")

I’ve been bullish on the VanEck Emerging Markets High Yield Bond ETF (NYSEARCA:HYEM) for several years, as emerging market bonds have traded with strong, above-average yields for quite a while. HYEM’s performance has generally been good, with the fund seeing double-digit, market-beating returns since late 2023, when I last covered the fund. Emerging market bonds continue to trade with strong, above-average yields, and so HYEM remains a buy.

HYEM – Overview and Analysis

Index and Portfolio

HYEM is an index ETF investing in dollar-denominated, high-yield, emerging market corporate bonds. Emerging market issuers are defined as those with significant exposure to emerging markets, including companies headquartered in developed markets. Lots of energy and mining companies meeting these characteristics. Applicable securities must also meet a basic set of inclusion criteria. It is a market-cap weighted index, with country and issuer caps to ensure diversification.

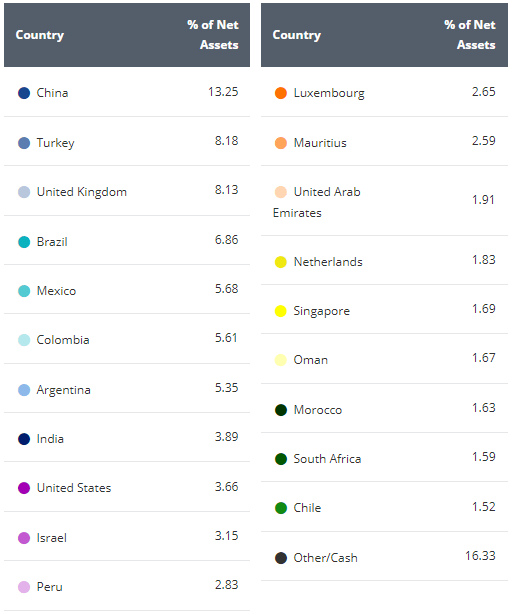

HYEM provides diversified exposure to its industry niche, with investments in over 500 securities from dozens of countries and all relevant industry segments. The fund does focus on emerging markets, with smaller investments in companies headquartered in developed markets. Country weights are reasonably well-diversified, without the significant overweight Chinese / Taiwanese positions common in these funds.

HYEM

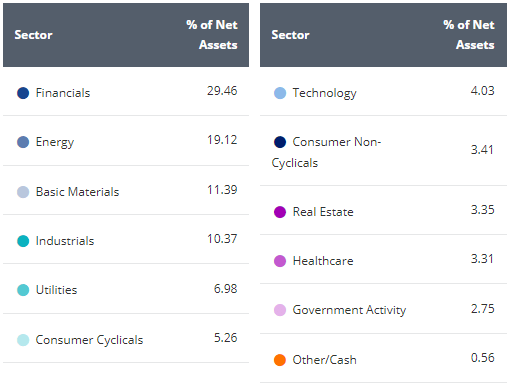

Sector weights are a bit more unbalanced, with significant overweight positions in financials (lots of emerging market banks are publicly traded), energy and materials (important in several emerging markets). Due to the latter, the fund is somewhat exposed to commodity prices, although not significantly so: bonds are senior to equity, and their coupons are not directly dependent on commodity prices.

HYEM

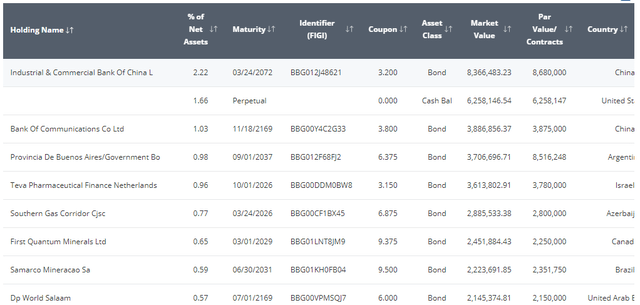

Portfolio concentration is quite low, with the fund’s top ten holdings accounting for less than 10% of its portfolio. Lots of financials and commodity companies here, in-line with broader sector exposures.

HYEM

Besides the above, nothing much else stands out about the fund or its portfolio.

Credit Risk

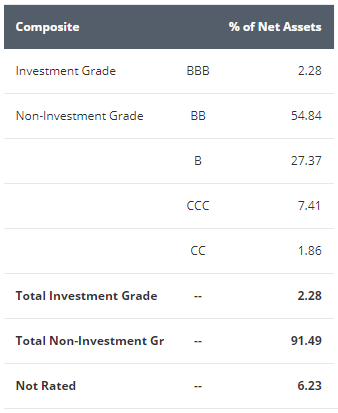

HYEM is on the riskier side of the bond market, with the fund focusing on high-yield, non-investment grade emerging market bonds. The fund focuses on bonds rated BB, with sizable allocations to those rated B and CCC. Overall credit quality seems marginally stronger than average for a high-yield bond ETF, significantly weaker than broader bond ETFs. Focusing on emerging market issuers increases risks too, although some of that risk should be reflected in the credit ratings already.

