")

Performance and net asset value

|

Quarterly return†: -3.52% |

NET ASSET VALUE PER UNIT AT 30 JUNE 2024†: $1.1016 CD |

|

NET ASSET VALUE PER UNIT AT 30 JUNE 2024†: $1.0938XD |

|

|

† after all ongoing and performance fees. High watermark at 30 June 2024 is $1.1073/unit |

The quarterly report for this period is slightly late – deliberately so. Given that ~25% of the portfolio over the quarter was invested in French listed equities – many of which are global businesses or holding companies which happen to have a manufacturing base or are headquartered in France – it seemed prudent to await the outcome of the recent, hastily called, French election. Given that the eventual out turn was not a realistic consideration three weeks prior, that has proven wise. As we will discuss below, the impact of Macron’s decision on French (and European) equity prices in the short term is providing an increased opportunity set, particularly within our portfolio. From 7 June 2024 – the closing trade date prior to Macron’s decision – to end June, the French market index (CAC:IND) fell 6.5%.

In many ways, French equities were a microcosm of what happened globally over the quarter. European indices fell over 3.5%, but Switzerland rose over 2%. US equities were dominated by the NASDAQ100 rising 7.8% with S&P500 (SP500, SPX) doing just less than half of that return, but indices more skewed to non-tech manufacturing and smaller companies all fell during the period.

The Dynasty Trust NAV fell 3.52% during the quarter – 2% of this decline was the strength in the Australian dollar against virtually all currencies (+3.2% versus € and +2.4% against US$) since we do not hedge currency exposures. The eclectic nature of the top five contributors is a good illustration of the quirky equity environment: Catapult International (CAZGF, +22%, featured below), Avation PLC (+23%), Manchester United PLC (MANU, +21% to sale), Senvest Capital (OTCPK:SVCTF, +19%) and Harworth Group PLC (+15%). Sports data analytics, specialist aircraft leasing, football club, hedge fund and land remediation!

Conversely, we held seven securities which fell 10% or more in the quarter, led by Compagnie de L’Odet (OTCPK:FCODF, -17%, featured below) Magellan Financial (OTCPK:MGLLF, -15%), HAL Trust (OTCPK:HALFF, -13%) and Christian Dior (OTCPK:CHDRF, -13.5%). The 14% fall in Porsche Automobil Holding (OTCPK:POAHY) partly reflected the dividend payment – equivalent to over 5% on the end March price – but also general weakness in the VW complex, notably the P911 (Porsche AG) car maker which fell 25% in the period.

Dynasty Trust’s top twenty positions as at 30 June 2024 as a percentage of net asset value are:

At quarter end, we retain around a 4% cash weighting.

Over the quarter we added new holdings in:

- Société Fermière du Casino Municipale de Cannes (FCMC), owner of two significant hotels and casinos in Cannes, operator of eight restaurants, together with concessions over attaching private beachfronts, as well as a hotel in St Barthélemy in the French West Indies. The company is 67% controlled by Group Lucien Barri è re, a prestigious long-established family-owned hospitality group and 26% by Qatari interests leaving the 7% public float, of a €220m market capitalised company with no net debt, as highly desirable. FCMC has been expanding and consolidating the St Barthélemy interests and we regard the effective valuation of the assets – particularly assessed on a per key basis – as well below any reasonable realisation value; and

- Viel et Cie (VIL.PA), a €622m French company controlled by Patrick Combes which controls two other listed companies: (a) the smaller Bourse Direct (€288m market capitalisation) 81% owned, listed in Paris, which is France’s third largest retail broker but more importantly (b) Compagnie Financière Tradition (CHF1.1billion market capitalisation) 71% owned, and one of the three major global inter-broker dealers, along with TP ICAP Group (listed in UK) and the NASDAQ listed BGC Group Inc. (BGC) CFT is the smallest of the three but has less return volatility and higher returns on capital. Including a 40% stake in the unlisted Swisslife Banque Privé, we estimate the shares trade at >40% discount to fungible value, with some signs that moves are afoot to close this discount.

The two purchases above are not a deliberate attempt to Gallicise the portfolio. Given the proliferation of controlled entities within France, the strong (global) businesses many possess and the low pricing of these companies – especially of late – it is an obvious pond in which to fish.

We have reorganised our Volkswagen Group (OTCPK:VWAGY) holdings to focus on the effective controller, Porsche Automobil Holdings (PAH), given the depressed price of its major investments of VW itself and Porsche AG together with the financial leverage in PAH and discount to NAV.

In this report, we discuss:

- our positions in the two Bolloré holding companies, which account for a combined 7.5% of our portfolio, where the relationship is currently out of sync but announcements after the quarter’s close to merge four companies within the “Rivaud” group – those listed entities controlled by Bolloré but with miniscule floats – suggest to us that Bolloré are getting primed for action early in 2025;

- a separate analysis of the Bolloré controlled company, Lagardère which is replete with corporate possibilities; and

- our position in the sports data company, Catapult International, which (in our view) necessitates a discussion on a tragic event 39 years ago which changed the face of the marketplace for global elite sports, and where we feel some investors still haven’t come to grips with the ramifications – because (stunningly) sport and its ancillaries are generally not publicly traded enterprises.

A nebula in the Bolloré galaxy

In the June quarter, and for much of the past year, our largest position in the portfolio – approximating 13% at 30 June 2024 – has been “long Bolloré”. Not just the company itself, but four separate and distinct positions within the 14 company “galaxy”, each having their own specific thesis, whilst obviously sharing common oversight (except Universal Music Group). They range from the ultimate holding company – Compagnie de L’Odet (Odet) – which owns 69% of Bolloré, but which is itself 35% owned by Bolloré, down to the most remote part of the galaxy, Lagardère, which is 63% owned by Vivendi (held), itself owned 30% by Bolloré. Hence, Odet has an effective ownership of 66% x 30% x 63% or ~12.5% of Lagardère.

All four of the securities, in our opinion, trade at significant discounts to intrinsic value, discounts driven by different influences. Moreover, there are both diverse AND common catalysts to closing these value gaps.

Public market value recognition in the two downstream companies – Vivendi and Lagardère – will be driven by separation of Vivendi into four distinct listed companies1; there is an interplay here with Lagardère in that its book publishing business (Hachette) is complementary to the magazine/online media assets (Prisma) within Vivendi itself. It makes little sense, in our opinion and in that context, for there to be a 37% minority in Hachette for no reason.

However, at this stage, which we believe will change over time, the fortunes of Odet and Bolloré are driven far more by the share price of Universal Music Group (OTCPK:UMGNF), the option value inherent in holding over €6billion of cash, and the ~€3bn value of Bolloré’s 30% shareholding in Vivendi. Any changes in Lagardère and Vivendi offer incremental value to the Odet and Bolloré holding companies. That’s why we feel comfortable owning all four securities.

The existence of a “nebula” in the galaxy is most surprising because this “cloud” resides in the most transparent part of the group – the relationship between Odet and Bolloré. The relative share prices of the two companies have become disjointed over the past year, especially so in the month of June with political emotions running high.

A year ago in this report (QR#2) 27 of its 29 pages covered the Bolloré “galaxy” with a focus on past history in an attempt to glean lessons applicable to the group’s future in its cashed up format – subject to the then completion of the European logistics sale to CMA CGM. Since then, much has happened within the Bolloré empire, virtually none of which can be construed to be negative in nature. Aside from the closure of Bolloré’s logistics sale and subsequent receipt of cash, it’s fair to say that the “action” – and subsequent investor focus – has been on the “downstream” companies which have seen far better twelve-month stock price performance:

|

30 June 2023 |

30 June 2024 |

change |

Benefit to Vivendi |

Benefit to Bolloré/Odet |

|||

|

€ share price |

€ share price |

€mn |

€/share |

€mn |

€/share loop adjusted (unadj) |

||

|

Universal Music Group |

20.35 |

27.78 |

36% |

1359 |

1.33 |

2,446 |

2.09 (0.86) |

|

Lagardère† |

16.41 |

20.70 |

26% |

392 |

0.39 |

||

|

Vivendi† |

8.41 |

9.76 |

16% |

419 |

0.36 (0.15) |

||

|

Bolloré† |

5.71 |

5.48 |

-4% |

||||

|

Compagnie de L’Odet† |

1554 |

1304 |

-16% |

1,688 |

to Odet 299 (256) |

||

| † held in East 72 Dynasty Trust Loop adjusted removes self-control loop and cancels relevant shares |

Since this time in 2023, UMG has continued to grow at well above average rates; rolling 12-month adjusted EBITDA (we’ll call it “earnings” which is sloppy but adds back stock-based compensation which can vary quarter to quarter) has grown a handy 10.8% in the year to 31 March 2024 – down from the near 20% annual growth rates of late 2022. But this metric is now running at €2.44billion, with consensus expectations of €2.65billion for the 2024 calendar year. UMG has benefitted from a register where 60% of the shares are locked up in four hands – including Bolloré 18% and Vivendi 10% – but also the fascination with “moated” stocks.

