")

")

Investment Thesis

Quite possibly one of the best value plays out there in my opinion, Bancolombia (NYSE:NYSE:CIB), trades at a very cheap 5.5x FWD earnings with a solid dividend yield of 10%, according to Seeking Alpha. To any bargain hunter this stock is incredibly attractive due to its strong fundamentals, solid profitability, and cheap valuation. Colombia continues to show an overall improving macroeconomic scene as it slowly rebounds from the pandemic, with lowering government expenditures helping reduce inflation. Overall, Colombian banks are expected to hold steady as the overall economic scene improves, leading me to rate shares of Bancolombia as a buy.

Company Overview

Like any bank, the core of Bancolombia’s business is to take deposits at a low rate and lend them out a higher rate and make the net interest spread. The company describes itself as a “growing, profitable organization with almost 30,000 employees and present in Colombia, Panama, Guatemala and El Salvador”. With over 30 million customers, Bancolombia “delivers its products and services through its regional network comprising Colombia’s largest non-Government owned banking network”.

Bancolombia has operations in several countries as mentioned before, and recently they have been transforming most of their services digitally. They offer digital services like Nequi, A la Mano, and other digital credit cards with strategic partners to expand their digital scope and presence. In some sense, banks are becoming more and more technologically oriented company and I view Bancolombia’s digital investments as highly attractive in order to keep their services competitive.

Investor presentation

Aside from traditional consumer banking and corporate banking, Bancolombia also participates in the capital markets through investment banking services, trust and fiduciary services, and even insurance. Investors can see that Bancolombia is heavily diversified and handles many financial activites throughout the Latin America region.

Profitability has been quite consistent as ROEs have been pretty high, at 17.4% as of Q1 2024 according to the investor presentation. I have never seen a bank so profitable yet so cheap, which makes me believe people are missing this story completely. The company has a strong track record of digital innovation, attracting and retaining customers, and handling their loans for profitability.

Overall, with several awards given to Bancolombia for its local market expertise and sustainability achievements, I believe management is very high-grade and can run this banking group extremely profitably for shareholders. Its profitability should continue to hold up as the bank tightens its loan book and continues to invest heavily in digital initiatives to stay above the competition.

My conclusion is that Bancolombia should continue to remain one of the top market leaders in the Latin American banking space and its diversified business allows it to weather storms resiliently while still maintaining a strong balance sheet. The dividends continue to increase steadily while the stock continues to misprice the fundamental strength and earning power of this banking conglomerate. Therefore, my analysis reveals a proper buying opportunity for those who like cheap banking stock in emerging markets.

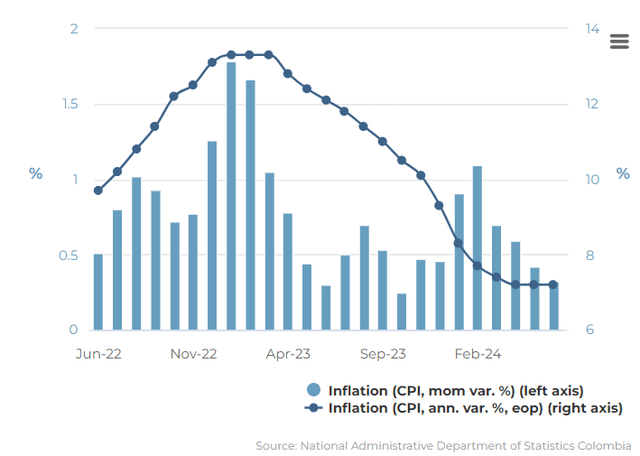

Colombia’s Inflation Begins To Drop

The banking sector is heavily tied to the overall economy, so it’s worth looking at the overall macro scene in my view to analyze the potential tailwinds Bancolombia has. In my opinion, the most notable improvement recently is the fall in inflation for Colombia, according to the World Bank “Macroeconomic imbalances that surfaced during a strong post-pandemic economic recovery are correcting rapidly, with declining inflation and fiscal and external deficits”.

Focus Economics

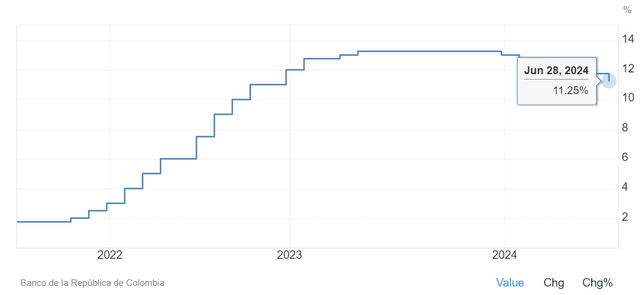

With inflation slowly getting under control, interest rates in Colombia no longer need to be that high, and are potentially going to be cut which should stimulate Colombia’s economy. Interest rates are now at 11.25%, down from the peak of 13.25% which signals to me that rates are now headed in the right direction to improve Colombia’s economy. Overall, an improving inflation trend allows central banks to slowly cut rates, leading to more spending and money circulation and overall GDP growth in my opinion.