HYEM

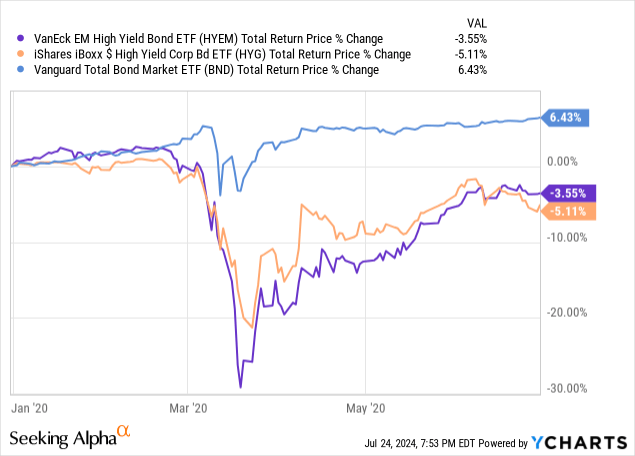

Considering the above, I would expect significant losses during downturns and recessions, significantly higher than those of broad-based bond ETFs, somewhat higher than those of high-yield bond ETFs. HYEM’s losses neared 30% during the pandemic, in-line with expectations. It recovered a bit quicker than benchmark high-yield ETFs though, perhaps due to normal market volatility.

Data by YCharts

Considering the above, HYEM seems about as risky as high-yield bond ETFs. It does have one important advantage relative to these: a higher yield. Let’s have a look.

Dividend Analysis

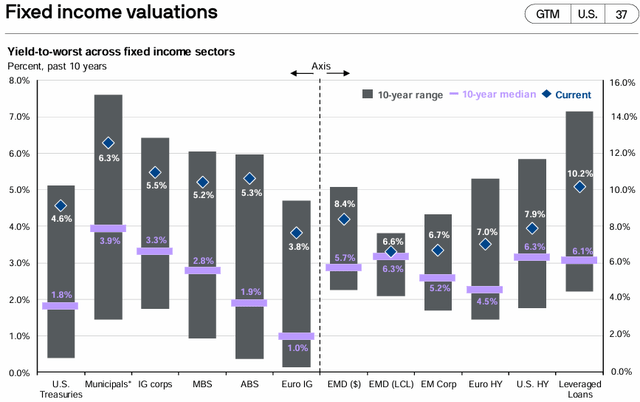

Federal Reserve hikes have led to higher coupon rates across fixed-income sub-asset classes. Some have benefitted more than average, including senior loans and other variable rate investments. Dollar-denominated emerging market bonds have benefitted more than average too, with their yields rising by 2.7%. For reference, U.S. high-yield bond yields have increased by 1.6%

JPMorgan Guide to the Markets

Expanding on the above, emerging market bonds tend to yield 0.6% less than U.S. high-yield bonds but yield 0.5% more right now.

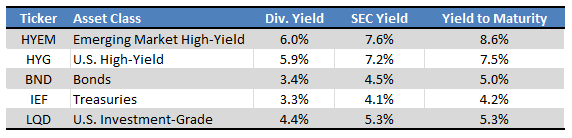

On a more negative note, this is not reflected in fund dividend yields right now, with the fund only yielding 0.1% more than the largest high-yield bond ETF in the market. SEC yields and yield to maturity are higher though, and these two are much more indicative of the actual income generated by the fund, and it’s expected returns, than more traditional TTM dividend yields. I’m not entirely sure why the discrepancy between yields here. It generally takes years for bond ETF dividend yields to reflect market-wide income levels, basically waiting until their existing bond portfolios mature. This might explain the situation, but the Fed started to hike rates several years ago already, and I’m not sure why this would impact HYEM more than average.

Fund Filings – Table by Author

In any case, HYEM’s above-average SEC yield and yield to maturity are both significant benefits for the fund, and advantages relative to high-yield bond ETFs. In my opinion, these benefits are more than enough for a buy rating. I said as much during late 2023, with the fund moderately outperforming since. Spreads have actually widened since then, so the fund is even stronger in this regard now.

Data by YCharts

Performance Analysis

HYEM’s performance track-record is reasonably good, with some caveats.

HYEM has slightly underperformed U.S. high-yield bonds long-term, consistent with their lower long-term average yields.

HYEM moderately underperformed these same bonds from late 2021 to late 2023, when spreads widened. This is reflected in the 3y and 5y returns.