Consequently, allowing for a significant €900million appreciation in UMG’s stake in Spotify (6.457million shares or 3.3%) UMG’s EV2 has moved from €38.2billion to a current €50.8billion over the course of the last twelve months: from 16.1x forward “earnings” (see above) to 19.2x.

The 36% appreciation in UMG’s price is equivalent to €1.33 per Vivendi share, roughly equating to the €1.35 change in Vivendi’s share price, suggesting none of the other positive factors within Vivendi – the proposed split, ongoing growth in profit – have been of significance. As we discuss below, we don’t view that as being realistic. It’s even worse for Bolloré where the increased UMG price is worth an effective 37% increment over the share price a year ago (dissolving the self-control loop with Odet) or 15% assuming full capital participation.

A year ago in QR#2, on pages 26 and 27, we tabulated estimates of the value of Bolloré at €13.15 per share; the tabulation showed a near perfect symmetry in netting off the value of the energy distribution business, storage systems and films plus assorted investments against the capitalised value of holding company costs. At this stage, therefore, we feel it is reasonable to simplify Bolloré down to an effective four-line table. Hence, after solving for the self-control loop, which we estimate reduces Bolloré capital from 2,850million shares to an estimated 1,156million, we can arguably simplify Bolloré down as follows:

|

As at 30 June 2024 |

€million |

Comments |

|

Cash (net) |

6,248 |

Deconsolidation as per December 2023 report |

|

Universal Music Group (18%) |

9,056 |

326m shares at €27.78 |

|

Vivendi (~30%) |

2,928 |

300m shares at €9.76 |

|

TOTAL |

18,232 |

€15.77 per share |

Hence at end June 2024, we view Bolloré as trading at a 65% discount to NAV, well above the prevailing discounts of ~40% of other European family-controlled conglomerates; more pointedly, the discount has blown out nine percentage points in a year despite the removal of transaction closure uncertainties and a 36% lift in the price of its largest investment.

If that is perplexing, the situation with Compagnie de L’Odet is even more the case, especially as at the June 2023 AGM, Chair Vincent Bolloré was noting the very low price of Odet; at 30 June 2024, it had fallen 14% from then.

A year ago (page 27 of QR#2), we calculated based on Bolloré’s then market price, that Odet was trading at around a 5% discount to market value NAV (€1554 against mid-point NAV of €1634). The same calculations at 30 June 2024 show that Odet has slithered away to close on a 20% discount to NAV at Bolloré’s market value:

|

€million |

Eliminate SCL† |

Don’t eliminate |

Comments |

|

Bolloré shares (€13.15) |

9,368 |

10,900 |

1,709m shares on elimination; 1,989m shares with SCL |

|

Vivendi shares (€9.76) |

54 |

54 |

5.5million |

|

UMG shares (€27.78) |

172 |

172 |

6.2million |

|

Debt |

(430) |

(430) |

Via deconsolidation |

|

TOTAL NAV |

9,164 |

10,696 |

|

|

Issued ODET shares |

5.649m |

6.586m |

|

|

NAV/share |

€1622 |

€1624 |

ODET price €1304 = 19.6% discount at Bolloré share price |

|

† self control loop |

So we have a holding company trading at a 20% discount to an intermediate holding company with effectively three investments, which itself trades at a 65% discount to real NAV. We value Odet at over €4,700/share on the current asset base – 260% above the prevailing market price. Given the massive optionality with Bolloré’s cash hoard and the clear desire of the group to commence the process of simplification and value extraction, there are few other low-moderate risk investments with such upside, anywhere on the planet.

Lagardère: only a minor possibility the business is properly valued

We have held a position in Lagardère for over eight months after the shares fell away whilst Vivendi waited for approval for its takeover offer. Vivendi already owned 27.6% of Lagardère and agreed to acquire Amber Capital’s 17.5% stake on 16 December 2021 and lodged takeover documentation on 21 February 2022. The takeover offer could not be finalised until Vivendi met two regulatory conditions, being to divest its Editis book publishing business and “Gala” magazine; these conditions were finally fulfilled in November 2023. As a result of the length of the offer, Vivendi closed the offer and granted accepting shareholders “transfer rights” to transfer their shares to Vivendi at the bid price of €24.10XD once the requisite conditions were met. In December 2023, it was agreed that the transfer rights would be extended to 15 June 2025, being a date by when Lagardère will announce its first full year results under Vivendi’s control. There was a maximum of 28m transfer rights outstanding and we believe around 23.5million still exist, mainly under the control of Arnaud Lagardère (the Chair) and Bernard Arnault (see below)

The present shareholder structure, with Vivendi having acquired ~63% of Lagardère, Arnaud Lagardère holding 8%, Financière Agache (Bernard Arnault) 8% and Qatar Holding 11.5%. When excluding an employee share plan, there is only a 7% free float of this €3.1billion market capitalisation company.

Lagardère has two different but desirable main businesses where there are very few pure-play exposures globally:

- general (as opposed to technical/legal) book publishing where it is the second largest global participant; and

- travel retail where the business is the second largest convenience retail operator within travel and the fourth largest duty free participant.

General book publishing is high return on capital but relatively slow growing and with occasional volatility; conversely, convenience travel retail is a stronger long-term growth story, but is currently experiencing an aggressive upswing as travel returns to normality – and growth – post COVID. There is NOW no logical fit between the two businesses (there certainly once was), and they are likely to find different homes once Vivendi splits into four constituent parts. Lagardère also has some minor press, entertainment management and radio interests, the most desirable of which – the venerable magazine Paris Match – was sold to LVMH for €120million in May 2024.

Lagardère is now inexorably linked to Vivendi, not only via the majority ownership but Vivendi’s provision of an initial ~€1.5billion debt line, required as a result of Vivendi’s takeover triggering early debt repayments. These loans have been refinanced to the tune of ~€1.3billion with external banks, and Vivendi making a €650million loan available, which has assisted in new revolving credit facilities being granted to Lagardère3.

Whilst nothing is ever obvious within the confines of the Bolloré empire, it does seem clear that the prevailing structure is highly sub-optimal. Parts of Lagardère would be best taken into 100% ownership to enable the creation of the envisaged publishing and distribution arm of Vivendi; however, we sense no long-term desire for Bolloré to own travel retail; it doesn’t fit neatly – other than as an investment – within the envisaged “new” Vivendi. But the travel retail business is a highly desirable asset which in our view has significantly greater value than that attributed by the accounting expert4 (€2.2billion) opining on the Vivendi acquisition or the independent expert5 (€2.04billion). Moreover, the Bolloré group’s desires appear to be to retain book publishing, since it fits within their own personal landscape, but also has financial attributes the group have historically found attractive.

This makes the investment case for Lagardère very attractive: there is effectively a Vivendi “put” – a value below which the shares are unlikely to fall, but in our view significant upside as the travel retail business will find a new home, either as part of a separate spin; at worst retained within a listed, rerated Lagardère which is very much the downside case or far more likely, sold to a third party. Private equity and Middle Eastern sovereign wealth (or a combination) would be obvious buyers given their other interests (past and present) in the sector.

Why is it unlikely that Lagardère is appropriately valued?

