companies like Hermès International Société en commandite par actions (OTCPK:HESAY) and LVMH Moët Hennessy – Louis Vuitton, Société Européenne (OTCPK:LVMUY) was evident for Burberry too. Comparable sales to the market fell by as much as 21% YoY. An even bigger 38% YoY decline in South Asia Pacific and a 26% fall in South Korean sales also contributed to the region’s weak performance, but it’s safe to assume that in absolute terms, China’s impact was most pronounced.

It really didn’t help that Burberry lost steam in other markets as well. Last year, the Americas, which saw a 12% sales contraction, continued to drop at an even more accelerated pace. Moreover, the EMEIA also joined in compared to a 4% increase seen in FY24.

Weaker Outlook

With the latest numbers being weak, it was to be expected that Burberry also saw disappointing performance for the full year FY25 as well. Specifically, it points to:

- Expectation of an operating loss in the first half (H1 FY25), if the trends from Q1 FY25 continue into Q2 FY25. Going by the overall trends in the luxury market, it’s hard to see the company doing better in Q2 FY25, indicating that an operating loss should essentially be taken as a given.

- The operating profit for the full year FY25 is expected to be below “current consensus”. This is even as it had seen cost savings offsetting the inflationary impact in the second half of the year in its initial outlook.

- While it had expected to see a 25% decline in wholesale revenues in H1 FY25 even earlier, it now expects to see an even bigger 30% fall for the full year FY25 as well. In the overall scheme of things, wholesale revenues aren’t significant, accounting for just 2% of total revenues in FY24. But the projections do indicate the exceptionally poor environment in which Burberry finds itself now.

Dividends, Earnings and Market Multiples

Considering the outlook and the latest performance, the company has now suspended dividend payments. This significantly adds to investor woes, considering that BURBY’s trailing twelve-months [TTM] dividend yield is at almost 8% after the price decline over the past few months.

Still, there could be an upside to the stock if the market multiples have fallen low enough. To estimate BURBY’s forward price-to-earnings (P/E) ratio, I’ve assumed that total revenue will fall by 22% in FY25, the same as the decline in retail revenue in Q1 FY25. The net attributable profit margin is kept constant at the FY24 level of 9.1%.

This results in a net attributable profit of GBP 211 million (USD 270 million) and a forward P/E of 12.7x. This is lower than my estimate of 13.9x when I last wrote about BURBY. But then again, the company’s profit surprised on the downside by almost 20% in FY24. If that were to repeat this year too, the forward P/E would rise to 15.9x. This means, that multiple can actually be less favourable than it was four months ago.

What Next?

With BURBY trading near its lowest levels ever, however, I believe the ship to sell the stock has sailed. For any investor who bought the stock even a month ago, there are in fact significant capital losses to make back. If there were no way out for Burberry, there would still be a Sell case for it.

But there is. The company is witnessing a disproportionate impact of a luxury market slowdown that isn’t sparing even the biggest of companies in the sector. It has been around for a really long time, boasts of distinct and coveted products, particularly its trench coats, and its numbers were relatively all right even until FY24.

I’m inclined to believe that it will see an uptick as the market stabilizes or starts growing again. In fact, I’d go so far as to say that investors with a risk appetite might even make gains over time from Buying it right now and then accumulating it on further dips.

However, for investors with moderate risk appetite, I’m maintaining a Hold rating on Burberry. There’s no point in selling at the current lows, especially when there’s nothing fundamentally wrong with the company. It could take some time to turn around, but there would likely be gains in the medium term.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here