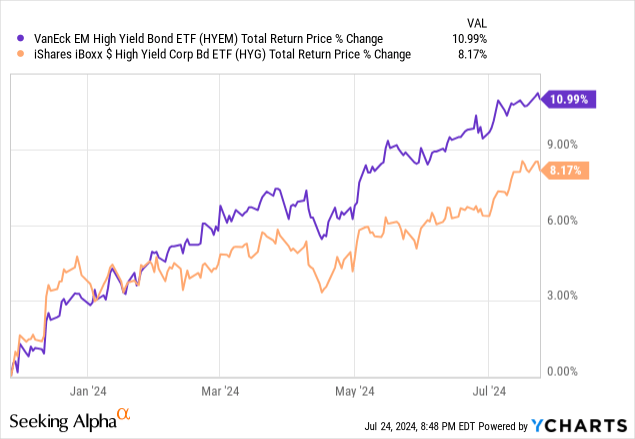

HYEM has moderately outperformed since, due to their higher yields and spreads, and due to these somewhat tightening.

The fund has consistently outperformed other bond sub-asset classes, due to its above-average dividend yield.

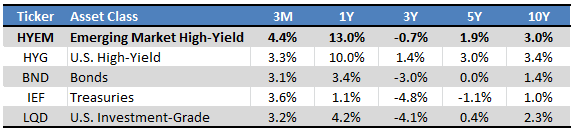

Performance is as follows:

Seeking Alpha – Table by Author

In my opinion, HYEM’s outperformance is set to continue, as the fund continues to trade with higher SEC yields and yields to maturity than average. It has outperformed since these conditions came to be, as expected. Long-term underperformance to U.S. high-yield bonds is an obvious negative, but this reflects markedly different market conditions (negative spreads), and so are not indicative or reflective of expected future returns. In my opinion at least.

Interest Rate Risk

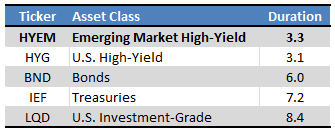

HYEM sports a duration of 3.3 years, in-line with U.S. high-yield bonds, materially lower than those of most other bond sub-asset classes.

Fund Filings – Table by Author

HYEM’s below-average duration should lead to outperformance when rates increase, as has been the case since early 2022.

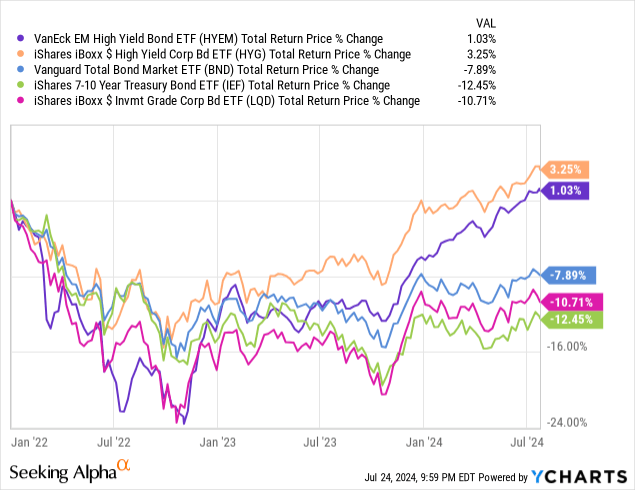

Data by YCharts

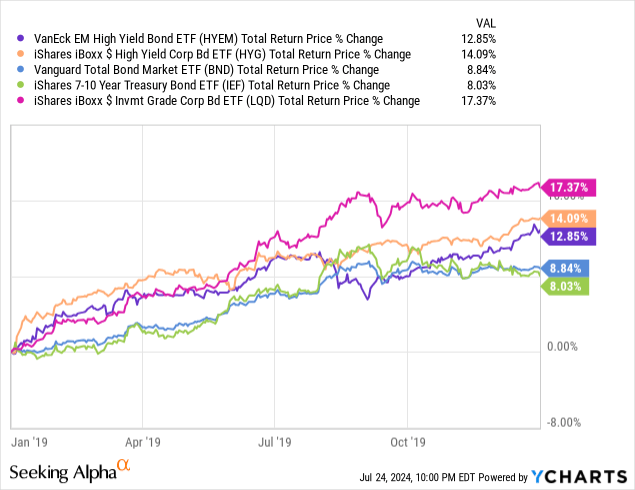

On the flipside, the fund should underperform when rates decrease, although much will depend on the speed and magnitude of any rate cuts. HYEM’s above-average dividends also matter and could end up outweighing any decrease in rates. Excluding the pandemic, rates last decreased in 2019, during which HYEM outperformed most bonds and bond sub-asset classes, mostly due to tightening credit spreads.

Data by YCharts

In my opinion, the situation above is set to repeat itself, as the market already expects several rate cuts, and is pricing bonds accordingly. It ultimately depends on the speed and magnitude of any rate cuts, and the market’s reaction to these, so I might very easily be proven wrong.

An important consideration for investors is the fact that HYEM, and emerging market high-yield bonds more broadly, have the highest fixed-income bond yields. Of the major bond sub-asset classes, only variable rate investments have higher yields. For more dovish investors, HYEM might be a more interesting choice than ETFs focusing on senior loans, CLOs, and the like.

Conclusion

HYEM focuses on emerging market high-yield bonds, the fixed-income securities with the highest yields right now. Due to this, I rate the fund a buy.

Read the full article here

")

")