There are eight overriding reasons for Lagardère shares to be mispriced:

- there is only a 7% free float (worth €220million) significantly restricting non-passive institutional investors from building a position; there is some offset by the fact that excluding past management and Bolloré, the two remaining significant external investors are astute judges of value, within strong global businesses, and have not made any type of overture to sell into the Bolloré offer;

- An uncertain strategic role for Lagardère within the Vivendi separation initiative – does it stay as a listed entity and on what basis? None of the Vivendi communications are clear about the role of travel retail, whilst regarding book publishing as a key asset;

- Vivendi’s offer to extend the transfer rights to 15 June 2025 creating confusion for longer;

- Career risk: the shares have long been regarded as a “dog” and currently trade 67% below the levels of early 2006 and nearly 30% below end 2009 – why bother?;

- The ongoing role of Arnaud Lagardère, the son of the founder (below) who was banned from holding executive roles on 30 April 2024 as a result of an indictment against him relating to events in 2018 and 20196; Arnaud Lagardère resumed his posts as Chair and CEO on 28 June 2024 after the partial lifting of the management activities ban M. Lagardère has recently sold ~4.2million shares to Vivendi to assist in the repayment of personal loans to Credit Agricole7 (OTCPK:CRARF) but has a checkered reputation (see “background” below);

- As we discuss below, there are very few publicly listed cohort companies in either of Lagardère’s key businesses – the major general publishers are either privately owned, recently acquired by private equity or are part of a wider media conglomerate. There are publicly listed pure publishers such as John Wiley (WLY) or Scolastic (SCHL) but they thrive in specialist, technical areas. There are cohorts in travel retail, but as we discuss, the space covers everything from pure duty free to pure food service;

- IFRS16, being the accountants’ revenge on securities analysts, by turning the simple – paying rent in cash – into the complex – discounted value calculations with discount rate unwinds is bad enough in many companies. In the travel retail industry it is nightmarish, with amounts paid to airports by the retail concession holders being a mixture of fixed rent (subject to IFRS 16), minimum guaranteed rent (subject to IFRS 16) plus expensed turnover related costs, and percentage of turnover which is not subject to IFRS 16 and just charged as an operating expense. Hence, the use of EBITDA is nonsensical since it includes only the variable rental component as a cost. Bluntly, how many analysts are going to make the effort to do comparative analysis with only a 7% free float?? This encourages us to use operating cash flow adjusted for lease payments as a guide to profitability, with due regard to capital expenditure.

- Extensive use of joint ventures and equity accounted/partly owned companies within travel retail; Lagardère has four 50/50 joint ventures, notably with AWPL in Australia and the Pacific, SNCF (French Railways) and Lyon Airport which have revenue of ~€760million (100% basis) but modest disclosed profits. Even more meaningful are the equity accounted associates with ADP (Aeroports de Paris) where Lagardère has 44% of the company which operates 140 stores at CDG and Orly plus 50% of the company operating the convenience retail. As a guide, turnover was ~€914million in CY2023.

Lagardère’s storied background

We don’t have time to write a book; to do justice to Lagardère’s history virtually demands it, with interwoven links with Bolloré and Arnault, a mini-history of French manufacturing, Formula 1 cars, aerospace- the antecedent of Airbus (OTCPK:EADSF) – and the current businesses. It’s when you examine “storied” – not always for the right reasons – conglomerates like these that you understand why there are numerous hidden treasure troves for the astute acquiror to pick over.

The book publishing business Hachette was founded by Louis Hachette in 1826 after the purchase of a Parisian bookstore, moving rapidly into book publishing. As long ago as 1900, Hachette launched bookstores on the Paris Metro, an early evolution of “travel retail”. Over the next 80 years, Hachette expanded overseas, created new publications – notably “Elle” – and remained owned by the Hachette family.

In 1981 Hachette was acquired by Daniel Filipacchi and Jean-Luc Lagardère; Lagardère was the CEO of Matra8, an aerospace, transportation and vehicle business which diversified into weapons systems and electrical equipment. Lagardère pursued a conglomerate strategy under the Matra name, despite being heavily focused around vehicles. The company entered Formula 1 in 1968 – for only one season – but provided the cars for Tyrell’s 1969 championship winning season driven by (Sir) Jackie Stewart9.

In 1992, the shareholdings in Hachette and Matra were pieced together under the banner of Matra Hachette, with “Lagardère”, the current entity, being the largest shareholder; Lagardère moved to full control in 1996. In 1999, the technology business was merged with Aérospatiale, then in July 2000 with CASA (Spanish aircraft) and Germany’s DASA aerospace to become EADS – the direct predecessor of the current Airbus.

The Lagardère “entity” had been created as an SCA10 en commandite par actions – French version of a partnership, with general (managing) partners (Lagardère himself) and limited partners (effectively shareholders); this gave Lagardère complete control with less than a 10% stake. The entity issue became more important when Jean-Luc Lagardère passed away in 2003; his only son, Arnaud Lagardère, became the Managing Partner of Lagardère SCA. Arnaud reversed the strategy of his father and sold off the manufacturing and aerospace interests and embarked on a strategy of investing in wider media (including a 20% stake in Canal+ at one stage) as well as sports and sports management.

In 2013, Lagardère sold its final stake in EADS (Airbus) – realising ~€2.3billion for the sale of 61.5million shares; these shares are now worth ~€7.9billion11 suggesting the decision left nearly 180% of the current market value of the whole of Lagardère on the table from this single transaction.

Source: tikr.com

These decisions plus money losing investments in sports set the scene for an ongoing decade plus of share price stagnation. In 2016, event driven European investor, Amber Capital, became a shareholder, building to above a 16% stake by March 2020, establishing a website “strongerLagardère.com” and putting forward a slate of 8 new directors12 and 16 resolutions, at a time when the share price was below €10. Six months prior, Lagardère had filed suit for significant damages alleging its shares had fallen significantly due to Amber’s campaign.

By mid 2021, M. Lagardère had been backed into a tight corner by Amber Capital’s 20% stake but Vivendi’s building of a 29% stake in the group throughout 2020 and 2021; despite a capital injection from Bernard Arnault to his personal holding company, the attempt to effectively pit Vincent Bolloré against Bernard Arnault in pursuit of Lagardère could not eventuate13. The SCA structure was removed in June 2021 by shareholder agreement at a cost of ~€200million (10million shares to the general partner), and eventually Vivendi buying out Amber Capital (subject to takeover).

With the sale of “Paris Match” to LVMH, M. Arnault has achieved something tangible from the exercise. We now move to the final stage of development with the likely break-up of Lagardère to fit the Bolloré/Vivendi agenda. We content that is not priced into the shares.

What could Lagardère be worth?

We view the best approach to valuing Lagardère as a sum of the parts, with the knowledge that in a Vivendi-driven dismemberment, the book publishing business will be spun off, to be preserved by Bolloré’s amazing sense of history in a new company named Louis Hachette Group14. This may require Vivendi to sell off the travel retail business within Lagardère, perhaps deal with the radio assets and bid for the 37% minorities. That is an easier proposition if the minority shareholders can SEE the fungible value of travel retail – which they presently can’t – as well as reducing the size (after a capital return?) of the required bid by Vivendi to acquire the minority position. Whilst Financière Agache and M. Lagardère both own transfer rights, the knowledge that travel retail could be worth far more than previously, aside from M. Lagardère’s emotional attachments to the business suggest negotiations with each of the key parties are likely. Qatar Holdings haven’t shown their hand other than not to accept the €25.50 (cum dividend) or €24.10 (ex-dividend) offers.

Travel retail: likely worth more than “independent valuation report”; significant rebound in progress

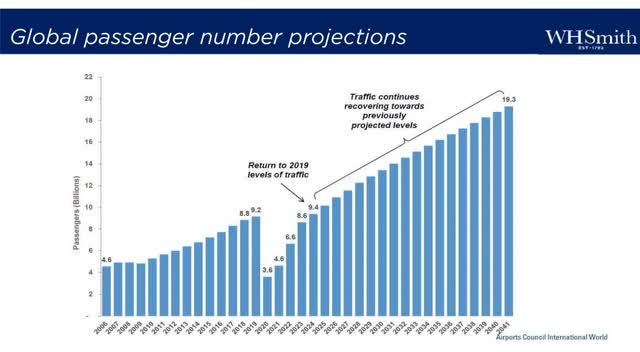

In our view, travel retail is an exciting business opportunity, which lends itself to sophisticated statistical analysis against a very simple equation: revenue = passengers x per pax spend. The more folks travelling, by ferry, cruise ship, train and plane, the greater the revenue opportunity. The key is to continue to unlock each passenger’s wallet which is where the analysis comes in. Most of our analysis is focused on airports since around 9.4 billion people use planes each year, with a positive demographic of younger people travelling more freely to more places using lower cost carriers and the various on-line methodologies to book and travel. Not forgetting demographically advantaged boomers…

Source: WH Smith plc Final Results presentation 9 November 2023

The sophisticated statistical analysis is all about trends, and how to maximise the selling potential of very expensive monopoly real estate within airports. Three of the listed companies – Avolta (OTCPK:DUFRY), WH Smith (OTCPK:WHTPF) and SSP Group (OTCPK:SSPPF) are (rightly) fanatical about formats, entry to new locations and the data analysis that underpins this. Somewhat stunningly, when we analyse Lagardère’s cohort and despite the complexity of the accounting, there is little differentiation between the pricing of the publicly listed companies or the underlying margins that they obtain.

In the two reports accompanying the bid documentation, we noted that travel retail was valued at a midpoint ~€2100million by Sextant Expertise and 8 Advisory. We think things have moved on from there given the merger of Dufry with Autogrill to form the Swiss-based Avolta and the strong growth reported by the four major listed players in revenues in the immediate past.