Trading Economics

I believe the financial sector is set to rebound and banks like Bancolombia are set to be a major beneficiary of this economic trend. Going forward, I expect earnings to hold up and potentially increase as further rate cuts incentivize people to borrow more money, encourage more capital markets and investment activity, and reduce the cost of deposits for Bancolombia. This should allow net interest margins to expand and lead to stable or higher ROEs for Bancolombia.

Going Digital

Bancolombia is investing heavily in its digital presence, which in my view explains why they’ve been so successful by innovating new products and services that the Colombian public are eager to use and integrate in their daily lives. For instance, in the transcript management announced,

On the business development front, we are pleased to share the recent launch of Wenia, a Bancolombia’s investment in a digital asset company.

By utilizing innovative technology, Wenia serves as a bridge between traditional financial system and the expanding digital economy. Initially Colombian residents will be able to engage in the buying, selling, converting, receiving and sending of digital assets such as Bitcoin, Ether and USBC in a swift and secure manner.

Wenia is a interesting initiative that shows management is potentially getting interested in cryptocurrencies and the blockchain technology to improve their banking business. For those who are believers in crypto, this example further shows that management is highly innovative and making bold bets on going digital. This new COPW coin is apparently a stablecoin that is backed by Colombian pesos, “and provides Wenia customers with the ability to seamlessly move in and out of fiat to cryptoassets within the Bancolombia Group ecosystem” according to the press release.

It looks like Bancolombia is not shying away from new digital technology, including crypto. Although crypto has had its fair-share of historical controversy, I think this is a nice initiative that puts more power, flexibility, and control into the hands of Bancolombia’s customers. It also does not undermine the Colombian central bank as the COPW is backed 1:1 to the Colombian Peso.

In any case, what this means is that Bancolombia is becoming more technologically advanced which should create shareholder value through more customer satisfaction and thus higher retention. Colombian citizens now have access to more secure and efficient transactions in the digital economy, giving them more confidence to save, invest, and borrow money through Bancolombia’s institutions. Overall, going digital can be seen as a major positive for shareholders in my opinion.

Valuation – $48 Fair Value

I believe a simple and effective way to value the company is through earnings, using projected ROEs to forecast earning power. Assuming shareholder equity remains flat at around $9.5 billion and ROEs of around 10%, earnings should come in at around $1 billion, rounded up.

I think equity will flatten out because of an improving interest rate environment which should accelerate borrowing, leading to higher loan originations and an expanding loan book. ROEs should remain around 10% in my view due to improving efficiency and a flattish equity base. Management’s own guidance is more optimistic and confirms my ROE forecast of at least 10%,

We keep our 6.8% guidance with regards to net interest margin adjust our cost of risk from 2.4% to 2.6% as Vintages continues performing better, adjusted efficiency ratio to 15% area and maintain our ROE forecast around 14% and core equity Tier 1 ratio of 11% area.

So, there’s evidence to believe that profits can come in at least $1 billion annually, assuming equity holds flat and ROEs stick around 10%. Divide $1 billion by shares outstanding of 258 million gets me EPS of $4, rounded up. Apply a sector median 12x FWD P/E multiple to $4 gets me $48 per share. The stock is undervalued by a significant margin and presents good long-term upside to those who believe in Bancolombia’s earnings power.

The dividends here are very attractive, with the most recent quarterly dividend being $0.898. This annualized out gets investors over 10% yield, assuming the dividend holds up. For income investors this stock looks attractive as management seems keen on paying dividends for now. So far the dividend shows no sign of stopping, and may continue to keep up which handsomely rewards investors for waiting.

Risks

Emerging markets have political risk and currency risks that investors should be aware of. If the Colombian Peso depreciates significantly, it translates into less USD which impacts the earnings for Bancolombia in USD. Runaway inflation could reverse course and set earnings on fire as a weaker Colombian peso translates to less USD earnings.

Regulators may restrict the digital advances Bancolombia is making, as the Wenia initiative allows retail users to trade Bitcoin, Ethereum, and other cryptocurrencies. The Colombian government may regulate this area because it could deem it a risk to the public. In any case, future unfriendly regulation could make Bancolombia’s digital investments impaired as banks are heavily scrutizined by the SFC.

Competitors may ramp up their digital investments and steal market share from Bancolombia. Furthermore, there is talk about how the Colombian government is financially strained, with budget deficits requiring Colombia’s financiers to either raise taxes or cut spending, which may dent the economy in the near-term.

Buy Bancolombia

This high dividend yielding bank stock is attractive with a cheap valuation, strong profitability, and strong digital presence in the Latin American banking sector. I believe Colombia is on the rise, and their economic growth should translate into solid long-term earnings power for Bancolombia. The group is well diversified with many segments in many regions, which should help it perform resiliently during recessions. At 5.5x FWD earnings the stock is way too cheap and should be bought, giving investors solid income and potential capital appreciation.

Read the full article here

")

Stock: Still Time To Buy On Deep Value")