")

")

MarineMax, Inc. (NYSE:HZO), the boat dealership operator, reported the company’s Q3 results on the 25th of July, showing a surprisingly good performance in the challenged industry backdrop. With the results beating Wall Street estimates by a notable margin, the stock went up by 17% on the earnings day.

I previously wrote an article on the stock, titled “MarineMax: Extensive Acquisitions Could Prove Themselves Promising”. In the article, published on the 18th of October in 2023, I initiated MarineMax at a Buy rating due to the stock’s attractive valuation considering the accretive M&A strategy. After the article was published, MarineMax’s stock has now returned 23% compared to S&P 500’s similar return of 25% despite macroeconomic worries pushing earnings down further than was expected in late 2023.

My Rating History on HZO (Seeking Alpha)

Q3 Report: Light at the End of the Tunnel

MarineMax’s Q3/FY2024 results, reported on the 25th of July, surprised the market very positively – the revenues of $757.7 million beat Wall Street estimates by a wide $37.4 million, and the adjusted EPS of $1.51 beat by $0.14 in the seasonally important quarter. Comparable store sales managed to increase by 4% year-on-year in the quarter.

Especially the reported earnings were good in my opinion, as operating income only fell by -18.2% from the prior Q3 after a Q2 year-on-year decline of -61.4%. MarineMax successfully stabilized its gross margin more from higher-margin boat sales.

The performance is still in a pressured macroeconomic environment with the boating industry seeing a very large decrease in demand, making the results great. MarineMax has already had to lower its guidance both in Q1 and Q2 from an initial $225-250 million adjusted EBITDA range in Q4 into the current $155-190 million range, now reaffirmed with the reported Q3 results. The reaffirmed guidance expects a mid-point adjusted EBITDA of $45.9 million, up from $42.6 million in the prior Q4. While the reaffirmed guidance points towards a mid-point improvement already, I believe that as a base scenario, MarineMax will hit the lower bound of the wide guidance range still.

M&A Speculation Arises

At least two parties have potentially become interested in MarineMax’s assets – first, OneWater (ONEW) was speculated in early June to be interested in acquiring the company with immense potential synergies between the companies, with a privately made offer of $40.00 per share. Afterwards, Island Capital Group [ICG] offered to buy back MarineMax’s yachting and marina business, which the company sold to MarineMax in 2022 for $480 million, for an EV/EBITDA multiple in the double digits.

ICG has since continued pressuring MarineMax to sell the segment, questioning the company’s board’s interests in the latest public press release, with MarineMax’s board being seemingly against the transaction. MarineMax had previously issued a statement in which the company’s board communicated to be open to potential transactions if they were in the best interest of shareholders.

With the Q3 results sending positive signals for MarineMax’s future, the potential transaction with OneWater may be more unlikely. After the Q3 results sent MarineMax’s stock up, the $40.00 consideration represents a very thin premium of just 7.5% at the time of writing, and I don’t believe that OneWater’s offer would now have to be considerably higher for MarineMax’s shareholders to approve an acquisition. A buyout at a higher consideration is still possible, but with OneWater’s already quite leveraged balance sheet, the rationale gets thinner.

The ICG offer’s rationale also depends more on the final valuation that ICG is ready to offer for the segment – MarineMax now trades at a forward EV/EBITDA of 10.9, making a small double-digit multiple acquisition of the yachting and marina segment likely a poor decision for MarineMax considering the operating leverage from larger operations. ICG has expressed the segment’s poor performance under MarineMax, but with the macroeconomic pressures behind the company’s recent issues, I don’t believe that the poor performance can be written off to a fault of MarineMax.

As such, the situation around potential M&A remains tense. I don’t believe that any transaction is yet the base scenario as OneWater’s rationale for a merger has gotten thinner and as MarineMax’s board is seemingly against ICG’s offer. Still, with especially great potential synergies between OneWater and MarineMax, I don’t write the potential for a merger completely off.

Updated Valuation: Still Attractive

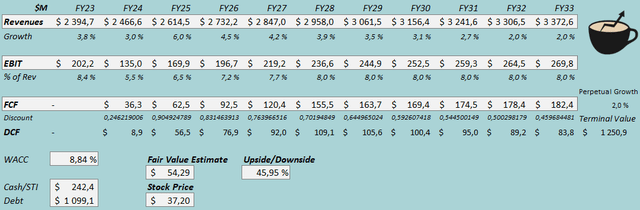

I updated my discounted cash flow [DCF] model from the previous estimates. With the macroeconomic turbulence and lower margins, I now estimate especially a weaker short-term future with only 3.0% revenue growth in FY2024 along with an EBIT of $135.0 million at a margin of 5.5%.

Afterwards, an industry recovery should aid earnings back better, and I estimate elevated growth in the upcoming years also including an expectation of moderate further dealership acquisitions. The total revenue CAGR from FY2023 to FY2033 stands at 3.5%. I now estimate the EBIT margin to rebound into a more conservative estimated level of 8.0% compared to 9.6% previously.

With the estimated moderate acquisitions, and MarineMax’s quite high capital expenditures, I estimate the cash flow conversion to be quite poor especially in the next few years.

DCF Model (Author’s Calculation)

The estimates put MarineMax’s fair value estimate at $54.29, 46% above the stock price at the time of writing – the stock continues to be priced attractively, with the potential M&A adding onto the stock’s upside potential. While the turbulent industry backdrop is still a risk, the margin of safety is really wide at the current level. The fair value estimate is up from $50.49 previously, mainly due to a lower WACC estimate.

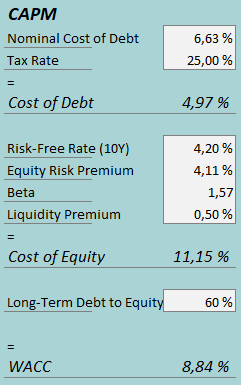

CAPM

A weighted average cost of capital of 8.84% is used in the DCF model, down considerably from 10.64% previously mainly due to a lower equity risk premium and risk-free rate. The used WACC is derived from a capital asset pricing model:

CAPM (Author’s Calculation)

In Q3, MarineMax had $18.2 million in interest expenses, making the company’s interest rate 6.63% with the current amount of interest-bearing debt. With the high floorplan debt and other long-term debt remaining, I estimate a long-term debt-to-equity ratio of 60%.

To estimate the cost of equity, I use the 10-year bond yield of 4.20% as the risk-free rate. The equity risk premium of 4.11% is Professor Aswath Damodaran’s estimate for the US, updated in July. I have kept the beta estimate at 1.57. With a liquidity premium of 0.5%, the cost of equity stands at 11.15% and the WACC at 8.84%.

Takeaway

MarineMax reported Q3 results that exceeded Wall Street’s estimates by a wide margin. The company’s industry environment has been extremely pressured with higher interest rates and a lower consumer sentiment, but the quarter finally showed quite a solid performance after the company has had to lower the FY2024 guidance twice previously in the fiscal year. Potential M&A with OneWater or ICG pose potential upside, and with the valuation remaining attractive, I remain at a Buy rating for MarineMax despite the industry’s remaining risks.

Read the full article here

")

")