We believe travel retail is a highly attractive business where consolidation of the industry on a global basis is leading to enhanced returns as passenger numbers grow rapidly as a rebound from COVID restrictions. Somewhat surprisingly, there are few publicly listed plays within an industry which investors would immediately recognise as being part of individually inherent monopolies, with significant pricing power – how often have you complained about the price of food, beverage or even a chocolate bar at an airport, anywhere on the planet?

We noted earlier that there are significant accounting issues in evaluating the cohort companies due to IFRS16; our focus is to look at segmental operating cash flow after lease payments which strips away most of the accounting issues, and to also be cognisant of capital expenditure which is a recurring contractual and expansionary item.

There are significant segmental differences within travel retail, with the business broadly dissecting into essentials (where Lagardère are the global leader in airports only), duty free and foodservice. Surprisingly, given that duty-free alone is a US$40bn+ global industry, there are few publicly listed peers within the industry. There is realistically only one direct comparative to Lagardère being Avolta (AVOL.SW) which has exposures to all the three main groupings, but there is merit in assessing three other listed entities:

Comparative sizes as at 30 June 2024

|

€billion† turnover |

shares |

Price (LOC) |

Eq. Cap (€mn) |

Debt (€mn) |

Ent value |

Outlets (#) |

Duty free |

Food |

Essentials |

|

Avolta |

150.4 |

€34.90 |

5,250 |

2,705 |

7,955 |

5100 |

4.90 |

4.64 |

4.09 |

|

Lagardère‡ |

Part of larger diverse group (analysis bellow) |

5120 |

2.19 |

1.56 |

2.02 |

||||

|

W H Smith† |

129.9 |

£11.32 |

1750 |

520 |

2,270 |

1270 |

1.74 |

||

|

SSP† |

796.0 |

£1.48 |

949 |

736 |

1,685 |

2900 |

4.10 |

||

|

China Tourism Duty Free† |

2068.9 |

K$47.9 |

11,619 |

(3,600) |

8,009 |

>200 |

5.56 + 2.81P |

||

|

DFS Group |

LVMH & Robert Miller; not separately disclosed |

420 |

4.00 |

||||||

|

Heinemann |

Privately owned – Heinemann family (Germany) |

500 |

3.60 |

||||||

|

Duty Free Americas |

Privately owned – Falic family (USA) |

200 |

1.94 |

||||||

| † £1=€1.19; €1=RMB7.95 €1=US$1.09 ‡ excludes joint ventures and associates |

Cohort valuations coalesce at historic EV/OCF of ~9x

The following tabulation assesses the four cohorts to Lagadere travel retail by examination of operating cash flow minus lease payments and comparison with capex over recent periods – trailing twelve months or estimates in the case of Avolta; it should be noted that the European companies are heavily seasonal with profits in the “summer” April – September period:

|

LOCmn |

Avolta (€mn) |

CTS Duty Free (RMB mn) |

SSP Group (£mn) |

W H Smith (£mn) |

|||||

|

CY2022 |

CY2023 |

CY2022 |

CY2023 |

year 9/23 |

TTM 3/24 |

year 9/22 |

year 9/23 |

TTM 2/24 |

|

|

Revenue |

6,878 |

12,790 |

54,296 |

67,075 |

3,009 |

3,209 |

1,400 |

1,793 |

1,862 |

|

OCF |

1,590 |

2,531 |

7,675 |

9,936 |

498 |

507 |

219 |

302 |

316 |

|

Leases |

(1,035) |

(1,883) |

(670) |

(711) |

(251) |

(258) |

(107) |

(137) |

(141) |

|

Net OCF† |

555 |

848 |

7,005 |

9,225 |

247 |

249 |

112 |

165 |

175 |

|

NET margin |

8.0% |

6.6% |

12.5% |

12.6% |

8.2% |

7.8% |

8.0% |

9.2% |

9.4% |

|

Capex |

(95) |

(396) |

(213) |

(746) |

(220) |

(251) |

(70) |

(106) |

(112) |

|

Free cash flow |

460 |

452 |

6,792 |

8,479 |

27 |

(2) |

42 |

59 |

63 |

|

Ent Value |

7,954 |

68,905 |

1,796 |

1,907 |

|||||

|

EV/Net OCF |

9.4x |

8.1x |

7.2x |

10.9x |

|||||

|

† before working capital changes |

There are various distortions to margins and multiples in the table above, notably:

- Avolta’s full acquisition of Autogrill did not close until July 2023, which results in significant revenue growth into CY24 and will see higher CY24 margins;

- SSP Group is in the midst of aggressive expansion of its food service outlets, which is constraining margin and adding to capex; the company has however, flagged midpoint revenue of £3.45bn for the year to September 2024;

- WH Smith still retains 514 “High Street” shops with £470m revenue & equivalent margin

Applying the cohort to value Lagardère Travel Retail at €3.35 billion

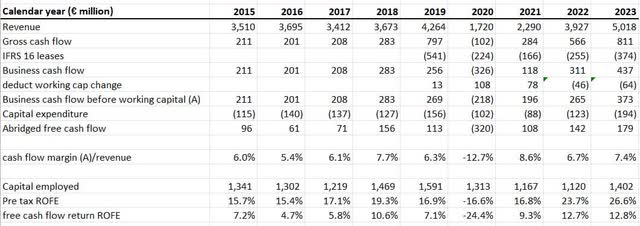

Relevant financials for Lagardère travel retail over a nine-year period are tabulated below:

We note, the significant recent growth in revenue which has attracted a stable, now slightly increasing margin and high return on funds employed despite >€100million in capital expenditure each year. Margin out-turn is consistent with Avolta but marginally below WH Smith.

The outlook for 2024 appears very bright at this junction, although there are some mixed signals in respect of the upcoming Olympic Games which will cause clear distortions. Based on growth in H1 2024, with revenue in travel retail some 13.5% above Q1CY2023 like for like, but 18.0% on a reported basis including acquisitions, we expect full year divisional revenues to hit €5.8billion, with increased cash flow margin around 7.8% – results consistent with WH Smith earlier this year. This suggests full year business cash flow around €450million, just over 20% above that of 2023.

Lagardère’s main peer, Avolta will also record significant growth because of a full year of Autogrill; based on consensus analysists estimates, we expect revenues of €13.6billion in CY2024, which at a 7% margin would yield business cash flow of €954million for 2024.

On this basis, with a 30 June 2024 enterprise value of €7,954million, Avolta trade at 8.3x forward business cash flow, not dissimilar to CTS Duty Free. Applying a similar multiple to Lagardère Travel Retail would provide a gross valuation of €3.7billion – close to 70% above the highest of the independent valuations in the Vivendi takeover documentation. Even apply the cohort’s 9x business cash flow valuation to CY2023 numbers would yield a value around €3.35billion for this unit.

Book publishing

Lagardère Publishing is, in our estimation, the world’s second largest general book publisher, with revenues of around €2.8billion per annum, about 60% of the size of Penguin-Random House, owned by the German Bertelsmann Group. Book publishing is a relatively slow growth business – Lagardère revenues have grown 4.5% pa CAGR over the past five full years – but is a high cash flow, high return on capital business. In CY2023, the Lagardère business generated pre-tax, pre-interest cash flow of €229million on revenue of €2.8billion, and then invested €64million for free cash generation of €165million. With the intellectual property of publishing knowledge, past libraries and access to distribution – of all types – these assets are prized for their long term “investment” properties; corporate transactions in the sector (when they occur) tend to be at relatively high prices.

A brief comparison of the “Big 5” general book publishers is given below:

|

€million |

Owners |

2023 revs |

|

Penguin Random House |

Bertelsmann (family) |

4,532 |

|

Hachette & other units |

Lagardère |

2,809 |

|

Harper Collins |

News Corp |

1,830 |

|

MacMillan |

Holtzbrinck (family) |

est. 1,060 |

|

Simon & Schuster |

KKR |

est. 1,057 |

The US$12billion in revenue carved up by the five majors has caused issues in respect of corporate transactions. The US Justice department successfully won a lawsuit (filed November 2021, deal terminated November 2022) to prevent Bertelsmann acquiring Simon and Shuster, when put up for sale by its previous owner, Paramount in November 2020. Bertelsmann had offered US$2.175billion versus the 2021 EBITDA earnings base of $216million, but Paramount was forced to accept an offer of (effectively) $1.62billion by KKR, pitched at around 8.2x EV/EBITDA .

The regulatory intervention shows the potential future difficulty in dealing at the higher end of the publishing market; the stumbling block for the merger related to the alleged two-thirds market control of acquisition of publishing rights in the US, post a merger. Given Lagardère’s French (and non English) language publishing and its #4 size in the USA, there may be more flexibility regarding an eventual merger with another top 5 player.

In February 2022, US listed Houghton Mifflin Harcourt (HMHC) agreed to be acquired by Veritas Capital Fund VII at $21 per share being an equity capitalisation of $2,682. The company, a major supplier of school books under contract, held net cash of $146million at end December 2021; the enterprise value of $2,535million equated to 9.4x 2021 adjusted EBITDA of $270million, being a 16.8% margin on revenue.

Valuations of book publishers and estimated value of Lagardère publishing

The passive trading multiples are below those applied in the last two corporate transactions in the sector, involving acquisitions of businesses with roughly $US$1billion revenue bases. There are three listed “pure” book publishers of any significance; however, the two US based and listed entities have significant specialisms in technical and learning (J. Wiley and Sons) and €2.8billion childrens’ books (Scholastic); the smaller UK listed Bloomsbury Publishing, famous for being publishers of the “Harry Potter” series:

|

Scholastic |

J. Wiley & Sons |

Bloomsbury Publishing |

|

|

SCHL (US$million) |

WLY (US$million) |

BMY (£million) |

|

|

Contract education & children |

Technical, education & research |

General |

|

|

Shares issued |

28.21 |

54.4 |

81.44 |

|

Price (30/6/2024) |

$35.47 |

$40.70 |

6.26 |

|

Market capitalisation |

1,000 |

2214 |

510 |

|

Net debt/(cash) (ex-leases) |

(79) |

684 |

(66) |

|

Enterprise value |

921 |

2,898 |

444 |

|

Forward year revenue |

1,440 |

1,670 |

343 |

|

Forward year EBITDA |

170 |

395 |

50 |

|

Margin |

11.8% |

23.6% |

16.2% |

|

EV/EBITDA |

5.4x |

7.3x |

8.0x |

We view Lagardère Publishing as a significantly appealing business, with potential merger possibilities within the Big 5, most likely Simon and Schuster, once it is liberated under the Vivendi separation program. Comparisions of Lagardère’s performance to that of Bertelsmann and Harper Collins, suggest a higher end multiple could be attained on an IPO.

The Independent Accountant and Independent Expert in the Vivendi takeover documentation15 attributed (mid-point) values of €3.25billion and €2.87billion respectively, averaging out at €3.06billion. Lagardère has performed better than Harper Collins over the past six years, but not quite as well as Penguin Random House (Bertelsmann) with the “Big 3” posting ~5%pa revenue CAGR over the period at average EBITDA margins of over 14.5%:

Source: Lagardère, News Corp & Bertelsmann annual reports

We are aware that an 8.2x EV/EBITDA multiple for the sale of Simon & Schuster was a distressed or pressured sale by the vendor. However, the use of the hefty premium Bertelsmann were prepared to pay is not appropriate. We believe in a passive valuation as part of the Vivendi separation, a multiple of 9x EV/EBITDA is reasonable, being above Bloomsbury but below the takeover of HMHC. On that basis, we view Lagardère Publishing as being worth €3.35billion. It is noteworthy that return on invested capital in the division is over 23% pre-tax leaving open the opportunity for a private equity buyer to participate and leverage the business, in a similar fashion to KKR in Simon & Schuster should a full sale be contemplated. This isn’t a situation that we believe the Bolloré family would contemplate.

Other assets

The radio and entertainment assets, licences for “Elle”, “Journal du Dimanche” are largely incidental, especially after the sale of “Paris Match”. Most of these assets are in a SCA structure with M. Lagardère as the general partner, which gives a hint, in our opinion, that they will go with him once other sales from Lagardère are made.

We are happy to take the Independent Accountant (€308million) and Independent Expert (€290million) views of value and deduct the €120million sale price of “Paris Match”, which was well above the estimates of either. That suggests the traditional media and entertainment assets to be worth ~€180million.

Sum of the parts valuation: €32.40

Our sum of the parts valuation of €32.40 per Lagardère share is tabulated below:

|

€million |

Comments |

|

|

Travel retail |

3,350 |

9x business cash flow as defined |

|

Book publishing |

3,350 |

9x EV/EBITDA per analysis above |

|

Other assets |

180 |

Independent experts less “Paris Match” sale |

|

Capitalised costs |

(126) |

9x central costs of €14 million |

|

Net debt |

(2,100) |

June 2024 = €2,255 but seasonal peak |

|

TOTAL |

4,564 |

|

|

Per share |

€32.40 |

30 June share price €20.70 represents 36% discount |

We have NOT applied a holding company discount since we view Lagardère as likely being dissected as part of the Vivendi separation which makes the significant passive valuation very appealing.

Global sports economics changed in May 1985: International catastrophe to Catapult International

This may appear a lengthy preamble, but in our view is essential to understand why the environment for media rights – the lifeblood of professional sport – across elite, in-demand sports will not change in the foreseeable future. We acknowledge that “in-demand” sports will change with occasional fads and strong marketing (eg. F1) but can’t see changes in the key ball-based sports.

On 29 May 1985, Liverpool FC played Turin’s Juventus16 for the (soccer) European Cup Final at the decrepit Heysel Stadium in Brussels, Belgium. Flimsy walls, chicken wire fencing and antipathy between the sets of supporters, with an inability to maintain a “neutral area”, led to sectional invasions, a wall collapse and the death of 35 fans, of whom 32 were Italian. Various subsequent enquiries and legal actions led to the conviction of 14 Liverpool fans for manslaughter.

Given the night occurred only ten weeks after a notorious FA Cup game between Luton and Millwall with extreme fan violence broadcast on UK delayed replay TV17 and just over two weeks after the death of 53 people in the Bradford City (Valley Parade) stadium fire, English football’s reputation had reached its deep nadir. Then Prime Minister Thatcher – hardly a sports fan – needed no prompting to take action, requesting the English governing body, the Football Association (‘FA’) to withdraw English clubs from European competitions. UEFA, the European football governing body, needed no second invitation and banned English clubs from competing in Europe indefinitely.

The impact of this ban and the way it played out over the next six years, specifically in the city of Liverpool and in North London – the latter the home of two of England’s best supported teams, Arsenal and Tottenham Hotspur – set the scene for enormous change in football broadcasting in England. American readers may struggle to comprehend that this transition, wrought on the dingy terracing of English football grounds, directly led to the transformation in US sports broadcasting from late 1993.

Rupert Murdoch celebrated his 93rd birthday in March. He also got married for the fifth time in June. There is a brilliant irony in that he married a lady whose daughter was formerly married to a man who assisted the significant growth in Mr. Murdoch’s net worth18. Murdoch has revolutionised many areas of film and media which have had significant impacts on investment markets, and his own net worth. Outside of the sale of the Fox assets to Disney (DIS), completed in March 2019, two quintessentially Australian aspects have driven the value of his fortune over recent years: property and sport. Property via the astonishing growth of the REA portal in Australia, the 61% shareholding in which comprises an exact 61% equivalent (approximately US$10.4billion) of the enterprise value of News Corporation (NWS).

Whilst investing in property and its ancillary activities has many publicly listed avenues, in theory, the same cannot be said for sports. This is changing, at an increasing pace. Why? Because of the recognition – notably by some of the world’s wealthiest people – of the ramifications of a tragedy 39 years ago and a decision made just over 32 years ago in England. Stunningly, in our opinion, it has taken nearly THAT long, at least to work out the subtleties of the decision. In this correspondent’s view, it is Murdoch’s most brilliant (not necessarily most lucrative) decision in his illustrious business career – which he repeated less than eighteen months later to blindside a group of US executives and magnify the impact of BOTH decisions. “You don’t beat live football with old movies”.19

The story which unfolds is the background and rationale to the massive tailwind of elite global sports revenues, why a return to the past is unlikely and why the US$331mn market capitalised Australian sports data analytics company, Catapult International, is in a marvellous position – if it can execute.

Creating a global media monster: the English Premier League: 15.5%pa compound revenue growth for 30 years

At the time of the post-Heysal European ban, English football had two “governing bodies” who didn’t get along: the overriding body: the FA and the Football League (‘EFL;), which organised regular season English football into four leagues from 1958 – 1992 with 92 teams, relegation and promotion, based on season ending positions. The European club competition ban financially pressured the English clubs, together with a Thatcher Government which wanted nothing to do with the game. As is the case with Brexit, Continental Europe happily got on with its (football) life with the folks across “La Manche” living off their past glories; European teams strengthened and pillaged the EFL of some of their best players. Every single British transfer record20 from May 1984 to June 1992 involved the player moving from a major UK club to Italy, France and Spain, as the record transfer fees escalated from £1.5million to £5.5million:

|

Month |

Player |

Selling club |

Buying club |

£million fee |

|

May 1984 |

Ray Wilkins |

Manchester United |

AC Milan (Italy) |

£1.5 |

|

May 1986 |

Mark Hughes |

Manchester United |

Barcelona (Spain) |

£2.3 |

|

August 1986 |

Gary Lineker† |

Everton |

Barcelona (Spain) |

£2.8 |

|

June 1987 |

Ian Rush |

Liverpool |

Juventus (Italy) |

£3.2 |

|

July 1989 |

Chris Waddle |

Tottenham Hotspur |

O. Marseille (France) |

£4.25 |

|

July 1991 |

David Platt |

Aston Villa |

Bari (Italy) |

£5.5 |

|

August 1991 |

Trevor Steven |

Glasgow Rangers |

O. Marseille (France) |

£5.5 |

|

June 1992 |

Paul Gascoyne |

Tottenham Hotspur |

Lazio (Italy) |

£5.5 |

|

† Top scorer in the 1986 World Cup |

The exclusive TV rights for the top division of EFL (then called First Division) were won by the commercial TV network in the UK (ITV) for four years from 1988-1992, involving the showing of live games, at a cost of £11million per season. There was a strong focus on a small number of clubs, and an effective “Big 5”21 teams shown regularly started to emerge. In late 1990, representatives of the Big 5 met with the largest of the ITV franchises with a view to significantly lifting the value of TV rights on the expiry of the deal.

Unknown to many, the Big 5 had the backing of the FA whose relations with the EFL were strained; the Big 5 were frustrated by their need to share the TV revenues across all 92 clubs in the EFL, resulting in their best players being picked off – as shown above at hefty prices – to play overseas.

The Big 5 started to garner other support from the top division to break-away from the EFL in order to retain this TV revenue and in July 1991, 18 First Division clubs with the backing of the FA, resigned from the EFL, effective from the conclusion of the 1991-2 season. The ability to do so was ratified in the UK High Court in August 1991 and the apparatus to run the new English Premier League (‘EPL’) put in place. From late 1991, an assortment of media companies had started to assess the economics of bidding for the EPL rights, with the full knowledge that higher levels of rights payments – exclusively to the EPL teams – were the sine qua non of the new league.

Between March – May 1992, the EPL negotiated with the various parties for the new season commencing in August 1992. There are numerous public accounts of the discussions involving two bidders – ITV and B Sky B – Rupert Murdoch’s merged cable/satellite TV business, then losing significant amounts of money and with no real “pull” for viewers.

With the First Division’s expiring contract at £11million per season, the bid for the EPL rights gradually escalated towards £34million per season. However, with guidance from close lieutenant Sam Chisholm and enthusiastic backing from Alan Sugar22 – the founder and controlling shareholder of Amstrad PLC – the major supplier of satellite dishes, Murdoch put in place the “Blow them out of the Water” strategy that has become the playbook for his operations from Italy to the USA.

The advice was given by Sugar – with the full knowledge by all that he would be a double beneficiary if Murdoch won, since he was also the largest shareholder in Tottenham Hotspur – but there was clear recognition that this was the content that would build Sky, as a network and rapidly accelerate the path to subscriber growth and profitability as “must have” content for the average UK resident. On 18 May 1992, Murdoch bid £304million for five seasons (60 live games a year) of EPL (~£60million a season, a 450% increase), way beyond the ambit of ITV.

In mid-December 1993, only eighteen months later, Murdoch used the same strategy to build a network – Fox – in the USA, using the differential economics of network building versus incumbency to massively overbid CBS, the incumbent broadcaster of the National Conference (NFC) in the NFL paying US$250m a year, but willing to go to $295million, by paying just on $400million a season for a four year deal. The magnitude of this strategy can be seen against the renewed bid of NBC for the less attractive23 American Conference (AFC) rights of $250m per annum for four years24,25.

Sky PLC was eventually sold to Comcast for £29.7billion in 2018 as part of the Disney acquisition of Fox.

Over time, it has become clear that these strategies are vitally dependent upon the attraction of the sport and league and the size of market into which it is being broadcast; second tier simply doesn’t work from an economic standpoint which is why certain European streamers – notably Viaplay – have failed. Folks in Sweden don’t want to watch the Scottish League Cup.

The strategy continues to be replicated in differing areas; in Australia, the second largest telecoms operator, Optus26 who in late 2015 bought the EPL rights for three seasons, forcing aficionados to subscribe to a new streaming platform, but with significant preferential deals for the telecom customers. There has been a significant focus on football, and the company retains the EPL rights through the conclusion of 2027/2028 season, along with other European leagues (LaLiga, Bundesliga).

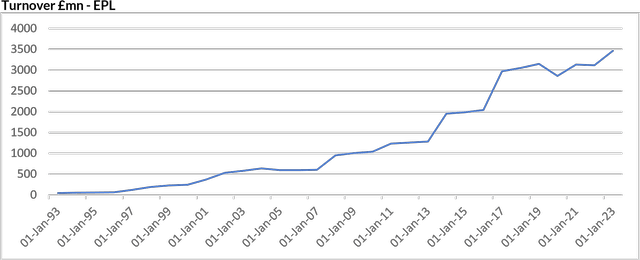

Since the creation of the EPL in 1992/3, the turnover of the company which owns the EPL27 has ballooned from £45.7million in the year to 31 July 1993 to £3,466million in the fiscal 2023 period – 15.5%pa compound growth over thirty years.

Unlike many other sports and leagues, the reason for the strong growth in EPL turnover is the sale of the foreign rights in separate jurisdictions, notably North America, Asia but also Europe. EPL now derive more for the global rights (~£1.7bn a season) than the domestic rights (~£1.67bn per season).

What makes this possible is, of course, the advent of streaming for sport which enables more broadcast participants to enter the race for “fragments” of the sports league’s rights (say Friday night or Monday night). It does mean that most major sports require fans to have at least two separate subscriptions should they wish to watch every game.

Elite sports media deals – for the biggest globally relevant events continue to provide an increasing torrent of money for participants; the US NBA has this month signed off on a series of deals amounting to US$76billion over 11 years with Disney, NBC, Prime, and TNT, a necessity given the sheer number of games28, which are predominantly broadcast locally

Five key landscape changes to global elite sports

With a focus on football – the leading global sport for these trends – we see five key landscape changes over the past fifteen years:

- Emergence of sovereign wealth, UHNW and private equity as club and league owners In August 2008, Sheikh Mansour, deputy prime minister of United Arab Emirates, based in Abu Dhabi, acquired Manchester City FC from the former Thai Prime Minister, Thaksin Shinawatra for an estimated £200million. Whatever your author’s distaste for City29 what has now morphed into “City Football Group” is at the forefront of two key aspects of global football: the trend towards multiple ownership of clubs under one banner and the introduction of private equity funds not club ownership. City Football Group (CFG) owns significant stakes in twelve clubs (including the parent), providing opportunities for young players to be developed in four corners of the globe, loaned out and transferred for profit or development reasons. This is the underpinning of the pinnacle club – Manchester City – for decades to come. US private equity firm SilverLake acquired 10% of CFG in 2019 for US$500million, since increasing its stake to 18%. Since “Abu Dhabi” made their move, the Government backed Qatar Sports Investments acquired Paris St Germain for €70million in June 2011; in December 2023, the US sport investment group Arctos Partners acquired a 12.5% stake in PSG for an effective 100% value of €4.25billion. In October 2021, the Saudi Public Investment Fund (80%) led consortium acquired the EPL’s Newcastle United for £300million. The same month, Saudi’s Public Investment Fund formally launched LIV Golf, the “breakaway” golf league which has paid significant one-off sums to attract top golfers to its organization. Private equity has full or partial equity ownership in numerous sports teams in USA and Europe, notably France. CVC Capital actually owns a 13% stake in Ligue 1’s media rights business30 Recently depleted in value by Vivendi’s Canal+ failing to bid for the next four seasons TV deal which has halved in value – don’t mess with Bolloré and SilverLake has a 33% stake in Australa’s A-League. Only 2 EPL teams – Brentford and Brighton – are now controlled by owners born in the UK.

US UHNW or private equity ownership in EPL – 2024/25 season

|

American |

EPL team ownership |

US sports participation |

|

Wes Edens |

Aston Villa (smaller co-owner) |

Milwaukee Bucks (NBA) |

|

Stan Kroenke |

Arsenal (100%) |

LA Rams (NFL), Denver Nuggets (NBA), Colorado Avalanche (NHL) |

|

Bill Foley |

Bournemouth (majority) |

Las Vegas Golden Knights (NHL) |

|

Todd Boehly/Clearlake Capital |

Chelsea (managing owner) |

LA Dodgers (MLB) |

|

John Textor |

Crystal Palace (40%) |

other non US soccer teams |

|

David Blitzer |

Crystal Palace (18%) |

|

|

Joshua Harris |

Crystal Palace (18%) |

|

|

Shahid Khan |

Fulham (100%) |

Jacksonville Jaguars (NFL) |

|

ORG/Bright Path Sports |

Ipswich (60/40) |

– |

|

John Henry/Tom Werner (Fenway Sports Group) |

Liverpool (100%) |

Boston RedSox (MLB), Pittsburgh Penguins (NHL) |

|

Silver Lake |

Manchester City (18%) |

|

|

Glazer Family |

Manchester United (54% economic) |

Tampa Bay Buccaneers (NFL) |

-

Players Individuals rock up to play for several hundred million (US) dollars over multi-year contracts; at the elite level, it’s usually $25-45million a season for star players in conventional leagues, with the occasional outlier.31 Why conventional leagues? Because in 2023, the world seemingly changed again with a new “out of the universe” competition in the overriding global sport – soccer – via the Saudi Pro League. In 2023, three of the top six best paid sportsmen32 were banked with Saudi money – Christiano Ronaldo (#1, football, US$276million), Jon Rahm (#2, golf, $203million) and Neymar Jr. (#6, football, $121million). In a sign of the times as to how globally elite sports matter, of the Top 15 male sports earners, only 2 came from US NFL, but 4 from the globally booming NBA, 5 from soccer (add in Messi, Benzema and Mbappe), 3 from golf plus F1’s Max Verstappen.

-

Sports betting: There has been significant liberalisation and widening of sports betting. In a very sad development, on a Saturday night in Sydney, Australia I can place bets on Norwegian Third Division football as well as the Estonian Second Division. As a guide, EIGHT of the 2023/24 EPL teams had shirt front advertising gaming sponsors, mainly offshore firms; these will be phased out by the start of the 2027/28 season.33 Aston Villa, Bournemouth, Brentford, Burnley, Everton, Fulham, Notts Forest, West Ham. Aside from computerised platforms, apart from mug punters, this expansion of sports betting demands just one thing: data – see below

-

Changing media distribution: To watch live EPL games, the UK based supporter needs three streaming services – Sky Sports, TNT (the old BT Sport) and Prime (Amazon). In the USA, to watch live NFL takes in SEVEN networks (the three traditional FTA plus Fox, Prime Video, ESPN and the NFL’s own NFL Network). The NFL pulls in $10billion a year in media rights.

-

Women and college: On both sides of the Atlantic, women’s sport is taking off in attendances, interest and media spend. Particularly in the US, there have been past resurgences in women’s sports competitions, but the increasing fragmentation of media outlets is providing more “space” for the broadcasting of female sport. Consequently, many of the sports are creating their won audiences, further heightened by genuine younger female interest in having their own sporting heroes. Rightly or wrongly, the advent of women’s sport does depend on the marketability of the star players; but with adroit use of social media, at both team and individual level, it suggests that the growth in professional female sport will have greater longevity than past phases. In the author’s opinion, no where is this more demonstrable than women’s football, where the strongest national teams in the world are truly from four corners of the globe, differ significantly from the men’s rankings and are in high income countries.34 This comes together in phenomenal competitions like Women’s Super League (EPL equivalent) with 60,000+ crowds for major games at large stadiums35 and greater mainstream coverage. In May 2024, NCAA – the organising body for US college sports – agreed to settle antitrust cases to settle lawsuits regarding lack of sharing of media revenues with players; more importantly, players can be paid directly by their colleges for playing. Given that college football (gridiron) attracts significant viewers – around 1.7million per game on ESPN with peaks for the biggest match-ups of 5-7million (cf. average NFL game of 18million and Superbowl at >100million). With the advent of a 12 team national college football playoff and US$1.3billion annual broadcast deal with ESPN signed in March 2024, it appears likely increased rights money will flow to the colleges and players.

Where do you put your bucket in this torrent of media rights money?

The astonishing aspect of elite sports is that there are so few realistic avenues – at present – across global markets to invest in the “business”. Consequently, we sense that investors in some of the few exposures that do exist have (in our view, they may disagree) surprisingly poor knowledge of the key drivers. Moreover, elite sports in the key area where publicly listed equities lack a role, has already been categorically supplanted by private equity in areas such as leagues Ligue 1, A- League and large scale teams.

From a public company standpoint, aside from investing in the smartly run media rights owners, such as Fox or Vivendi, or over the top streamers, we believe there are five ways to invest in the ongoing growth of elite sport:

- Invest in sport itself or league: There are two avenues to invest directly in the sport or controlling body of the sport:

- Formula 1 Group (FWONK) part of Liberty Media (market cap: ~US$18billion)

- TKO Group Holdings (TKO) owners of UFC and WWE “combat” sports (Market Cap: ~US$8.5billion)

- Invest in sports teams: There is a myriad of publicly traded sports teams, mainly soccer in Europe. These securities have universally been lousy investments since most are controlled companies, either by families or by a “mutual” mechanism. Most clubs end up spending windfall media/competition profits badly on expensive sub-par players, which then causes a second round of loss making to rebuild. The two best known publicly listed teams – Manchester United (MANU) and Juventus (OTCPK:JVTSF) – have both fallen into this category. One of this year’s European Champions League finalists, Borussia Dortmund (OTCPK:BORUF), is also listed but most German clubs have a “communal” feel to them (massive attendances, low ticket prices) with stability rather than profit maximisation a key ethos. Glasgow Celtic (OTCPK:CLTFF) are not hamstrung by on-field performance or attendance, more by the tiny media deals for Scottish football and failures to advance in European competition. Dynasty Trust has owned MANU in the past, which was a low risk play on the substantial sale of a trophy asset, which did not materialise in the manner we hoped. These scenarios are usually the reason to invest in teams.

- Invest in sports wagering: There are several significant listed sports wagering companies, with the UK based entities Entain (OTCPK:GMVHF) and Flutter (FLUT) having morphed from their roots as bookmakers on horse-racing. In the US, whilst Flutter owns FanDuel, the major listed players have their genesis as genuine sports bookmakers rather than horse racing. The largest entities like DraftKings (DKNG), Penn Entertainment (PENN) Caesars Entertainment (CZR) and MGM Resorts (MGM) are either part of larger casino owning combines or offer casino games. Most have been modest investments over a three-to-five-year period, with increased competition, general lack of a moat and requirement to spend increasing amounts of money on advertising. All have been growing revenue, but have been donating increasing amounts to……..these guys:

- Invest in (oligopoly) data suppliers: There are two significant publicly listed data suppliers who share an effective near-oligopoly of data supply to sports bookmakers from major leagues around the world, as well as providing data and graphics feeds to sports media broadcasters, again on a licensed basis: Sportradar, a Swiss company listed on NASDAQ (SRAD); and Genius Sports, a UK based company listed on NYSE (GENI). Both have had enormous revenue and cash flow growth over the past five years but have been extremely mediocre investments because of the high pricing of their IPO’s. Each company has exclusivity arrangements with major leagues around the world, for which they pay handsomely. The two have slightly different balance sheet accounting, with the upfront cost of the arrangements being amortised each period. SRAD carries a significant intangible and offsetting “lease-type” liability in contrast to GENI. Both are avid users of “adjusted EBITDA”, which for once, has reason and relevance. A tabular encapsulation is given below. Given the significant decline in equity price alongside growth of the businesses and entrenched positions, both companies have started to attract a coterie of quality, growth type investors, alongside the founder shareholders. GENI has been hard hit by the exit of a cornerstone PE shareholder, Apax Partners, who sold out this month, and the fact it went public via a SPAC. The founder, Mark Locke still owns ~9% of the company, with NFL having warrants over ~8.6% of the capital. GENI has the benefit of the rapid growth of in-game wagering which is growing rapidly in NFL (around 25% of bets) and its prevalence in EPL (80%) of bets, which offer significantly higher margins than pre-game wagering, which partly accounts for the higher revenue growth over the past five years. SRAD has a very constrained share register, with a Swiss-style arrangement of the founder, Carsten Koerl holding Class B shares, which represent 1/10 th “A” share from an economic standpoint, but have full voting rights36 giving Mr. Koerl 82% of the votes. The ~208million tradeable “A” shares are close to 81% owned by four shareholders – CPP Investment Board (Canada) (38%), Technology Crossover Mgt (16%) and a further 7% held by a single fund leaving around a US$450million free float. The two companies represent an effective intermediator between media rights paying companies, bookmakers and the sports themselves. With the US wagering market still deregulating and at an early stage of growth, the two companies arguably represent a higher quality play on that growth versus the sportsbetting companies themselves.

|

US$millions |

SRAD |

GENI |

|

Sports league betting data exclusives |

MLB (ex-US), NBA (ex- China), NHL, ATP (tennis), CONMEBOL (football), UEFA, FIFA, F1, Bundesliga, |

EPL, FIBA (basketball), MLB, NFL, CFL (Canada) |

|

Market Cap. |

3,335 |

1,330 |

|

Debt/(cash) |

(274) |

(167) |

|

Enterprise Value |

3,061 |

1,263 |

|

Revenue guide 2024 |

1,144† |

490 |

|

Adjusted EBITDA guide 2024 |

220† |

82 |

|

EV/adjusted EBITDA |

13.9x |

15.4x |

|

Revenue CAGR (5ys) |

22.5% pa |

33.7% pa |

|

IPO price |

US$27.00 (September 2021) |

US$19.00 (June 2021) |

|

price & ∆ from IPO |

US$11.19 (-59%) |

US$5.60 (-71%) |

|

† Converted from € at US$=€1.09 |

5. Invest in must have technology: In our view, investing in the technology and data analytics software the teams (or sports) must have is a further, high quality source of annuity-style revenues and profitability. The problem? There is only ONE publicly listed global company in the area, where the sports technology business is really meaningful. Catapult International Limited. It’s based in America, but incorporated and listed in Australia, which has largely kept it out of the ambit of US investors. That has been to the Dynasty Trust’s benefit since it has been one of our top few holdings for over a year, having started acquiring shares at A$0.78 against the 30 June 2024 level of A$1.89.

Catapult International: a high quality “pick and shovel” play on elite sports

[Note: Catapult releases significant data from a SaaS perspective on a group basis, and management financial data on a divisional basis. For obvious competitive reasons – see later – the company is guarded regarding contributions by sport. We choose to assess the company with regard to cash flow rather than EBITDA given significant R&D investment in intangibles, which are fully disclosed by the company. We encourage readers to with additional interest to consult Catapult’s results presentations available at www.catapult.com]

Background and volatility of operating and share price performance

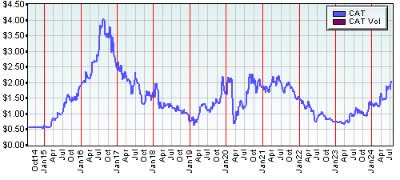

Catapult has 262m shares on issue, trading at $1.895 at 30 June 2024 for a market capitalisation of A$496mn (US331million) with no net financial debt.

We believe it is one of the most misunderstood companies listed on ASX. It has few sell-side analysts, who in any event can only spend limited time on the company, given their other commitments. There is a need to disaggregate the accounts and reconcile cash flow, which takes some degree of time, and the company has differing margins across its three main businesses (including media). There is no publicly listed cohort, and the unlisted competitors (especially Agile Sports Technology – “Hudl”) guard their financials and IP closer than nuclear launch codes.

More pointedly, we see few analysts who have a comprehension of what’s happening with sports media and the long-term high growth in revenues to elite sports/sports teams. That’s why we have spent significant space in explaining why we don’t believe this is a trend which will be under meaningful pressure, though inevitably there will be abatements of growth rates from time to time (eg French football post the recent TV “deal”).

Bluntly, we have rarely seen an industry environment so conducive to a company’s growth; so it’s simply down to Catapult management to execute. As we discuss below, past management hasn’t always done so, and there remain significant sceptics in Australia regarding the business. Interestingly, outside of the management shareholdings, there are a group of slightly unconventional investors who hold major stakes in the company, reflecting (in our opinion) their greater knowledge base of the underlying drivers. This is not a conventionally institutionally owned company.

Catapult was founded in 2006 after the conclusion of Government funding at Co-operative Research Centre for Microtechnology in Melbourne which was working with Canberra’s Australian Institute of Sport combining inertial sensors with GPS tracking. The technology was placed into a company backed by the two founders Shaun Holthouse and Ivor van de Griendt plus outsiders Dr Adi Schiffman and Calvin Ng. The first three of these individuals remain on the board of Directors with substantial holdings (or having established funds with these holdings).

Catapult International: share price performance from IPO

The early focus of Catapult was around “wearables” – trackers worn by players which measure all aspects of their performance, notably speed, acceleration and positioning. This has morphed over recent years, notably from 2021 onwards sophisticated integration with video analysis and predictive technologies, to provide greater tactical insight for coaches based on player performance.

Catapult’s first sales were to Australian domestic sports37 (AFL, rugby league) but rapidly grew to overseas organisations. Until 2021/22, the model was ostensibly a capital equipment sales-based affair which meant that the company was free cash flow positive by 2020 on ~3,000 team clients. In addition, from 2016 (via acquisition) the company targeted the “prosumer” market – amateur athletes keen to measure their performance in a more sophisticated manner. The scaling down of efforts in this market have been one important component to recently improved financial performance.

Catapult IPO’d in December 2014 raising A$12million at A$0.55 (proceeds to company) with a market value of A$66million. The shares advanced sharply over 2015 with a succession of league and team client wins and closed the year at A$1.90. Further earnings upgrades and local enthusiasm for one of the few “technology” companies with strongly growing revenue saw the shares double again in seven months to hit A$4.00 in August 2016.

The strong rise in the shares enabled Catapult to cement a merger with the US based XOS Technologies, in July 2016, being the first of two company changing acquisitions since listing, Catapult had been engaging in partnerships with XOS since June 2015, and the A$80million acquisition instantly added 143% to Catapult revenue, bringing with it 66% of NFL teams, college basketball and football plus over 66% of NHL teams. XOS was the “missing link” with digital video solutions specifically designed for gridiron and with media applications. Catapult funded the acquisition via part acceptance by the vendors of scrip plus A$100million worth of equity issued to shareholders and new owners at A$3.00 per share.

Over the next five years, Catapult shares were buffeted by an assortment of profit warnings (early 2019) unexpected capital raises (A$25million at $1.10) in March 2018, COVID fears (not realised) and a cynicism by investors regarding the company’s “prosumer” strategy – selling to smaller, non-elite teams.

In June 2021, what should have been the death-knell for prosumer was signed with the acquisition of the London based SBG Sports Software, the second company changing acquisition. SBG was acquired for US$45m split in half via cash and shares; the company raised a further US$40million via placements and share purchase plans at A$1.90. SBG and the motorsports clientele – teams, F1 and NASCAR – is a KEY differentiator versus its competitors.

SBG brought significant expertise in video solutions based around analytics from motor sport, notably Formula 1, which was capable of being adapted to “field” sports to provide real time insights into performance. SBG accelerated the integration of “wearables” – now known as “Performance and Health” – with video analysis, “Tactics and Coaching” which is significantly higher margin. Pre-acquisition by Catapult, SBG’s key sports of football, rugby and motorsport were generating gross margins of 96% and brought a whole new market (motorsport) and clients (Mercedes, BMW, F1 race control) into Catapult.

The excess equity raising was designed to invest US$17million in technology and product plus drive the business away from capital sales to a 100% SaaS model. As with virtually every other “capital” to SaaS transition we have observed, it took longer and losses were greater than investors anticipated.

We have made adjustments to Catapult’s stated results to illustrate clearly that the company lost over US$43million in negative cash flow in the two years to March 2023, implementing the integration of SBG, new products, business growth, still pursuing the prosumer strategy for a period, and most importantly, transition the business to a full subscription model.

It is over this period that investors lost confidence in the company, simply because the losses were so high against a reduced equity capitalisation of ~US$165million (at say 90c and f/x of 0.7) and with the company carrying US$20million of debt, from Western Alliance Bank.38

Catapult International: Key pre-tax metrics as adjusted by East 72 Management

The table above adjusts historic key components of Catapult’s results from IPO, modifying:

- All metrics to US$ at relevant exchange rates for the period prior to 2020;

- Adjusting disclosed operating cash flow for investment in intangibles (effectively R&D) plus payments for leases to bring the business onto a proper operating cash flow/burn basis;

- Noting capital expenditure to obtain a “free cash flow” from business; and

- Building in Catapult’s own disclosures of annual contract value at the end of the period and a rough approximation of team numbers.

The turning point